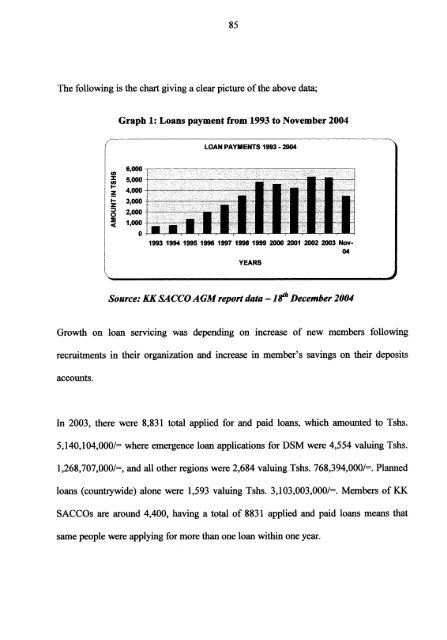

844.1.2.2 ProductsKK SACC O had been issuing two types of loans to its members (article 34(1) of KK bylaws),the emergence loan with a maximum of Tshs.300,000/= payable in 6 months andplanned (long term) loan reaching as high as three times of member's savings, payablewithin 48 months. O n the AGM held on 20 th and 21 st December 2002 members agreedto introduc e a new product, " education loan" that starte d wit h effec t from Januar y2004. Before 2004, some of the loans issued for other uses were also used to pay schoolfees until members decided to officiate it as one of its main products.The maximu m payment o f this loa n i s Tshs.l , 000,000/ = payabl e directl y to therespective schoo l or college with repaymen t perio d of 12 months. For members whowants loans for school fees exceeding Tshs. 1.0 million the y have to fill planne d loanforms instead of education fees forms and the loan is paid directly to them. Members areallowed to have all types of loans, provided the total amount should not exceed threetimes of their savings.For th e past 1 2 years, including 1 1 months of year 2004, KK SACCO have granted atotal sum of Tshs.38.039 Billion as shown on the table below;Table 14: Loans paid from 1993 to November 2004YEARLOAN GRANTED (Tshs) GROWTH RAT E1993 639,225,818 -1994 734,647,200 15%1995 1,307,945,650 78%1996 1,980,283,159 51%1997 2,621,864,650 32%1998 3,482,545,575 33%1999 4,756,916,732 37%2000 4,542,725,673 (5)%2001 4,183,311,999 (8)%2002 5,217,419,666 25%2003 5,140,104,000 (D%NOV-2004 3,432,162,903 (33)%TOTAL 38,039,153,025Source: KKSACCO AGMreport-18? December 2004

85The following is the chart giving a clear picture of the above data;Graph 1: Loans payment from 1993 t o November 2004Growth o n loa n servicin g wa s dependin g o n increas e o f ne w member s followin grecruitments in their organization and increase in member's saving s on their depositsaccounts.In 2003, there were 8,831 tota l applied for and paid loans , which amounte d to Tshs.5,140,104,000/= where emergence loan applications for DSM were 4,554 valuing Tshs.1,268,707,000/=, and all other regions were 2,684 valuing Tshs. 768,394,000/=. Plannedloans (countrywide) alone were 1,59 3 valuing Tshs. 3,103,003,000/=. Members of KKSACCOs ar e around 4,400, having a total of 8831 applied and paid loan s means thatsame people were applying for more than one loan within one year.

- Page 1:

SOUTHERN NEW HAMPHSHIRE UNIVERSIT Y

- Page 4 and 5:

iiiDECLARATION:I, Kassian A. Mtey,

- Page 6 and 7:

ABSTRACTCooperative system s wer e

- Page 8 and 9:

viiABBREVIATIONACCOSCA Africa n Con

- Page 10 and 11:

ix2.3 Polic y review 4 3CHAPTER HI3

- Page 12 and 13:

xiGraph 2; Planned loans for 2003 8

- Page 15 and 16:

3(a) Identifyin g shortcomings, whi

- Page 17 and 18:

5The societ y ha s neve r undertake

- Page 19 and 20:

7(ii) Members participationMember's

- Page 21 and 22:

9created through unity of different

- Page 23 and 24:

11In Tanzania SACCOs are divided in

- Page 25 and 26:

13Microfinance i s the provision of

- Page 27 and 28:

15interruptions, cooperatives hav e

- Page 29 and 30:

17and responsibilities of other sta

- Page 31 and 32:

192.1.2 Developmen t of SACCOs in T

- Page 33 and 34:

21savings mean t puttin g asid e so

- Page 35 and 36:

23In som e rural areas especially a

- Page 37 and 38:

25According t o Kironde , J.M.L (19

- Page 39 and 40:

27(SACCOS) an d th e financia l Non

- Page 41 and 42:

29died of malaria, would that stop

- Page 43 and 44:

31A lo t have been written regardin

- Page 45 and 46: 33Another SACCOs visited in this ca

- Page 47 and 48: 35have yet to be developed. In gene

- Page 49 and 50: 37(i) B e able to identif y trainin

- Page 51 and 52: 39community in that area, their low

- Page 53 and 54: 41To hi s opinion, there has bee n

- Page 55 and 56: 43Many shortcoming s reporte d sho

- Page 57 and 58: 45In respec t o f SACCOs, th e micr

- Page 59 and 60: 47CHAPTER III3.0 RESEARCH METHODOLO

- Page 61 and 62: 493.2 Research approach and strateg

- Page 63 and 64: 51(c) Pas t experienceHaving worke

- Page 65 and 66: 53The recommendation s wil l b e sh

- Page 67 and 68: 554.1.1 INSTITUTIONA L ASSESSMENTTh

- Page 69 and 70: 57to 41% . These parameter s were u

- Page 71 and 72: 59a) Administrativ e policies and p

- Page 73 and 74: 614.1.1.2 Material and human resour

- Page 75 and 76: 63SharesKK als o invested in shares

- Page 77 and 78: 65who are not members of the Board

- Page 79 and 80: 67KK ha s survived many years of po

- Page 81 and 82: 69KK executiv e chairman is clearly

- Page 83 and 84: 71In our study findings above, it w

- Page 85 and 86: 73For those who were not satisfied,

- Page 87 and 88: 75financial reports are prepared an

- Page 89 and 90: 77minutes of the past annual genera

- Page 91 and 92: 79For proper safe keeping of money,

- Page 93 and 94: 81Table 11: Opinion for non-members

- Page 95: 83cooperative rules, which states;

- Page 99 and 100: 87Diversity of issued loan s i s ve

- Page 101 and 102: 89thinking of other economic develo

- Page 103 and 104: 91that from the salary received, he

- Page 105 and 106: 93The mone y requeste d t o b e wri

- Page 107 and 108: 95issued b y the Ban k o f Tanzania

- Page 109 and 110: 97KK charge s an interest of 1.5% p

- Page 111 and 112: 99activities an d se t targets . Fr

- Page 113 and 114: 1014.13.1 Finance and planning(a) A

- Page 115 and 116: 103information fo r financial state

- Page 117 and 118: 105In the study, when reviewing the

- Page 119 and 120: 107(a) 20% of net surplus eac h yea

- Page 121 and 122: 109year 1997 , 199 9 an d 2001 . Th

- Page 123 and 124: Illcontinued wit h same tradition,

- Page 125 and 126: 113(ii) Hig h level cooperative ill

- Page 127 and 128: 115Management can set some categori

- Page 129 and 130: 117mismanagement o f powers and res

- Page 131 and 132: 119knowledge to generate more incom

- Page 133 and 134: 121In Tanzania , SACCOs hav e regis

- Page 135 and 136: 123If KK management wil l immediate

- Page 137 and 138: 125policy. Th e organizatio n need

- Page 139 and 140: 127In cas e situation becomes diffi

- Page 141 and 142: 129BibiiograhyAdam Mwandeng a (2000