AUDIT ANALYTICS AUDIT

x8YaD9

x8YaD9

- No tags were found...

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

CASE STUDY C: INCREASING <strong>AUDIT</strong> EFFICIENCY<br />

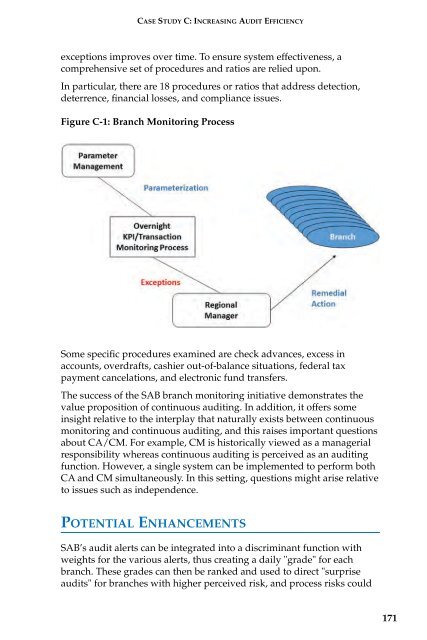

exceptions improves over time. To ensure system effectiveness, a<br />

comprehensive set of procedures and ratios are relied upon.<br />

In particular, there are 18 procedures or ratios that address detection,<br />

deterrence, financial losses, and compliance issues.<br />

Figure C-1: Branch Monitoring Process<br />

Some specific procedures examined are check advances, excess in<br />

accounts, overdrafts, cashier out-of-balance situations, federal tax<br />

payment cancelations, and electronic fund transfers.<br />

The success of the SAB branch monitoring initiative demonstrates the<br />

value proposition of continuous auditing. In addition, it offers some<br />

insight relative to the interplay that naturally exists between continuous<br />

monitoring and continuous auditing, and this raises important questions<br />

about CA/CM. For example, CM is historically viewed as a managerial<br />

responsibility whereas continuous auditing is perceived as an auditing<br />

function. However, a single system can be implemented to perform both<br />

CA and CM simultaneously. In this setting, questions might arise relative<br />

to issues such as independence.<br />

POTENTIAL ENHANCEMENTS<br />

SAB’s audit alerts can be integrated into a discriminant function with<br />

weights for the various alerts, thus creating a daily "grade" for each<br />

branch. These grades can then be ranked and used to direct "surprise<br />

audits" for branches with higher perceived risk, and process risks could<br />

171