D2 3 Computing e-Infrastructure cost calculations and business _models_vam1-final

D2 3 Computing e-Infrastructure cost calculations and business _models_vam1-final

D2 3 Computing e-Infrastructure cost calculations and business _models_vam1-final

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

e-‐FISCAL: www.efiscal.eu <br />

EC Contract Number: 283449 <br />

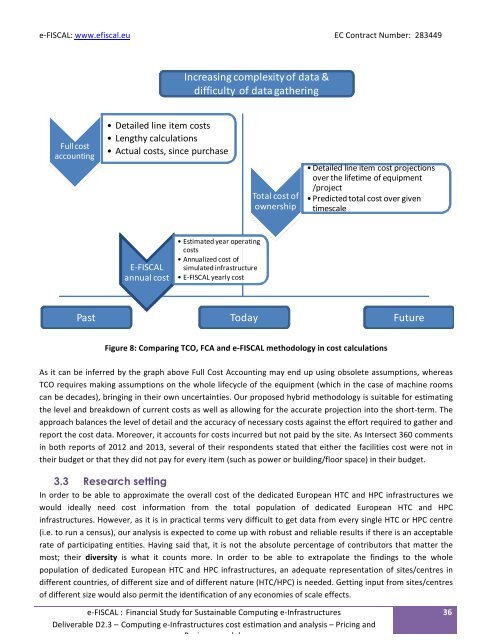

Increasing complexity of data & <br />

difficulty of data gathering <br />

Full <strong>cost</strong> <br />

accounting<br />

• Detailed line item <strong>cost</strong>s <br />

• Lengthy <strong>calculations</strong><br />

• Actual <strong>cost</strong>s, since purchase<br />

Total <strong>cost</strong> of <br />

ownership<br />

• Detailed line item <strong>cost</strong> projections <br />

over the lifetime of equipment <br />

/project<br />

• Predicted total <strong>cost</strong> over given <br />

timescale<br />

E-‐FISCAL <br />

annual <strong>cost</strong><br />

• Estimated year operating <br />

<strong>cost</strong>s<br />

• Annualized <strong>cost</strong> of <br />

simulated infrastructure<br />

• E-‐FISCAL yearly <strong>cost</strong><br />

Past <br />

Today <br />

Future <br />

Figure 8: Comparing TCO, FCA <strong>and</strong> e-‐FISCAL methodology in <strong>cost</strong> <strong>calculations</strong> <br />

As it can be inferred by the graph above Full Cost Accounting may end up using obsolete assumptions, whereas <br />

TCO requires making assumptions on the whole lifecycle of the equipment (which in the case of machine rooms <br />

can be decades), bringing in their own uncertainties. Our proposed hybrid methodology is suitable for estimating <br />

the level <strong>and</strong> breakdown of current <strong>cost</strong>s as well as allowing for the accurate projection into the short-‐term. The <br />

approach balances the level of detail <strong>and</strong> the accuracy of necessary <strong>cost</strong>s against the effort required to gather <strong>and</strong> <br />

report the <strong>cost</strong> data. Moreover, it accounts for <strong>cost</strong>s incurred but not paid by the site. As Intersect 360 comments <br />

in both reports of 2012 <strong>and</strong> 2013, several of their respondents stated that either the facilities <strong>cost</strong> were not in <br />

their budget or that they did not pay for every item (such as power or building/floor space) in their budget. <br />

3.3 Research setting<br />

In order to be able to approximate the overall <strong>cost</strong> of the dedicated European HTC <strong>and</strong> HPC infrastructures we <br />

would ideally need <strong>cost</strong> information from the total population of dedicated European HTC <strong>and</strong> HPC <br />

infrastructures. However, as it is in practical terms very difficult to get data from every single HTC or HPC centre <br />

(i.e. to run a census), our analysis is expected to come up with robust <strong>and</strong> reliable results if there is an acceptable <br />

rate of participating entities. Having said that, it is not the absolute percentage of contributors that matter the <br />

most; their diversity is what it counts more. In order to be able to extrapolate the findings to the whole <br />

population of dedicated European HTC <strong>and</strong> HPC infrastructures, an adequate representation of sites/centres in <br />

different countries, of different size <strong>and</strong> of different nature (HTC/HPC) is needed. Getting input from sites/centres <br />

of different size would also permit the identification of any economies of scale effects. <br />

e-‐FISCAL : Financial Study for Sustainable <strong>Computing</strong> e-‐<strong>Infrastructure</strong>s <br />

Deliverable <strong>D2</strong>.3 – <strong>Computing</strong> e-‐<strong>Infrastructure</strong>s <strong>cost</strong> estimation <strong>and</strong> analysis – Pricing <strong>and</strong> <br />

Business <strong>models</strong> <br />

36