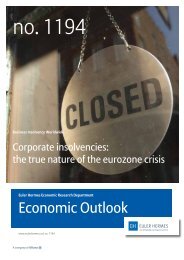

<strong>Euler</strong> <strong>Hermes</strong>Economic Outlook n° 1187 | Special Report | The <strong>Re<strong>in</strong>dustrialization</strong> of the United StatesIt is the (macro)economy, stupid!With the deceleration of the global economyand prolonged limbo of the euro zone, the U.S.economy appears to be particularly central toglobal recovery. However, domestically, severalsteps need to be taken to limit the damage of thefiscal situation, curb unemployment figures, andbenefit fully from the aggressive monetary policystance chosen by the Fed. It will also be necessary tocont<strong>in</strong>ue to unleash growth drivers: consumption,private sector <strong>in</strong>vestments, and exports to offset thegradual withdrawal of the post-crisis governmentspend<strong>in</strong>g, without caus<strong>in</strong>g damage. Is this feasible?We argue that there are some green shoots whichcould lead to a favorable macroeconomic backdrop,aga<strong>in</strong>st which what we call the “<strong>Re<strong>in</strong>dustrialization</strong>of the U.S.” is possible.A. Macroeconomic Forecasts for the U.S.U.S.A. share 2011 2012 2013 2014GDP 100% 1.8 2.2 1.9 2.5Consumer Spend<strong>in</strong>g 71% 2.5 2.0 2.2 2.6Public Spend<strong>in</strong>g 19% -3.1 -1.9 -1.4 -1.3Investment 13% 6.6 7.8 3.9 7.2Construction 2% -1.4 11.6 9.5 10,3Equipment 10% 8.6 6.9 2.4 6.5Stocks* 0% -0.2 0.1 0.1 0,0Exports 13% 6.7 3.6 4.3 6.5Imports 16% 4.8 2.8 3.5 6.5Net exports * ‐3% 0.1 0.0 -0.0 -0.2Current account ** ‐466 -508 -495 -477Current account (% of GDP) -3.1 -3.2 -3.0 -2.8Employment 0.6 1.7 1.1 1.5Unemployment rate 8.9 8.1 7.7 7.1Wages 2.0 1.5 1.9 2.2Inflation 3.3 2.2 2.0 2.1General government balance ** -1250 -1129 -1039 -981General government balance (% of GDP) -8.3 -7.2 -6.4 -5.8Public debt (% of GDP) 101.0 104.8 108.1 110.1Nom<strong>in</strong>al GDP ** 15 076 15 684 16 230 16 909Change over the period, unless otherwise <strong>in</strong>dicated: * contribution to GDP growth ** U.S.D billionsSource : IHS Global Insight, <strong>Euler</strong> <strong>Hermes</strong>6

Economic Outlook n° 1187 | Special Report | The <strong>Re<strong>in</strong>dustrialization</strong> of the United States<strong>Euler</strong> <strong>Hermes</strong>Fall<strong>in</strong>g over the ‘fiscal cliff’:why the short-term outlook is worry<strong>in</strong>gThe U.S. economy still faces significantheadw<strong>in</strong>ds result<strong>in</strong>g <strong>in</strong> expectationsof sub-par GDP growth and elevatedunemployment for 2013. The FederalReserve has started another roundof quantitative eas<strong>in</strong>g (QE3) to helpstimulate the hous<strong>in</strong>g market and thebroader economy. However, QE3 islikely to have a very limited effect anduncerta<strong>in</strong>ty surround<strong>in</strong>g the fiscalsituation is likely to contribute to theweakness.u Recent DevelopmentsThe U.S. economy lost 9 million jobs <strong>in</strong> the recessionand as of August 2012, more than three years s<strong>in</strong>ce therecession ended, it has only recovered about half thatamount. The unemployment rate, despite a recentdecl<strong>in</strong>e, has rema<strong>in</strong>ed above 8% for three and one halfyears and the labor participation rate is the lowest ithas been <strong>in</strong> 30 years. GDP has been correspond<strong>in</strong>glyweak, grow<strong>in</strong>g only 2.1% over the past four quarters.Manufactur<strong>in</strong>g, which helped lead the economy outof recession, has been stumbl<strong>in</strong>g for several months,and while consumers have enjoyed some recentga<strong>in</strong>s <strong>in</strong> <strong>in</strong>come, consumption still rema<strong>in</strong>s weak.Positives have <strong>in</strong>cluded surpris<strong>in</strong>gly strong auto sales,a firm<strong>in</strong>g hous<strong>in</strong>g market, and fall<strong>in</strong>g <strong>in</strong>solvencies.u Mixed perspectives for 2013Loom<strong>in</strong>g events will make for yet another year ofsub-par GDP growth <strong>in</strong> 2013 - around 2% - withunemployment most likely rema<strong>in</strong><strong>in</strong>g near 8%. Theuncerta<strong>in</strong>ty of the fiscal situation at the beg<strong>in</strong>n<strong>in</strong>g of2013 is weigh<strong>in</strong>g on the economy. Even if a plan isdevised to reduce the country’s debt, it will probablynot have much effect until the middle of 2013 at theearliest. Fiscal Contraction could push the economy<strong>in</strong>to recession. However, the most likely scenario isthat most of the fiscal contraction will be avoided s<strong>in</strong>ceboth Republicans and Democrats believe that such arapid fiscal withdrawal would be politically dangerousand a serious blow to the economy. Yet uncerta<strong>in</strong>tyrema<strong>in</strong>s as the fiscal situation issues may not beaddressed entirely by the new session of Congress.On the monetary side, while QE3 is <strong>in</strong>tended to boostthe hous<strong>in</strong>g sector by lower<strong>in</strong>g mortgage rates, theplan is unlikely to help much s<strong>in</strong>ce mortgage ratesare already near historical lows. Risk-averse bankershave slowed the mortgage market, not high <strong>in</strong>terestrates. Nonetheless, there has been some firm<strong>in</strong>g <strong>in</strong>several hous<strong>in</strong>g market measures such as prices andunit sales, but it is premature to call a bottom. On anupbeat note, <strong>in</strong>solvencies are expected to fall 8% <strong>in</strong>2013 due to positive, albeit weak GDP growth.• • •Estimat<strong>in</strong>g the impact of the fiscal situationu What: A comb<strong>in</strong>ation of higher taxes and reducedspend<strong>in</strong>g at the start of 2013.u How much: Fiscal tighten<strong>in</strong>g would amount to a good4% of GDP <strong>in</strong> 2013 (5% of GDP, if changes <strong>in</strong> revenues andspend<strong>in</strong>g unl<strong>in</strong>ked to specific policies are <strong>in</strong>cluded). Ifthe automatic spend<strong>in</strong>g cuts (across-the-board spend<strong>in</strong>gcuts) under the Budget Control Act are avoided,fiscal tighten<strong>in</strong>g would be reduced to between 1.8% ofGDP and 2.7% of GDP, respectively. Apply<strong>in</strong>g an overallfiscal multiplier of 0.75, the drag on GDP growth wouldamount to between 1.4% and 2%, respectively.u To put 2013 fiscal tighten<strong>in</strong>g <strong>in</strong>to perspective: Generalgovernment net borrow<strong>in</strong>g amounted to 8.7% of GDP <strong>in</strong>H1 2012, down from 10.25% of GDP <strong>in</strong> 2011.7