Michel Dacorogna, Tail-Dependence an Essential Factor for

Michel Dacorogna, Tail-Dependence an Essential Factor for

Michel Dacorogna, Tail-Dependence an Essential Factor for

- No tags were found...

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

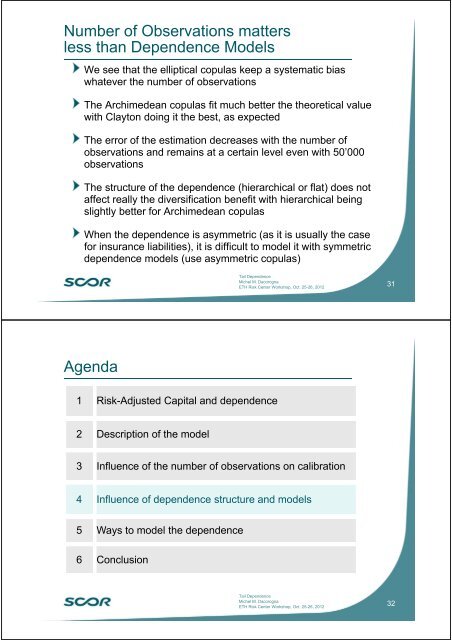

Number of Observations mattersless th<strong>an</strong> <strong>Dependence</strong> ModelsWe see that the elliptical copulas keep a systematic biaswhatever the number of observationsThe Archimede<strong>an</strong> copulas fit much better the theoretical valuewith Clayton doing it the best, as expectedThe error of the estimation decreases with the number ofobservations <strong>an</strong>d remains at a certain level even with 50’000observationsThe structure of the dependence (hierarchical or flat) does notaffect really the diversification benefit with hierarchical beingslightly better <strong>for</strong> Archimede<strong>an</strong> copulasWhen the dependence is asymmetric (as it is usually the case<strong>for</strong> insur<strong>an</strong>ce liabilities), it is difficult to model it with symmetricdependence models (use asymmetric copulas)<strong>Tail</strong> <strong>Dependence</strong><strong>Michel</strong> M. <strong>Dacorogna</strong>ETH Risk Center Workshop, Oct. 25-26, 201231Agenda1 Risk-Adjusted Capital <strong>an</strong>d dependence2 Description of the model3 Influence of the number of observations on calibration4 Influence of dependence structure <strong>an</strong>d models5 Ways to model the dependence6 Conclusion<strong>Tail</strong> <strong>Dependence</strong><strong>Michel</strong> M. <strong>Dacorogna</strong>ETH Risk Center Workshop, Oct. 25-26, 201232