AUDIT ANALYTICS AUDIT

x8YaD9

x8YaD9

- No tags were found...

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

<strong>AUDIT</strong> <strong>ANALYTICS</strong> AND CONTINUOUS <strong>AUDIT</strong>:LOOKING TOWARD THE FUTURE<br />

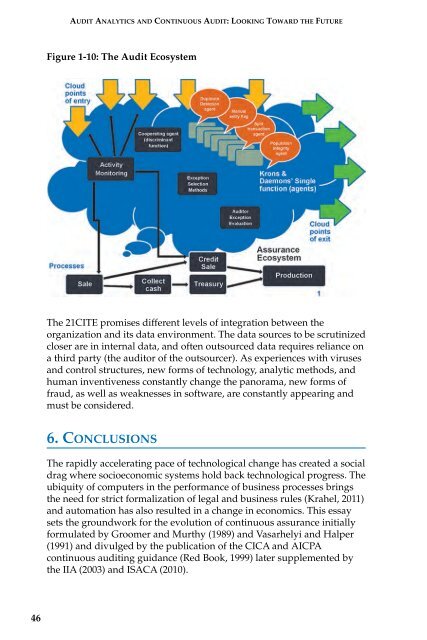

Figure 1-10: The Audit Ecosystem<br />

The 21CITE promises different levels of integration between the<br />

organization and its data environment. The data sources to be scrutinized<br />

closer are in internal data, and often outsourced data requires reliance on<br />

a third party (the auditor of the outsourcer). As experiences with viruses<br />

and control structures, new forms of technology, analytic methods, and<br />

human inventiveness constantly change the panorama, new forms of<br />

fraud, as well as weaknesses in software, are constantly appearing and<br />

must be considered.<br />

6. CONCLUSIONS<br />

The rapidly accelerating pace of technological change has created a social<br />

drag where socioeconomic systems hold back technological progress. The<br />

ubiquity of computers in the performance of business processes brings<br />

the need for strict formalization of legal and business rules (Krahel, 2011)<br />

and automation has also resulted in a change in economics. This essay<br />

sets the groundwork for the evolution of continuous assurance initially<br />

formulated by Groomer and Murthy (1989) and Vasarhelyi and Halper<br />

(1991) and divulged by the publication of the CICA and AICPA<br />

continuous auditing guidance (Red Book, 1999) later supplemented by<br />

the IIA (2003) and ISACA (2010).<br />

46