AUDIT ANALYTICS AUDIT

x8YaD9

x8YaD9

- No tags were found...

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

<strong>AUDIT</strong> <strong>ANALYTICS</strong> AND CONTINUOUS <strong>AUDIT</strong>:LOOKING TOWARD THE FUTURE<br />

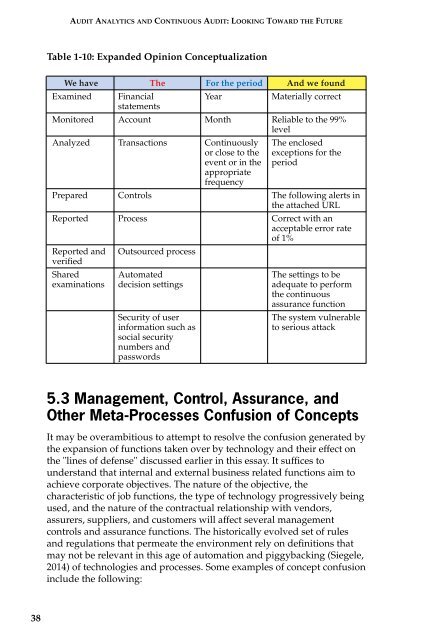

Table 1-10: Expanded Opinion Conceptualization<br />

We have The For the period And we found<br />

Examined<br />

Financial<br />

statements<br />

Year<br />

Materially correct<br />

Monitored Account Month Reliable to the 99%<br />

level<br />

Analyzed Transactions Continuously<br />

or close to the<br />

event or in the<br />

appropriate<br />

frequency<br />

The enclosed<br />

exceptions for the<br />

period<br />

Prepared Controls The following alerts in<br />

the attached URL<br />

Reported Process Correct with an<br />

acceptable error rate<br />

of 1%<br />

Reported and<br />

verified<br />

Outsourced process<br />

Shared<br />

examinations<br />

Automated<br />

decision settings<br />

Security of user<br />

information such as<br />

social security<br />

numbers and<br />

passwords<br />

The settings to be<br />

adequate to perform<br />

the continuous<br />

assurance function<br />

The system vulnerable<br />

to serious attack<br />

5.3 Management, Control, Assurance, and<br />

Other Meta-Processes Confusion of Concepts<br />

It may be overambitious to attempt to resolve the confusion generated by<br />

the expansion of functions taken over by technology and their effect on<br />

the "lines of defense" discussed earlier in this essay. It suffices to<br />

understand that internal and external business related functions aim to<br />

achieve corporate objectives. The nature of the objective, the<br />

characteristic of job functions, the type of technology progressively being<br />

used, and the nature of the contractual relationship with vendors,<br />

assurers, suppliers, and customers will affect several management<br />

controls and assurance functions. The historically evolved set of rules<br />

and regulations that permeate the environment rely on definitions that<br />

may not be relevant in this age of automation and piggybacking (Siegele,<br />

2014) of technologies and processes. Some examples of concept confusion<br />

include the following:<br />

38