AUDIT ANALYTICS AUDIT

x8YaD9

x8YaD9

- No tags were found...

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

<strong>AUDIT</strong> <strong>ANALYTICS</strong> AND CONTINUOUS <strong>AUDIT</strong>:LOOKING TOWARD THE FUTURE<br />

business processes have become too complex to be efficiently addressed<br />

through pure human assurance. Layers of data, software, and the<br />

interconnection with upstream and downstream systems (and processes)<br />

make observation and evaluation very complex.<br />

In general an entirely new family of audit analytics is emerging 15 that can<br />

affect all parts of the audit engagement and can allow the use of an<br />

expanded data framework that includes external big data to support<br />

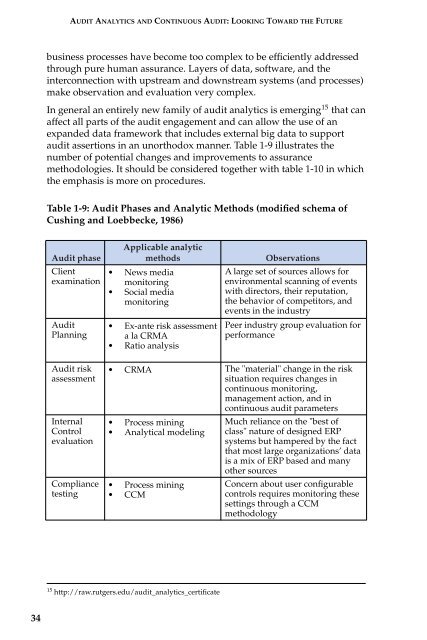

audit assertions in an unorthodox manner. Table 1-9 illustrates the<br />

number of potential changes and improvements to assurance<br />

methodologies. It should be considered together with table 1-10 in which<br />

the emphasis is more on procedures.<br />

Table 1-9: Audit Phases and Analytic Methods (modified schema of<br />

Cushing and Loebbecke, 1986)<br />

Audit phase<br />

Applicable analytic<br />

methods<br />

Client<br />

examination • News media<br />

monitoring<br />

• Social media<br />

monitoring<br />

Audit<br />

Planning<br />

• Ex-ante risk assessment<br />

alaCRMA<br />

• Ratio analysis<br />

Observations<br />

A large set of sources allows for<br />

environmental scanning of events<br />

with directors, their reputation,<br />

the behavior of competitors, and<br />

events in the industry<br />

Peer industry group evaluation for<br />

performance<br />

Audit risk<br />

assessment<br />

Internal<br />

Control<br />

evaluation<br />

Compliance<br />

testing<br />

• CRMA The "material" change in the risk<br />

situation requires changes in<br />

continuous monitoring,<br />

management action, and in<br />

continuous audit parameters<br />

• Process mining<br />

• Analytical modeling<br />

• Process mining<br />

• CCM<br />

Much reliance on the "best of<br />

class" nature of designed ERP<br />

systems but hampered by the fact<br />

that most large organizations’ data<br />

is a mix of ERP based and many<br />

other sources<br />

Concern about user configurable<br />

controls requires monitoring these<br />

settings through a CCM<br />

methodology<br />

15 http://raw.rutgers.edu/audit_analytics_certificate<br />

34