Michel Dacorogna, Tail-Dependence an Essential Factor for

Michel Dacorogna, Tail-Dependence an Essential Factor for

Michel Dacorogna, Tail-Dependence an Essential Factor for

- No tags were found...

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

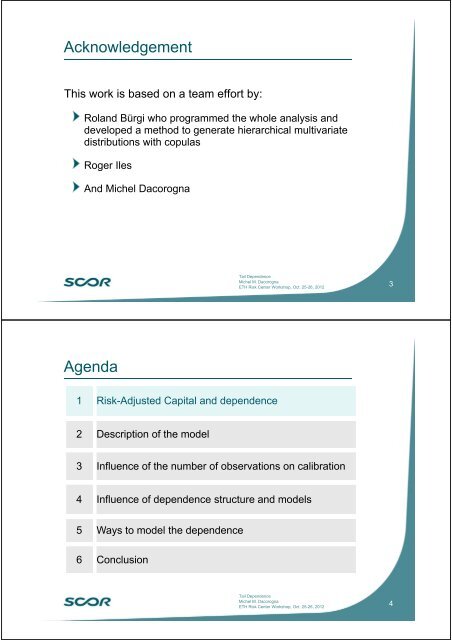

AcknowledgementThis work is based on a team ef<strong>for</strong>t by:Rol<strong>an</strong>d Bürgi who programmed the whole <strong>an</strong>alysis <strong>an</strong>ddeveloped a method to generate hierarchical multivariatedistributions with copulasRoger IlesAnd <strong>Michel</strong> <strong>Dacorogna</strong><strong>Tail</strong> <strong>Dependence</strong><strong>Michel</strong> M. <strong>Dacorogna</strong>ETH Risk Center Workshop, Oct. 25-26, 20123Agenda1 Risk-Adjusted Capital <strong>an</strong>d dependence2 Description of the model3 Influence of the number of observations on calibration4 Influence of dependence structure <strong>an</strong>d models5 Ways to model the dependence6 Conclusion<strong>Tail</strong> <strong>Dependence</strong><strong>Michel</strong> M. <strong>Dacorogna</strong>ETH Risk Center Workshop, Oct. 25-26, 20124