FINANCE FOR ALL ? - Frankfurt School of Finance & Management

FINANCE FOR ALL ? - Frankfurt School of Finance & Management

FINANCE FOR ALL ? - Frankfurt School of Finance & Management

Erfolgreiche ePaper selbst erstellen

Machen Sie aus Ihren PDF Publikationen ein blätterbares Flipbook mit unserer einzigartigen Google optimierten e-Paper Software.

den Boom des Mikrokredits. Mit den Minidarlehen sollten auch die<br />

Ärmsten der Armen am wirtschaftlichen Aufschwung teilhaben,<br />

mit dem das Schwellenland seit Jahren beeindruckt. Wirtschaftswachstum<br />

und Entwicklung müssen nicht Hand in Hand gehen,<br />

das zeigt ein kürzlich veröffentlichter Artikel, den Wirtschaftsnobelpreisträger<br />

Amartya Sen zusammen mit Jean Drèze verfasst<br />

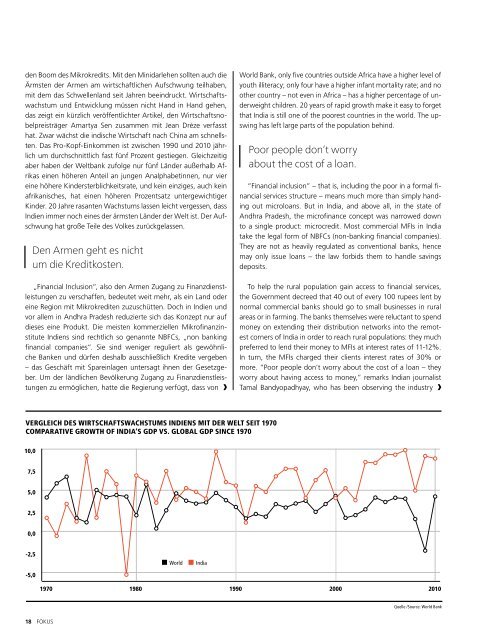

hat. Zwar wächst die indische Wirtschaft nach China am schnellsten.<br />

Das Pro-Kopf-Einkommen ist zwischen 1990 und 2010 jährlich<br />

um durchschnittlich fast fünf Prozent gestiegen. Gleichzeitig<br />

aber haben der Weltbank zufolge nur fünf Länder außerhalb Afrikas<br />

einen höheren Anteil an jungen Analphabetinnen, nur vier<br />

eine höhere Kindersterblichkeitsrate, und kein einziges, auch kein<br />

afrikanisches, hat einen höheren Prozentsatz untergewichtiger<br />

Kinder. 20 Jahre rasanten Wachstums lassen leicht vergessen, dass<br />

Indien immer noch eines der ärmsten Länder der Welt ist. Der Aufschwung<br />

hat große Teile des Volkes zurückgelassen.<br />

Den Armen geht es nicht<br />

um die Kreditkosten.<br />

„Financial Inclusion“, also den Armen Zugang zu Finanzdienstleistungen<br />

zu verschaffen, bedeutet weit mehr, als ein Land oder<br />

eine Region mit Mikrokrediten zuzuschütten. Doch in Indien und<br />

vor allem in Andhra Pradesh reduzierte sich das Konzept nur auf<br />

dieses eine Produkt. Die meisten kommerziellen Mikr<strong>of</strong>inanzinstitute<br />

Indiens sind rechtlich so genannte NBFCs, „non banking<br />

financial companies“. Sie sind weniger reguliert als gewöhnliche<br />

Banken und dürfen deshalb ausschließlich Kredite vergeben<br />

– das Geschäft mit Spareinlagen untersagt ihnen der Gesetzgeber.<br />

Um der ländlichen Bevölkerung Zugang zu Finanzdienstleistungen<br />

zu ermöglichen, hatte die Regierung verfügt, dass von<br />

World Bank, only five countries outside Africa have a higher level <strong>of</strong><br />

youth illiteracy; only four have a higher infant mortality rate; and no<br />

other country – not even in Africa – has a higher percentage <strong>of</strong> underweight<br />

children. 20 years <strong>of</strong> rapid growth make it easy to forget<br />

that India is still one <strong>of</strong> the poorest countries in the world. The upswing<br />

has left large parts <strong>of</strong> the population behind.<br />

Poor people don’t worry<br />

about the cost <strong>of</strong> a loan.<br />

“Financial inclusion” – that is, including the poor in a formal financial<br />

services structure – means much more than simply handing<br />

out microloans. But in India, and above all, in the state <strong>of</strong><br />

Andhra Pradesh, the micr<strong>of</strong>inance concept was narrowed down<br />

to a single product: microcredit. Most commercial MFIs in India<br />

take the legal form <strong>of</strong> NBFCs (non-banking financial companies).<br />

They are not as heavily regulated as conventional banks, hence<br />

may only issue loans – the law forbids them to handle savings<br />

deposits.<br />

To help the rural population gain access to financial services,<br />

the Government decreed that 40 out <strong>of</strong> every 100 rupees lent by<br />

normal commercial banks should go to small businesses in rural<br />

areas or in farming. The banks themselves were reluctant to spend<br />

money on extending their distribution networks into the remotest<br />

corners <strong>of</strong> India in order to reach rural populations: they much<br />

preferred to lend their money to MFIs at interest rates <strong>of</strong> 11-12%.<br />

In turn, the MFIs charged their clients interest rates <strong>of</strong> 30% or<br />

more. “Poor people don’t worry about the cost <strong>of</strong> a loan – they<br />

worry about having access to money,” remarks Indian journalist<br />

Tamal Bandyopadhyay, who has been observing the industry<br />

Vergleich des WirtschaftswachstumS Indiens mit der Welt seit 1970<br />

Comparative growth <strong>of</strong> India’s GDP vs. global GDP since 1970<br />

10,0<br />

7,5<br />

5,0<br />

2,5<br />

0,0<br />

-2,5<br />

-5,0<br />

World<br />

India<br />

1970<br />

1980 1990 2000 2010<br />

Quelle /Source: World Bank<br />

18 FOKUS