FINANCE FOR ALL ? - Frankfurt School of Finance & Management

FINANCE FOR ALL ? - Frankfurt School of Finance & Management

FINANCE FOR ALL ? - Frankfurt School of Finance & Management

Sie wollen auch ein ePaper? Erhöhen Sie die Reichweite Ihrer Titel.

YUMPU macht aus Druck-PDFs automatisch weboptimierte ePaper, die Google liebt.

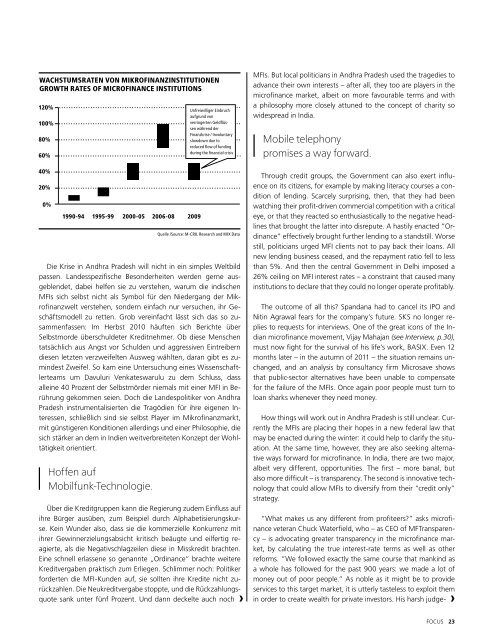

WachstumsRATEN VON Mikr<strong>of</strong>inanzinstitutionen<br />

GROWTH RATES OF Micr<strong>of</strong>inance institutions<br />

120% Unfreiwilliger Einbruch<br />

aufgrund von<br />

100%<br />

verringerten Geldflüssen<br />

während der<br />

Finanzkrise / Involuntary<br />

80%<br />

slowdown due to<br />

reduced flow <strong>of</strong> funding<br />

during the financial crisis<br />

60%<br />

40%<br />

20%<br />

0%<br />

1990-94 1995-99 2000-05 2006-08 2009<br />

Die Krise in Andhra Pradesh will nicht in ein simples Weltbild<br />

passen. Landesspezifische Besonderheiten werden gerne ausgeblendet,<br />

dabei helfen sie zu verstehen, warum die indischen<br />

MFIs sich selbst nicht als Symbol für den Niedergang der Mikr<strong>of</strong>inanzwelt<br />

verstehen, sondern einfach nur versuchen, ihr Geschäftsmodell<br />

zu retten. Grob vereinfacht lässt sich das so zusammenfassen:<br />

Im Herbst 2010 häuften sich Berichte über<br />

Selbstmorde überschuldeter Kreditnehmer. Ob diese Menschen<br />

tatsächlich aus Angst vor Schulden und aggressiven Eintreibern<br />

diesen letzten verzweifelten Ausweg wählten, daran gibt es zumindest<br />

Zweifel. So kam eine Untersuchung eines Wissenschaftlerteams<br />

um Davuluri Venkateswarulu zu dem Schluss, dass<br />

alleine 40 Prozent der Selbstmörder niemals mit einer MFI in Berührung<br />

gekommen seien. Doch die Landespolitiker von Andhra<br />

Pradesh instrumentalisierten die Tragödien für ihre eigenen Interessen,<br />

schließlich sind sie selbst Player im Mikr<strong>of</strong>inanzmarkt,<br />

mit günstigeren Konditionen allerdings und einer Philosophie, die<br />

sich stärker an dem in Indien weitverbreiteten Konzept der Wohltätigkeit<br />

orientiert.<br />

H<strong>of</strong>fen auf<br />

Mobilfunk-Technologie.<br />

Quelle /Source: M-CRIL Research and MIX Data<br />

Über die Kreditgruppen kann die Regierung zudem Einfluss auf<br />

ihre Bürger ausüben, zum Beispiel durch Alphabetisierungskurse.<br />

Kein Wunder also, dass sie die kommerzielle Konkurrenz mit<br />

ihrer Gewinnerzielungsabsicht kritisch beäugte und eilfertig reagierte,<br />

als die Negativschlagzeilen diese in Misskredit brachten.<br />

Eine schnell erlassene so genannte „Ordinance“ brachte weitere<br />

Kreditvergaben praktisch zum Erliegen. Schlimmer noch: Politiker<br />

forderten die MFI-Kunden auf, sie sollten ihre Kredite nicht zurückzahlen.<br />

Die Neukreditvergabe stoppte, und die Rückzahlungsquote<br />

sank unter fünf Prozent. Und dann deckelte auch noch<br />

MFIs. But local politicians in Andhra Pradesh used the tragedies to<br />

advance their own interests – after all, they too are players in the<br />

micr<strong>of</strong>inance market, albeit on more favourable terms and with<br />

a philosophy more closely attuned to the concept <strong>of</strong> charity so<br />

widespread in India.<br />

Mobile telephony<br />

promises a way forward.<br />

Through credit groups, the Government can also exert influence<br />

on its citizens, for example by making literacy courses a condition<br />

<strong>of</strong> lending. Scarcely surprising, then, that they had been<br />

watching their pr<strong>of</strong>it-driven commercial competition with a critical<br />

eye, or that they reacted so enthusiastically to the negative headlines<br />

that brought the latter into disrepute. A hastily enacted “Ordinance”<br />

effectively brought further lending to a standstill. Worse<br />

still, politicians urged MFI clients not to pay back their loans. All<br />

new lending business ceased, and the repayment ratio fell to less<br />

than 5%. And then the central Government in Delhi imposed a<br />

26% ceiling on MFI interest rates – a constraint that caused many<br />

institutions to declare that they could no longer operate pr<strong>of</strong>itably.<br />

The outcome <strong>of</strong> all this? Spandana had to cancel its IPO and<br />

Nitin Agrawal fears for the company’s future. SKS no longer replies<br />

to requests for interviews. One <strong>of</strong> the great icons <strong>of</strong> the Indian<br />

micr<strong>of</strong>inance movement, Vijay Mahajan (see Interview, p.30),<br />

must now fight for the survival <strong>of</strong> his life’s work, BASIX. Even 12<br />

months later – in the autumn <strong>of</strong> 2011 – the situation remains unchanged,<br />

and an analysis by consultancy firm Microsave shows<br />

that public-sector alternatives have been unable to compensate<br />

for the failure <strong>of</strong> the MFIs. Once again poor people must turn to<br />

loan sharks whenever they need money.<br />

How things will work out in Andhra Pradesh is still unclear. Currently<br />

the MFIs are placing their hopes in a new federal law that<br />

may be enacted during the winter: it could help to clarify the situation.<br />

At the same time, however, they are also seeking alternative<br />

ways forward for micr<strong>of</strong>inance. In India, there are two major,<br />

albeit very different, opportunities. The first – more banal, but<br />

also more difficult – is transparency. The second is innovative technology<br />

that could allow MFIs to diversify from their “credit only”<br />

strategy.<br />

“What makes us any different from pr<strong>of</strong>iteers?” asks micr<strong>of</strong>inance<br />

veteran Chuck Waterfield, who – as CEO <strong>of</strong> MFTransparency<br />

– is advocating greater transparency in the micr<strong>of</strong>inance market,<br />

by calculating the true interest-rate terms as well as other<br />

reforms. “We followed exactly the same course that mankind as<br />

a whole has followed for the past 900 years: we made a lot <strong>of</strong><br />

money out <strong>of</strong> poor people.” As noble as it might be to provide<br />

services to this target market, it is utterly tasteless to exploit them<br />

in order to create wealth for private investors. His harsh judge-<br />

FOCUS<br />

23