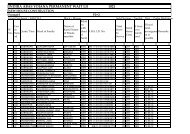

West Bengal Panchayat (Zilla Parishad and Panchayat Samiti ...

West Bengal Panchayat (Zilla Parishad and Panchayat Samiti ...

West Bengal Panchayat (Zilla Parishad and Panchayat Samiti ...

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

(12) At the close of each month, the Bank account <strong>and</strong> the Load Fund account as reflected in the Cash<br />

Book, shall be reconciled with Pass Book of the Bank <strong>and</strong> of the Treasury. Statements on such<br />

reconciliation shall be prepared accordingly in Form 11 <strong>and</strong> shall be preserved in a register to be<br />

maintained for the purpose.<br />

(13) The differences or the discrepancies detected in the statement as referred to in sub-rule (12), shall<br />

immediately be set right in case the mistake occurred in the <strong>Panchayat</strong> body. Otherwise, it shall immediately<br />

be brought to the notice of the Treasury Officer or the Manager of the Bank concerned <strong>and</strong> the discrepancies<br />

shall be reconciled. If the discrepancies still persist, the matter shall be brought to the notice of the District<br />

Magistrate by the <strong>Zilla</strong> <strong>Parishad</strong> or to the notice of the Sub-Divisional Officer by the <strong>Panchayat</strong> <strong>Samiti</strong><br />

immediately for settlement of such discrepancies. It is necessary that the discrepancy shall be brought to the<br />

notice of the Treasury or Bank, as the case may be, in the month following the month of transaction <strong>and</strong> that<br />

should be settled by personal contact with the Treasury or the Bank at appropriate level.<br />

(14)The Cash Book balance shall be analyzed at the close of the month showing balance of Fund <strong>and</strong><br />

position of cash, scheme-wise, head-wise or purpose-wise, available for utilization.<br />

Key Word: Subsidiary Cash Book<br />

22.<br />

(1) For any important scheme or programme, a subsidiary Cash Book may be maintained by the <strong>Zilla</strong><br />

<strong>Parishad</strong> or the <strong>Panchayat</strong> <strong>Samiti</strong> in Form 12 when so directed by the Funding authority with respect to any<br />

scheme or programme or when the <strong>Panchayat</strong> body considers it necessary <strong>and</strong> expedient to maintain a<br />

subsidiary Cash Book in relation to a scheme or a programme.<br />

(2) Provisions relating to maintenance of Cash Book as provided in rule 21 shall apply mutatis<br />

mut<strong>and</strong>is for maintenance of the subsidiary Cash Book.<br />

(3) Total receipt <strong>and</strong> expenditure recorded in the Subsidiary Cash Book for every month shall be brought<br />

into the principal Cash Book by recording such receipt or expenditure on the last working day of the month<br />

for the purpose of calculating the total Fund <strong>and</strong> for classification of the Fund scheme-wise <strong>and</strong> head-wise.<br />

(4) Cash drawn through self-cheque unless immediately disbursed may be recorded in the Liquid Cash Book<br />

by the cashier in Form 31, which shall be balanced, closed <strong>and</strong> physically verified at the close of a clay's<br />

transaction by the Drawing <strong>and</strong> Disbursing Officer<br />

Key Word: Security arrangement for carrying cash<br />

23.<br />

Responsibility for fetching or carrying cash shall not be given to a member of the Group-D staff<br />

unless it is necessary. When the amount exceeds rupees five hundred, another employee shall accompany the<br />

Cashier. The Cashier who brings the money shall be provided with a leather bag fitted with a lock <strong>and</strong> chain,<br />

which can be secured to his body. When a sum of rupees twenty five thous<strong>and</strong> or above amount is<br />

involved, armed police escorts may be provided with the Cashier for additional protection.<br />

Key Word: General Ledger<br />

24.<br />

(1) All financial transaction of the <strong>Zilla</strong> <strong>Parishad</strong> or the <strong>Panchayat</strong> <strong>Samiti</strong>, as the case<br />

may be, shall be recorded In the general ledger maintained as per Form 13 following the double<br />

entry system of book keeping.<br />

(2) Each account maintained in the general ledger shall be totalled every month to facilitate<br />

preparation of monthly <strong>and</strong> annual Receipts <strong>and</strong> Payment Account of the <strong>Zilla</strong> <strong>Parishad</strong> or the <strong>Panchayat</strong><br />

<strong>Samiti</strong>, as the case maybe. An illustrative list of heads of account by which Receipts <strong>and</strong> Payment<br />

Account of the <strong>Zilla</strong> <strong>Parishad</strong> or the <strong>Panchayat</strong> <strong>Samiti</strong> shall be prepared is furnished in ANNEXURE I.