Annual Report 2007

Annual Report 2007

Annual Report 2007

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

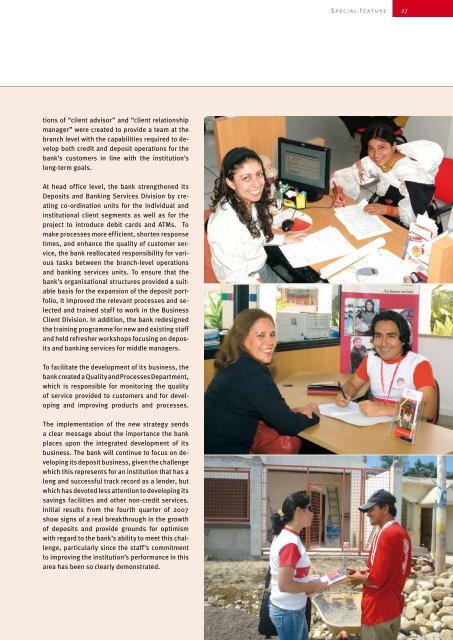

tions of “client advisor” and “client relationship<br />

manager” were created to provide a team at the<br />

branch level with the capabilities required to develop<br />

both credit and deposit operations for the<br />

bank’s customers in line with the institution’s<br />

long-term goals.<br />

At head office level, the bank strengthened its<br />

Deposits and Banking Services Division by creating<br />

co-ordination units for the individual and<br />

institutional client segments as well as for the<br />

project to introduce debit cards and ATMs. To<br />

make processes more efficient, shorten response<br />

times, and enhance the quality of customer service,<br />

the bank reallocated responsibility for various<br />

tasks between the branch-level operations<br />

and banking services units. To ensure that the<br />

bank’s organisational structures provided a suitable<br />

basis for the expansion of the deposit portfolio,<br />

it improved the relevant processes and selected<br />

and trained staff to work in the Business<br />

Client Division. In addition, the bank redesigned<br />

the training programme for new and existing staff<br />

and held refresher workshops focusing on deposits<br />

and banking services for middle managers.<br />

To facilitate the development of its business, the<br />

bankcreatedaQualityandProcessesDepartment,<br />

which is responsible for monitoring the quality<br />

of service provided to customers and for developing<br />

and improving products and processes.<br />

The implementation of the new strategy sends<br />

a clear message about the importance the bank<br />

places upon the integrated development of its<br />

business. The bank will continue to focus on developing<br />

its deposit business, given the challenge<br />

which this represents for an institution that has a<br />

long and successful track record as a lender, but<br />

which has devoted less attention to developing its<br />

savings facilities and other non-credit services.<br />

Initial results from the fourth quarter of <strong>2007</strong><br />

show signs of a real breakthrough in the growth<br />

of deposits and provide grounds for optimism<br />

with regard to the bank’s ability to meet this challenge,<br />

particularly since the staff’s commitment<br />

to improving the institution’s performance in this<br />

area has been so clearly demonstrated.<br />

S p e c i a l F e at u r e