D2 3 Computing e-Infrastructure cost calculations and business _models_vam1-final

D2 3 Computing e-Infrastructure cost calculations and business _models_vam1-final

D2 3 Computing e-Infrastructure cost calculations and business _models_vam1-final

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

e-‐FISCAL: www.efiscal.eu <br />

EC Contract Number: 283449 <br />

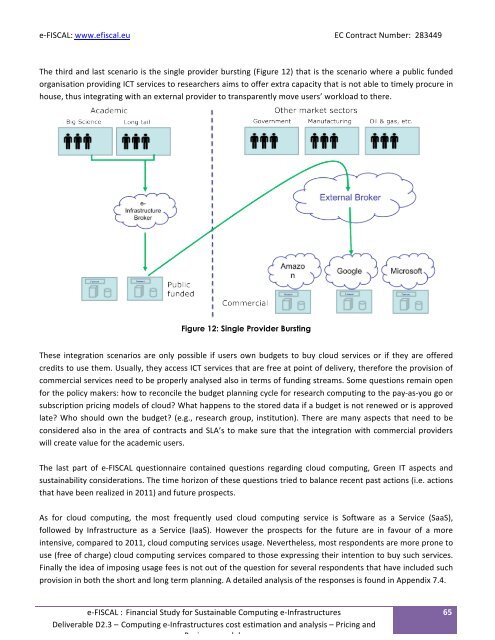

The third <strong>and</strong> last scenario is the single provider bursting (Figure 12) that is the scenario where a public funded <br />

organisation providing ICT services to researchers aims to offer extra capacity that is not able to timely procure in <br />

house, thus integrating with an external provider to transparently move users’ workload to there. <br />

Figure 12: Single Provider Bursting<br />

These integration scenarios are only possible if users own budgets to buy cloud services or if they are offered <br />

credits to use them. Usually, they access ICT services that are free at point of delivery, therefore the provision of <br />

commercial services need to be properly analysed also in terms of funding streams. Some questions remain open <br />

for the policy makers: how to reconcile the budget planning cycle for research computing to the pay-‐as-‐you go or <br />

subscription pricing <strong>models</strong> of cloud? What happens to the stored data if a budget is not renewed or is approved <br />

late? Who should own the budget? (e.g., research group, institution). There are many aspects that need to be <br />

considered also in the area of contracts <strong>and</strong> SLA’s to make sure that the integration with commercial providers <br />

will create value for the academic users. <br />

The last part of e-‐FISCAL questionnaire contained questions regarding cloud computing, Green IT aspects <strong>and</strong> <br />

sustainability considerations. The time horizon of these questions tried to balance recent past actions (i.e. actions <br />

that have been realized in 2011) <strong>and</strong> future prospects. <br />

As for cloud computing, the most frequently used cloud computing service is Software as a Service (SaaS), <br />

followed by <strong>Infrastructure</strong> as a Service (IaaS). However the prospects for the future are in favour of a more <br />

intensive, compared to 2011, cloud computing services usage. Nevertheless, most respondents are more prone to <br />

use (free of charge) cloud computing services compared to those expressing their intention to buy such services. <br />

Finally the idea of imposing usage fees is not out of the question for several respondents that have included such <br />

provision in both the short <strong>and</strong> long term planning. A detailed analysis of the responses is found in Appendix 7.4. <br />

e-‐FISCAL : Financial Study for Sustainable <strong>Computing</strong> e-‐<strong>Infrastructure</strong>s <br />

Deliverable <strong>D2</strong>.3 – <strong>Computing</strong> e-‐<strong>Infrastructure</strong>s <strong>cost</strong> estimation <strong>and</strong> analysis – Pricing <strong>and</strong> <br />

Business <strong>models</strong> <br />

65