Michel Dacorogna, Tail-Dependence an Essential Factor for

Michel Dacorogna, Tail-Dependence an Essential Factor for

Michel Dacorogna, Tail-Dependence an Essential Factor for

- No tags were found...

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

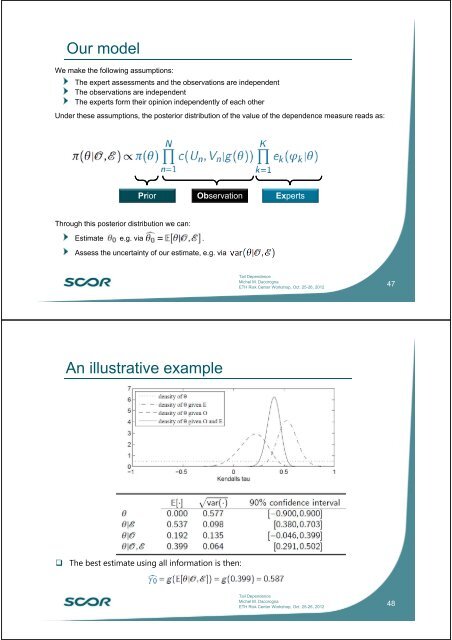

Our modelWe make the following assumptions:The expert assessments <strong>an</strong>d the observations are independentThe observations are independentThe experts <strong>for</strong>m their opinion independently of each otherUnder these assumptions, the posterior distribution of the value of the dependence measure reads as:PriorObservationExpertsThrough this posterior distribution we c<strong>an</strong>:Estimate , e.g. via .Assess the uncertainty of our estimate, e.g. via .<strong>Tail</strong> <strong>Dependence</strong><strong>Michel</strong> M. <strong>Dacorogna</strong>ETH Risk Center Workshop, Oct. 25-26, 201247An illustrative exampleThe best estimate using all in<strong>for</strong>mation is then:<strong>Tail</strong> <strong>Dependence</strong><strong>Michel</strong> M. <strong>Dacorogna</strong>ETH Risk Center Workshop, Oct. 25-26, 201248