- Page 2 and 3: 4 AST Goldman Sachs Mid-Cap Growth

- Page 5: CONTENTSGLOSSARY OF TERMS .........

- Page 8 and 9: Good Order: An instruction received

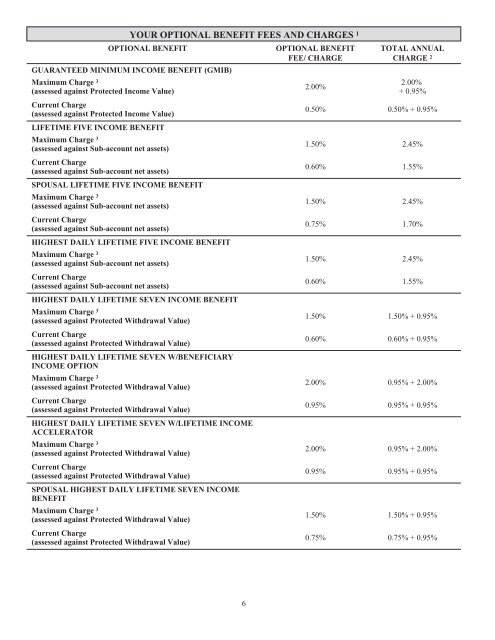

- Page 10 and 11: SUMMARY OF CONTRACT FEES AND CHARGE

- Page 14 and 15: 1 How Living Benefit Charges are De

- Page 16 and 17: UNDERLYINGPORTFOLIOUNDERLYING MUTUA

- Page 18 and 19: 1 AST Advanced Strategies Portfolio

- Page 20 and 21: EXPENSE EXAMPLEThis example is inte

- Page 22 and 23: Where should I invest my money? Wit

- Page 24 and 25: Charges for Optional Benefits: If y

- Page 26 and 27: Group I: Allowable Benefit Allocati

- Page 28 and 29: Certain optional living benefits (e

- Page 30 and 31: ADVANCED SERIESTRUST (“AST”)POR

- Page 32 and 33: ADVANCED SERIESTRUST (“AST”)POR

- Page 34 and 35: ADVANCED SERIESTRUST (“AST”)POR

- Page 36 and 37: ▪ If you are not participating in

- Page 38 and 39: increase the Annual Maintenance Fee

- Page 40 and 41: PURCHASING YOUR ANNUITYPlease note

- Page 42 and 43: Owner, Annuitant and Beneficiary De

- Page 44 and 45: Account. The ability to continue th

- Page 46 and 47: MANAGING YOUR ACCOUNT VALUEHOW AND

- Page 48 and 49: Any transfer to or from any Sub-acc

- Page 50 and 51: HOW MUCH CAN I WITHDRAW AS A FREE W

- Page 52 and 53: WHAT IS A MEDICALLY-RELATED SURREND

- Page 54 and 55: LIVING BENEFITSDO YOU OFFER BENEFIT

- Page 56 and 57: HIGHEST DAILY GUARANTEED RETURN OPT

- Page 58 and 59: pre-determined mathematical formula

- Page 60 and 61: Special Considerations under HD GRO

- Page 62 and 63:

HD GRO, by moving assets out of cer

- Page 64 and 65:

▪▪▪▪▪You cannot participa

- Page 66 and 67:

Key Feature - Protected Income Valu

- Page 68 and 69:

On the date that you elect to begin

- Page 70 and 71:

Step-Up of the Protected Withdrawal

- Page 72 and 73:

Annual Income Amount for future Ann

- Page 74 and 75:

Additional Tax ConsiderationsIf you

- Page 76 and 77:

BENEFITS UNDER THE SPOUSAL LIFETIME

- Page 78 and 79:

As indicated, withdrawals made whil

- Page 80 and 81:

The Highest Daily Lifetime Five ben

- Page 82 and 83:

▪▪▪▪▪▪example, withdraw

- Page 84 and 85:

Depending on the results of the for

- Page 86 and 87:

Once the 90% cap feature is met, fu

- Page 88 and 89:

that varies based on the age of the

- Page 90 and 91:

▪▪If no withdrawal was ever tak

- Page 92 and 93:

we use 5% in the formula, irrespect

- Page 94 and 95:

Upon a death that triggers payment

- Page 96 and 97:

LIA amount at the first Withdrawal.

- Page 98 and 99:

Important Consideration When Electi

- Page 100 and 101:

each Annuity Anniversary, by perfor

- Page 102 and 103:

▪▪If no withdrawal was ever tak

- Page 104 and 105:

election to begin receiving annuity

- Page 106 and 107:

treatment of withdrawals. We do not

- Page 108 and 109:

are no assurances that future trans

- Page 110 and 111:

You may use the Systematic Withdraw

- Page 112 and 113:

In this example, 5% of the December

- Page 114 and 115:

▪▪If no Lifetime Withdrawal was

- Page 116 and 117:

difference by the amount held withi

- Page 118 and 119:

Additional Tax ConsiderationsIf you

- Page 120 and 121:

Eligibility Requirements for LIA Am

- Page 122 and 123:

withdraw an annual amount (the “A

- Page 124 and 125:

Highest Daily Auto Step-UpAn automa

- Page 126 and 127:

The Non-Lifetime Withdrawal will pr

- Page 128 and 129:

Other Important Considerations▪ W

- Page 130 and 131:

If you take a partial withdrawal to

- Page 132:

Value is equal to your Account Valu

- Page 135 and 136:

You must tell us if your withdrawal

- Page 137 and 138:

▪In the absence of an election wh

- Page 139 and 140:

which we are providing administrati

- Page 141 and 142:

to the Bond Sub-account occurs. The

- Page 143 and 144:

(2) The designated life is unable t

- Page 145 and 146:

annual amount (the “Annual Income

- Page 147 and 148:

Withdrawal Value and your Account V

- Page 149 and 150:

▪ The Account Value at benefit el

- Page 151 and 152:

If no Lifetime Withdrawal was ever

- Page 153 and 154:

designated life (except as may be n

- Page 155 and 156:

Calculation of the Combination 5% R

- Page 157 and 158:

Can I terminate the optional Death

- Page 159 and 160:

▪▪▪Withdrawals are not subjec

- Page 161 and 162:

The NYSE is closed on the following

- Page 163 and 164:

TAX CONSIDERATIONSThe tax considera

- Page 165 and 166:

If an Annuity is purchased through

- Page 167 and 168:

A Nonqualified annuity may also be

- Page 169 and 170:

account” described under Code Sec

- Page 171 and 172:

insurance/annuity products to plans

- Page 173 and 174:

WHAT IS THE SEPARATE ACCOUNT?The Se

- Page 175 and 176:

WHO DISTRIBUTES ANNUITIES OFFERED B

- Page 177 and 178:

Mutual of Omaha BankNational Planni

- Page 179 and 180:

concerning certain business or proc

- Page 181 and 182:

APPENDIX A-ACCUMULATION UNIT VALUES

- Page 183 and 184:

Sub-AccountsAccumulationUnit Value

- Page 185 and 186:

Sub-AccountsAccumulationUnit Value

- Page 187 and 188:

Sub-AccountsAccumulationUnit Value

- Page 189 and 190:

Sub-AccountsAccumulationUnit Value

- Page 191 and 192:

Sub-AccountsAccumulationUnit Value

- Page 193 and 194:

Sub-AccountsAccumulationUnit Value

- Page 195 and 196:

Sub-AccountsAccumulationUnit Value

- Page 197 and 198:

Sub-AccountsAccumulationUnit Value

- Page 199 and 200:

APPENDIX B-CALCULATION OF OPTIONAL

- Page 201 and 202:

APPENDIX C-FORMULA UNDER HIGHEST DA

- Page 203 and 204:

The following formula, which is set

- Page 205 and 206:

APPENDIX D-FORMULA UNDER HIGHEST DA

- Page 207 and 208:

The formula will transfer assets in

- Page 209 and 210:

The formula will transfer assets in

- Page 211 and 212:

APPENDIX E-FORMULA UNDER HIGHEST DA

- Page 213 and 214:

The following formula, which is set

- Page 215 and 216:

“a” Factors for Liability Calcu

- Page 217 and 218:

APPENDIX F-FORMULA FOR HIGHEST DAIL

- Page 219 and 220:

“a” Factors for Liability Calcu

- Page 221 and 222:

APPENDIX G-SPECIAL CONTRACT PROVISI

- Page 223 and 224:

APPENDIX H-FORMULA UNDER HIGHEST DA

- Page 225 and 226:

FORMULA FOR ELECTIONS OF HD GRO II

- Page 227 and 228:

APPENDIX I-FORMULA FOR HIGHEST DAIL

- Page 229 and 230:

“a” Factors for Liability Calcu

- Page 231 and 232:

PRUCO LIFE INSURANCE COMPANY (PRUCO

- Page 233 and 234:

Deducting ContributionsGenerally, y

- Page 235 and 236:

Required Minimum DistributionsIf yo

- Page 237 and 238:

traditional IRA at the end of your

- Page 239 and 240:

income), pension or annuity income,

- Page 241 and 242:

2. The payment or distribution is:a

- Page 243 and 244:

PRUCO LIFE INSURANCE COMPANY(A PRUD

- Page 245 and 246:

PLEASE SEND ME A STATEMENT OF ADDIT