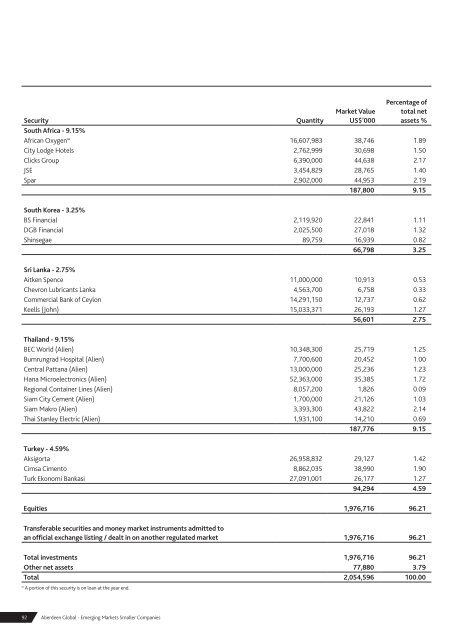

Market ValueUS$’000Percentage oftotal netassets %SecurityQuantitySouth Africa - 9.15%African Oxygen ∞ 16,607,983 38,746 1.89City Lodge Hotels 2,762,999 30,698 1.50Clicks Group 6,390,000 44,638 2.17JSE 3,454,829 28,765 1.40Spar 2,902,000 44,953 2.19187,800 9.15South Korea - 3.25%BS Financial 2,119,920 22,841 1.11DGB Financial 2,025,500 27,018 1.32Shinsegae 89,759 16,939 0.8266,798 3.25Sri Lanka - 2.75%Aitken Spence 11,000,000 10,913 0.53Chevron Lubricants Lanka 4,563,700 6,758 0.33Commercial Bank of Ceylon 14,291,150 12,737 0.62Keells (John) 15,033,371 26,193 1.2756,601 2.75Thailand - 9.15%BEC World (Alien) 10,348,300 25,719 1.25Bumrungrad Hospital (Alien) 7,700,600 20,452 1.00Central Pattana (Alien) 13,000,000 25,236 1.23Hana Microelectronics (Alien) 52,363,000 35,385 1.72Regional Container Lines (Alien) 8,057,200 1,826 0.09Siam City Cement (Alien) 1,700,000 21,126 1.03Siam Makro (Alien) 3,393,300 43,822 2.14Thai Stanley Electric (Alien) 1,931,100 14,210 0.69187,776 9.15Turkey - 4.59%Aksigorta 26,958,832 29,127 1.42Cimsa Cimento 8,862,035 38,990 1.90Turk Ekonomi Bankasi 27,091,001 26,177 1.2794,294 4.59Equities 1,976,716 96.21Transferable securities and money market instruments admitted toan official exchange listing / dealt in on another regulated market 1,976,716 96.21Total investments 1,976,716 96.21Other net assets 77,880 3.79Total 2,054,596 100.00∞A portion of this security is on loan at the year end.92 <strong>Aberdeen</strong> <strong>Global</strong> - Emerging Markets Smaller Companies

Ethical World EquityFor the year ended 30 September 2012PerformanceFor the year ended 30 September 2012, the value of the Ethical WorldEquity - A Accumulation shares increased by 17.16% compared to anincrease of 21.98% in the benchmark, the FTSE World Index.Source: Lipper, Basis: total return, NAV to NAV, net of annual charges, gross incomereinvested, USD.Manager’s review<strong>Global</strong> equities rallied in the year under review, largely drivenby the vast amount of liquidity injected into the global financialsystem. Developed markets generally outperformed their emergingcounterparts. Throughout the period, the Eurozone debt crisis andslowing economic activity dominated sentiment. Notably, the tenuousrecovery in the US and a significant deceleration in China’s growth casta pall over the global economic outlook. But risk appetite returnedfollowing efforts by major central banks to provide emergency loansto European banks, while Britain and Japan expanded quantitativeeasing. In particular, the European Central Bank (ECB)’s long-termrefinancing operation for lenders raised investors’ hopes, as did newsof the €130 billion Greek bailout. Optimism that funding pressureswould ease was also boosted by the ECB’s interest rate cuts to ahistoric low and bond-buying programme, known as OutrightMonetary Transactions. As well, the US Federal Reserve’s (Fed)third round of quantitative easing lifted sentiment towards theend of the period.Portfolio reviewThe Fund’s underperformance was largely a result of the underweightto the US, where the stock market outperformed following the Fed’spolicy easing. Stock selection there was weak as well. Not holdingApple cost the Fund, as the US technology company’s share price wasboosted by robust full-year results, driven by sales of its latest iPhoneand iPad models. It also declared its first dividend pay-out in 17 yearsand a US$10 billion stock buyback. Meanwhile, holding cereal makerKellogg Co and energy company Hess Corp detracted from relativeperformance. Kellogg ended the year largely flat after it pared itsearnings forecast, following its purchase of Procter & Gamble’sPringles business, while Hess Corp posted disappointing results;we have since disposed of the stock.Against this, the sharp rally in the crude oil price benefited ourholdings in the oil and gas sector such as Italian-listed pipe makerTenaris and Eni, as well as EOG Resources in the US. Tenaris alsogained from healthy third-quarter profits, while a sharp increasein output of petroleum liquids proved beneficial for EOG.In portfolio activity, we introduced several companies at attractivevaluations. These included Hong Kong-based insurance group AIA,a high quality company with good growth prospects in Asia, andUS cable company Comcast, which generates solid cash flowsthat could lead to attractive dividend payouts. Other new holdingsincluded Japanese medical equipment maker Sysmex, French utilityGDF Suez, which has an attractive international asset base, andSpanish food-casing manufacturer Viscofan, owing to the strengthof its business and healthy outlook. In the UK, we initiated positionsin industrial company Weir Group on the back of attractive long-termopportunities, energy services company John Wood, a well-managedbusiness with good long-term potential, and steam specialistSpirax-Sarco Engineering.Against this, we sold Japan’s Takeda Pharmaceutical and machinetoolmaker Amada because of their deteriorating outlook, as well asthe aforementioned US energy company Hess.OutlookWhile recent stimulus efforts by major central banks may have liftedmarkets, these stop-gap measures appear to succeed only in boostingshort-term sentiment and inflating asset prices, instead of providingviable long-term solutions. Evidently, central bank policies onlycontribute to half of the equation, with the other half dependent ongovernment spending via fiscal policies. At present, we remain waryof several events, including the looming “fiscal cliff” in the US and thepossibility of a Chinese hard landing, which will have a dire impact onexport-dependent economies. On the corporate front, the earningsoutlook appears challenging. As such, we maintain a cautious stance.www.aberdeen-asset.com93