annual report 2008-09 - IRDA

annual report 2008-09 - IRDA

annual report 2008-09 - IRDA

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

ANNUAL REPORT <strong>2008</strong>-<strong>09</strong><br />

i) World insurance scenario<br />

As per Swiss Re, global insurance premiums in<br />

calendar year <strong>2008</strong> were USD 4270 billiion which is<br />

slightly higher than USD 4128 billiion in 2007. Life<br />

business accounted for USD 2491 billiion; and nonlife<br />

insurance accounted for the remaining USD 1779<br />

billiion. Adjusted for inflation, non-life premiums<br />

declined by 0.8 per cent and life premiums falling even<br />

faster at 3.5 per cent over the previous year. While<br />

underwriting results of non-life insurance business<br />

remained comfortable, investment income and return<br />

on equity fell sharply in both life and non-life insurance.<br />

While life premium in the industrialised countries<br />

declined by 5.3 per cent, in the emerging markets they<br />

increased by 15 per cent in <strong>2008</strong>. The financial crisis<br />

and the economic downturn severely impacted sales<br />

of single premium products and unit-linked products.<br />

The profitability of life insurers deteriorated in <strong>2008</strong><br />

due to low investment yields, high cost of guarantees<br />

and low revenues from asset management fees.<br />

Solvency was impacted and access to capital became<br />

difficult. Slower demand for cover and softening of<br />

premium rates caused decline in non-life premium<br />

volume in <strong>2008</strong>. Non-life premiums declined by 1.9<br />

per cent in the industrialised countries, but recorded<br />

a positive growth of 7.1 per cent in the emerging<br />

markets.<br />

The outlook for insurance industry in 20<strong>09</strong> looks<br />

uncertain due to many challenges. Reduced demand,<br />

low interest rates and the need for additional capital<br />

by many companies are some of the major challenges<br />

facing the insurance industry in 20<strong>09</strong>. The economic<br />

downturn will curb demand for non-life insurance,<br />

particularly in the commercial lines of business.<br />

Demand for personal lines of insurance (eg. Motor) is<br />

likely to be less affected, since insurance spending is<br />

less discretionary, particularly in the industrialised<br />

markets. Insurers may have to focus on underwriting<br />

discipline and reduction in costs so as to remain<br />

profitable.<br />

Average insurance density (per capita premium) in<br />

dollar terms for industrialized countries stood at USD<br />

3655, of which USD 2175 was for life insurance and<br />

USD 1481 was in the non-life insurance. In the<br />

emerging countries, the insurance density was USD<br />

89 (USD 47 in life and USD 42 in non-life segments),<br />

compared to its previous year level of USD 74. The<br />

Insurance density of India was USD 47.4, which<br />

continued to be dominated by life insurance business<br />

(USD 41.2).<br />

Insurance penetration (insurance premium as per cent<br />

of GDP) measures the level of insurance activity<br />

relative to the size of the economy. As GDP per capita<br />

rises, it is expected that individuals will purchase more<br />

insurance. The latest Swiss Re <strong>report</strong> reveals that the<br />

insurance penetration in India was 4.6 per cent in <strong>2008</strong><br />

consisting of 4.0 per cent in life business and 0.6 per<br />

cent from non-life business, unchanged from 2007.<br />

India’s position vis-à-vis other Asian countries in<br />

respect of insurance penetration and density is<br />

depicted in the following tables and graphs.<br />

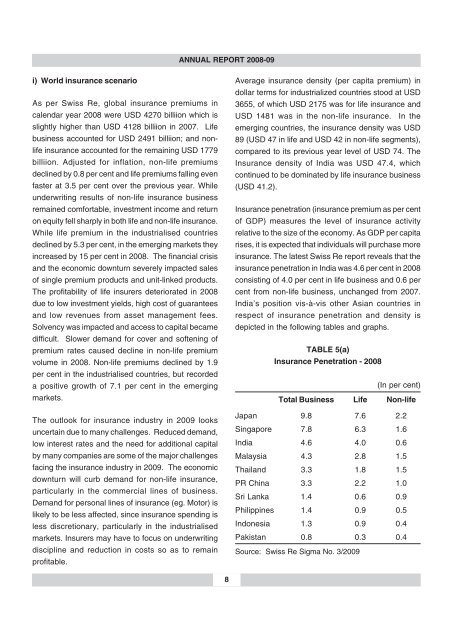

TABLE 5(a)<br />

Insurance Penetration - <strong>2008</strong><br />

(In per cent)<br />

Total Business Life Non-life<br />

Japan 9.8 7.6 2.2<br />

Singapore 7.8 6.3 1.6<br />

India 4.6 4.0 0.6<br />

Malaysia 4.3 2.8 1.5<br />

Thailand 3.3 1.8 1.5<br />

PR China 3.3 2.2 1.0<br />

Sri Lanka 1.4 0.6 0.9<br />

Philippines 1.4 0.9 0.5<br />

Indonesia 1.3 0.9 0.4<br />

Pakistan 0.8 0.3 0.4<br />

Source: Swiss Re Sigma No. 3/20<strong>09</strong><br />

8