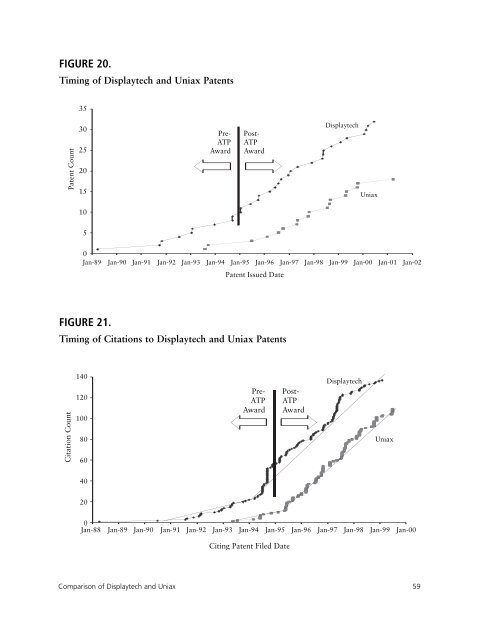

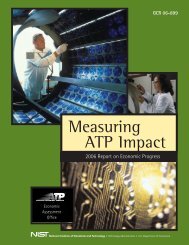

percent thereafter. The pattern suggests that the net social value employment effect <strong>of</strong> bothfirms is in the same order <strong>of</strong> magnitude, with a two-year lag for Uniax.Because Uniax technology has not yet entered mass commercial markets, lacking efficientcomplementary manufacturing equipment technologies, <strong>and</strong> because <strong>of</strong> the existing fiercecompetition among the 100 or so firms in those markets, there is little additional economicsurplus yet from either price or quantity effects directly stemming from Uniax activities.Future economic surplus directly in these markets, however, may be significant if thepotential discussed above is ever realized, particularly for radical product categories thatflexible displays could enable. We address the broader knowledge spillover effects belowwhile discussing the patent <strong>and</strong> publication citation analysis.Comparing the two cases, then, both Uniax <strong>and</strong> Displaytech have created roughly the sameorder <strong>of</strong> magnitude (low tens <strong>of</strong> millions <strong>of</strong> dollars) in total direct economic value from theirtechnologies, well in excess <strong>of</strong> the federal investments, resulting in similar magnitude NPVs(mid-millions). In both cases, the time-to-mass-market horizon was eight or more years,consistent with <strong>ATP</strong>’s stated high-risk, long-term mission. <strong>ATP</strong> investment in Displaytech,based on a proposal from the same award competition as Uniax, accelerated Displaytech’smarket entry by about two years, attracted venture capital, <strong>and</strong>, along with other federalcontracts in our view, allowed the firm to weather the technology downturn. Uniax survivedwith private equity investments <strong>and</strong> licensing revenue from large firms <strong>and</strong> non-<strong>ATP</strong> federalcontracts. Yet even now, despite DuPont’s resources, mass-market entry for the technologyproposed to <strong>ATP</strong> remains elusive <strong>and</strong> lags at least two years behind Displaytech. As acounterfactual exercise, it is difficult to know whether an <strong>ATP</strong> award would have furtheraccelerated Uniax’s learning curve to commercialization or whether Uniax would have beenable to attract additional equity earlier or in greater volumes.PATENT CITATION ANALYSISCounterfactual problems notwithst<strong>and</strong>ing, a similar time lag between the two cases ariseswhen we turn to patent citations. As shown in Figures 20 <strong>and</strong> 21, the timing <strong>of</strong> Uniaxpatents <strong>and</strong> patent citations follows a remarkably parallel course to Displaytech’s, with abouta two-year delay. The graphs show cumulative patent counts (by patent issue date) <strong>and</strong>patent citation counts (by filing date) over time. The rate <strong>of</strong> Displaytech patenting picks upsignificantly around the time <strong>of</strong> the 1994 $1.75 million <strong>ATP</strong> award, <strong>and</strong> Uniax patentingaccelerates around the time <strong>of</strong> the 1996 $3 million equity investments by Hoechst <strong>and</strong>Philips. Because <strong>of</strong> the delay between patent filing <strong>and</strong> issue, in both cases it appears that theinvestments followed successful early technological progress.Turning to the timing <strong>of</strong> the citations to each firm’s patents, a similar two-year lag appears,as does the pattern <strong>of</strong> investment following technical progress. With striking similarity inboth cases, the rate <strong>of</strong> citation picks up well in advance <strong>of</strong> the cash infusions. Thetechnologies <strong>of</strong> both firms began attracting notice as revealed through citation by others,which indicates a growing interest in their commercial potential. The revealed technicalsuccess <strong>and</strong> increasing notoriety precedes (<strong>and</strong> it seems reasonable to assume is causally58 DIRECT AND SPILLOVER EFFECTS OF <strong>ATP</strong>-FUNDED PHOTONICS TECHNOLOGIES

FIGURE 20.Timing <strong>of</strong> Displaytech <strong>and</strong> Uniax Patents35 35Patent CountPatent Count30252015Post-Post-<strong>ATP</strong><strong>ATP</strong>Award AwardPre-Pre-<strong>ATP</strong><strong>ATP</strong>AwardDisplaytechDisplaytechUniax1050Jan-89 Jan-90 Jan-91 Jan-92 Jan-93 Jan-94 Jan-95 Jan-96 Jan-97 Jan-98 Jan-99 Jan-00 Jan-01 Jan-02Patent Issued DatePatent Issued DateFIGURE 21.Timing <strong>of</strong> Citations to Displaytech <strong>and</strong> Uniax PatentsCitation Count Count1401201008060Post-<strong>ATP</strong>AwardAwardPre-<strong>ATP</strong>AwardAwardDisplaytechDisplaytechUniaxUniax40200Jan-88 Jan-89 Jan-90 Jan-91 Jan-92 Jan-93 Jan-94 Jan-95 Jan-96 Jan-97 Jan-98 Jan-99 Jan-00Citing PatentFiledDateCiting Patent Filed DateComparison <strong>of</strong> Displaytech <strong>and</strong> Uniax 59