Exhibit 2.7 Value of World Imports of Cut Flowers and Market Share of the Top Four Importing Countries 1984-1988 1984 Imports - $1.29 Billion 1985 Imports - $1.30 Billion W Germany 40% 3e% NetNrerianis Netnerianca 5% 4 7% .... in, ton3Slaie5s( United Slates tn: 22% 21% Oltmer Countries 28% Other Count riesi 21310 Neith erancjs Uniled Slates 1986 Imports - $1.74 Billion W Gernmany 38% 1987 Imoorts - $2.22 Billion 1988 Import- $2.52 Billion W Glrmany W Germany 38%t 35t 101 N~teelncis Ne lnret nc 8 5% United States 14%MH:...... 12 32% United 1awes France 384 0

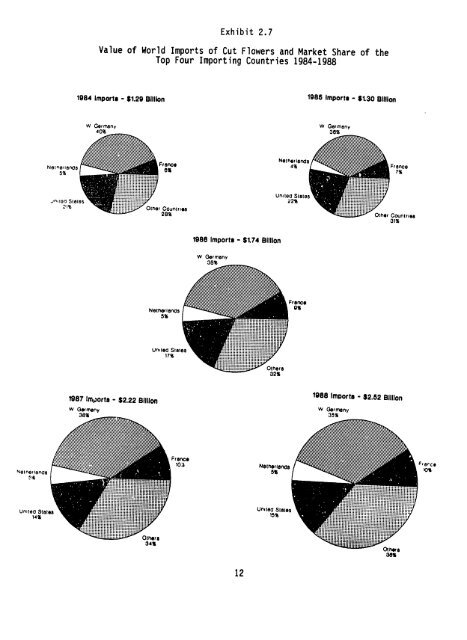

ises in the level of imports were also recorded for carnation and other flowers in terms of both volume and value. Although much of this increase is attributable to the Netherlands, there remain clear opportunities for developing country suppliers able to compete with the reliability of service and quality provided by traders in the Netherlands. The United States is the only major importer whose primary supply of cut flower imports is from a developing country, namely Colombia, which shipped $175.6 million worth of cut flowers, or 62 percent of total U.S. imports of $283.5 million in 1988. The Netherlands is the second most important supplier with $63.6 million of U.S imports, or 22 percent of the market, followed by Mexico, Canada, Costa Rica, Israel, Ecuador, Peru, and Thailand with a total of $32.7 million, or 11.5 percent. Other countries that represent potentially lucrative markets are the United Kingdom and Switzerland. The United Kingdom has registered the greatest growth in its share of world imports, from $73.7 million, or 5.7 percent of world imports in 1984, to $230.3 million, or 9.1 percent in 1988. With the secoq highest per capita spending on cut flowers in the world after Japan, Switzerland isan important importer of roses and carnations, primarily from the Netherlands and Italy. The ITC report states, "Inspite of strong competition, some developin 9 countries have been successful in entering the Swiss market in recent years."1,1 Morocco, for example, has increased the value of its rose exports to Switzerland from $95,000 in 1985 to $669,000 in 1988. 2.2 Market Trends and Preferences 2.2.1 Consumer Preferences One of the most important .factors determining market demand for cut flowers isthe celebration of special occasions, such as religious holidays. In France, for example, chrysanthemums are purchased for All Saints Day (November 1), all flowers for Christmas and New Year's, roses for Valentine's Day (February 14), lilies of the valley for May 1, and roses and other flowers for Mother's Day (last Sunday of May). The most popular cut flowers in France are roses, carnations, tulips, chrysanthemums, and gladioli, in that order . Winter demand for flowers tends to be very strong in other European countries also because of special occasion purchases. Inthe Netherlands, where per capita consumption ishigh, consumers purchase flowers year-round (especially chrysanthemu~ms, followed by roses, carnations, freesias, and tulips) and often 13 ITC report, p. 68. 14 The Flower Council of Holland. 15 ITC, p. 201. 16 L'Or Vert, No. 160, October 1990, p. 7. 13

- Page 1 and 2: APIP Agricultural Policy Implementa

- Page 3 and 4: TABLE OF CONTENTS EXECUTIVE SUMMARY

- Page 5 and 6: LIST OF EXHIBITS Exhibit 2.1 Major

- Page 7 and 8: orchids, gladioli and tulips are th

- Page 9 and 10: high yields. Overall, therefore, th

- Page 11 and 12: 1.1 Study Objectives 1. INTRODUCTIO

- Page 13 and 14: covered seven major importing count

- Page 15 and 16: 2. WORLD TRADE IN CUT FLOWERS AND T

- Page 17 and 18: to all the major importing countrie

- Page 19 and 20: 7 6 5 4 3 2 1 0 Millions of US$ Sou

- Page 21: Exhibit 2.6 Value of World Imports

- Page 25 and 26: Many of the European countries, suc

- Page 27 and 28: in both activities. Finally, there

- Page 29 and 30: These prices are for "extra" qualit

- Page 31 and 32: Exhibit 3.1 List of Selected Grower

- Page 33 and 34: grow flowers to sell intheir stalls

- Page 35 and 36: flowers. Tunisian growers' willingn

- Page 37 and 38: timing and coordination of loading

- Page 39 and 40: distinguish it in the market (unlik

- Page 41 and 42: profitable, assuming that high yiel

- Page 43 and 44: 4.2 Cash Flow Analysis Exhibit 4.3

- Page 45 and 46: ',,-t r,,VW AINLY5 o I 4 UR CARNATI

- Page 47 and 48: uj CASH INFLOW Yield Price Value of

- Page 49 and 50: CASH INFLOW Yield Price Vslc of ToW

- Page 51 and 52: , . CASH INFLOW Yield Price Value o

- Page 53 and 54: 5. TUNISIAN GOVERNMENT AGENCIES AND

- Page 55 and 56: equired so much time. In an effort

- Page 57 and 58: 6.0 CONCLUSIONS AND RECONNENDATIONS

- Page 59 and 60: 7. Work with government and foreign

- Page 61 and 62: production is expensive because it

- Page 63 and 64: ANNEXES 53

- Page 65 and 66: The following solutions were offere

- Page 67 and 68: Miscellaneous maintenance (buying v

- Page 69 and 70: ANNEX 2-A ASSUMPTIONS FOR CALCULATI

- Page 71 and 72: Pesticide Costs: Lannate 21.0 DT/kg

- Page 73 and 74:

GLADIOLA- ENTERPRISE BUDGET, LOW/ME

- Page 75 and 76:

ANNEX 3 ISSUES RELATED TO POST-HARV

- Page 77 and 78:

Acaricides: Kelthane 0,2 1/hl Systb

- Page 79 and 80:

Mildrion: Manbbe 160 g/hl Zin~be 20

- Page 81 and 82:

LE GERBERA GERBERA JAMESONII FAKILL

- Page 83 and 84:

LE GLAIEUL GLADIOLUS FAMILLE DES IR

- Page 85 and 86:

O Annex b Quality Required by the C

- Page 87 and 88:

ii) Categorie U1 10 % des fleurs co

- Page 89 and 90:

RE7UMLI93B TUMISI MIC KINISTE E DE

- Page 91 and 92:

IPARTICIPANTS I ADRESSE TELEPHONE V

- Page 93 and 94:

IPA.TIC!PANTS I ADRESSE TELEPHONE I

- Page 95 and 96:

Wholesalers/Importers ANNEX 8 PERSO

- Page 97 and 98:

APIP Agricultural Policy Implementa

- Page 99 and 100:

Abet Jacques 43, Avenue du Cimetibr

- Page 101 and 102:

Ariaflor Box 147 - Fleurs 4 M.I.N.

- Page 103 and 104:

Berry Fleurs SARI Ruelle des Gats P

- Page 105 and 106:

Briois Christine 219, All6e des Oei

- Page 107 and 108:

Cochet Thierry SARL 160, AII6e des

- Page 109 and 110:

David Barthdlmy Charlin; Delamare G

- Page 111 and 112:

I Dia - Fleurs Box no 2 - SICA - Ma

- Page 113 and 114:

Fleurassistance GlE 149, Avenue des

- Page 115 and 116:

Flora Partner SA 23, rue Nicot 3300

- Page 117 and 118:

Galoppe Christine 135, AII6e des Oe

- Page 119 and 120:

Granier Michel Ets 28, Avenue Pierr

- Page 121 and 122:

Iris 200 199, AII6e des GlaTeuls 20

- Page 123 and 124:

Landes Fleurs SARL 44, Boulevard de

- Page 125 and 126:

Lotte et Cie Magnon Ets 59, AIIde d

- Page 127 and 128:

Marcucci G6rard SARL 4, rue Layriss

- Page 129 and 130:

Minnaar Fleurs SARL Moreau Th6r~se

- Page 131 and 132:

Olivreau SARL 220, A1l6e des Oeille

- Page 133 and 134:

Penja 260, A116 des Arums 94644- RU

- Page 135 and 136:

Pierlot et Cia 259, AlMa des Oeille

- Page 137 and 138:

I Roata - Pignet SA ROA TA . PIGNE

- Page 139 and 140:

La Roseraie 51, AII6e des Arums 941

- Page 141 and 142:

Salanque Flours Domaine Sainte Eug6

- Page 143 and 144:

Silva Flor St6 Aquitaine de Diffusi

- Page 145 and 146:

Sodlh Monpalasir 47320 - BOURRAN T6

- Page 147:

Vettese Jean Fleurs 360 112, AIl6e