AUDIT ANALYTICS AUDIT

x8YaD9

x8YaD9

- No tags were found...

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

ESSAY 5: DATA <strong>ANALYTICS</strong> FOR FINANCIAL STATEMENT <strong>AUDIT</strong>S<br />

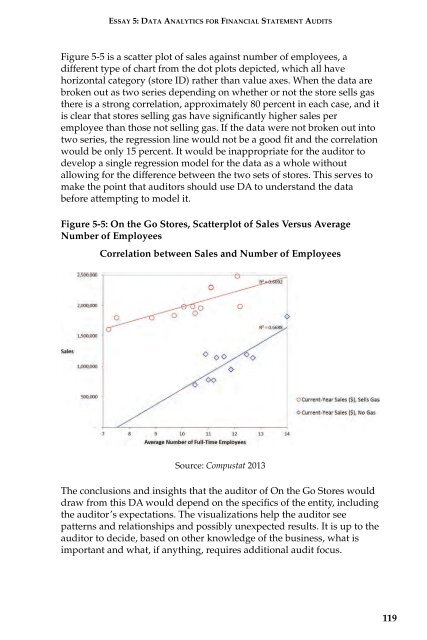

Figure 5-5 is a scatter plot of sales against number of employees, a<br />

different type of chart from the dot plots depicted, which all have<br />

horizontal category (store ID) rather than value axes. When the data are<br />

broken out as two series depending on whether or not the store sells gas<br />

there is a strong correlation, approximately 80 percent in each case, and it<br />

is clear that stores selling gas have significantly higher sales per<br />

employee than those not selling gas. If the data were not broken out into<br />

two series, the regression line would not be a good fit and the correlation<br />

would be only 15 percent. It would be inappropriate for the auditor to<br />

develop a single regression model for the data as a whole without<br />

allowing for the difference between the two sets of stores. This serves to<br />

make the point that auditors should use DA to understand the data<br />

before attempting to model it.<br />

Figure 5-5: On the Go Stores, Scatterplot of Sales Versus Average<br />

Number of Employees<br />

Correlation between Sales and Number of Employees<br />

Source: Compustat 2013<br />

The conclusions and insights that the auditor of On the Go Stores would<br />

draw from this DA would depend on the specifics of the entity, including<br />

the auditor’s expectations. The visualizations help the auditor see<br />

patterns and relationships and possibly unexpected results. It is up to the<br />

auditor to decide, based on other knowledge of the business, what is<br />

important and what, if anything, requires additional audit focus.<br />

119