Empirical Evaluation of Hybrid Defaultable Bond Pricing ... - risklab

Empirical Evaluation of Hybrid Defaultable Bond Pricing ... - risklab

Empirical Evaluation of Hybrid Defaultable Bond Pricing ... - risklab

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

E(t, T ))/(T − t). Therefore, w ensures the empirically validated negatively correlated<br />

relationship between spreads and non-defaultable short rates (see also<br />

Bakshi, Madan & Zhang (2001b)).<br />

If we estimate the parameters using the data speciÞed in Section 2 by application<br />

<strong>of</strong> Kalman Þlter techniques we get the estimates as speciÞed in Tables 3<br />

and 4.<br />

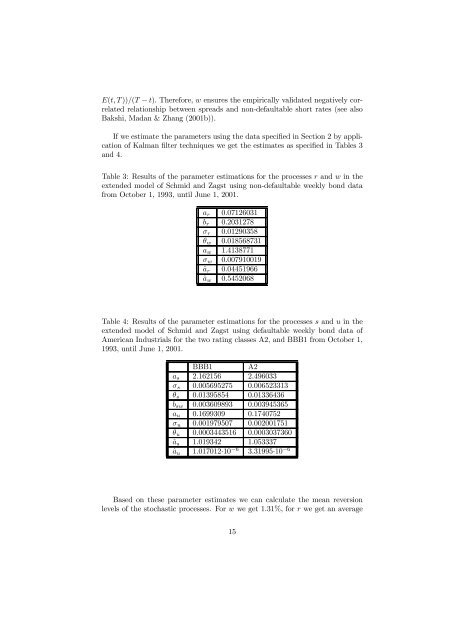

Table 3: Results <strong>of</strong> the parameter estimations for the processes r and w in the<br />

extended model <strong>of</strong> Schmid and Zagst using non-defaultable weekly bond data<br />

from October 1, 1993, until June 1, 2001.<br />

a r 0.07126031<br />

b r 0.2031278<br />

σ r 0.01290358<br />

θ w 0.018568731<br />

a w 1.4138771<br />

σ w 0.007910019<br />

â r 0.04451966<br />

â w 0.5452068<br />

Table 4: Results <strong>of</strong> the parameter estimations for the processes s and u in the<br />

extended model <strong>of</strong> Schmid and Zagst using defaultable weekly bond data <strong>of</strong><br />

American Industrials for the two rating classes A2, and BBB1 from October 1,<br />

1993, until June 1, 2001.<br />

BBB1 A2<br />

a s 2.162156 2.496033<br />

σ s 0.005695275 0.006523313<br />

θ s 0.01395854 0.01336436<br />

b sw 0.003609893 0.003945365<br />

a u 0.1699309 0.1740752<br />

σ u 0.001979507 0.002001751<br />

θ u 0.0003443516 0.0003037360<br />

â s 1.019342 1.053337<br />

â u 1.017012·10 −6 3.31995·10 −6<br />

Based on these parameter estimates we can calculate the mean reversion<br />

levels <strong>of</strong> the stochastic processes. For w we get 1.31%, for r we get an average<br />

15