Powering the Future Summary Report - Parsons Brinckerhoff

Powering the Future Summary Report - Parsons Brinckerhoff

Powering the Future Summary Report - Parsons Brinckerhoff

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

<strong>Powering</strong> <strong>the</strong> <strong>Future</strong> <strong>Summary</strong> <strong>Report</strong><br />

<strong>Powering</strong> <strong>the</strong> <strong>Future</strong> <strong>Summary</strong> <strong>Report</strong><br />

Findings<br />

1. The scale and urgency of <strong>the</strong> challenge.<br />

Achieving <strong>the</strong> 80% reduction in CO 2 emissions<br />

mandated by <strong>the</strong> Climate Change Act 2008 is<br />

feasible but extraordinarily challenging. It will<br />

require urgent and large-scale effort in every sector<br />

of <strong>the</strong> UK, and a delay in any sector will jeopardise<br />

<strong>the</strong> commitment.<br />

2. Leadership. The scale and rate of change<br />

required across all sectors to achieve <strong>the</strong> desired<br />

reductions in CO 2 emissions are such that market<br />

mechanisms will require strong leadership from<br />

government to be effective.<br />

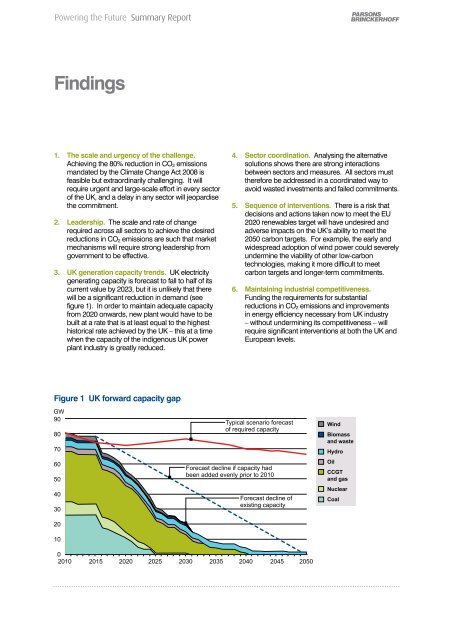

3. UK generation capacity trends. UK electricity<br />

generating capacity is forecast to fall to half of its<br />

current value by 2023, but it is unlikely that <strong>the</strong>re<br />

will be a significant reduction in demand (see<br />

figure 1). In order to maintain adequate capacity<br />

from 2020 onwards, new plant would have to be<br />

built at a rate that is at least equal to <strong>the</strong> highest<br />

historical rate achieved by <strong>the</strong> UK – this at a time<br />

when <strong>the</strong> capacity of <strong>the</strong> indigenous UK power<br />

plant industry is greatly reduced.<br />

4. Sector coordination. Analysing <strong>the</strong> alternative<br />

solutions shows <strong>the</strong>re are strong interactions<br />

between sectors and measures. All sectors must<br />

<strong>the</strong>refore be addressed in a coordinated way to<br />

avoid wasted investments and failed commitments.<br />

5. Sequence of interventions. There is a risk that<br />

decisions and actions taken now to meet <strong>the</strong> EU<br />

2020 renewables target will have undesired and<br />

adverse impacts on <strong>the</strong> UK’s ability to meet <strong>the</strong><br />

2050 carbon targets. For example, <strong>the</strong> early and<br />

widespread adoption of wind power could severely<br />

undermine <strong>the</strong> viability of o<strong>the</strong>r low-carbon<br />

technologies, making it more difficult to meet<br />

carbon targets and longer-term commitments.<br />

6. Maintaining industrial competitiveness.<br />

Funding <strong>the</strong> requirements for substantial<br />

reductions in CO 2 emissions and improvements<br />

in energy efficiency necessary from UK industry<br />

– without undermining its competitiveness – will<br />

require significant interventions at both <strong>the</strong> UK and<br />

European levels.<br />

7. Primary reduction measures. Comparing <strong>the</strong><br />

main CO 2 reduction options shown in figure 2<br />

indicates that <strong>the</strong> following measures are essential:<br />

• rapid and large-scale switch of cars and light<br />

goods vehicles to electric battery power<br />

• radical improvement in industrial energy efficiency<br />

• large-scale application of renewable heat using<br />

solar energy and making maximum use of<br />

available biomass<br />

• intensive and substantial improvement in <strong>the</strong><br />

insulation of new and existing homes and<br />

buildings<br />

• development and application of carbon capture<br />

and storage (CCS) for large emitters in <strong>the</strong><br />

industry sector, in addition to its application for<br />

coal-burning power plant<br />

8. Secondary reduction measures. Wind power,<br />

nuclear power and solar photovoltaic (PV) are<br />

collectively essential to <strong>the</strong> decarbonisation of<br />

electricity production, reducing CO 2 emissions by<br />

over 100 MtCO 2 /yr from current levels. However,<br />

as electricity will be largely decarbonised by 2050,<br />

<strong>the</strong> value of any individual low-carbon power<br />

generating measure will be low, as shown in<br />

figure 2. The choice between <strong>the</strong>se alternatives<br />

must <strong>the</strong>refore be made on operational, economic<br />

and energy security grounds.<br />

9. Avoiding technology dependence. Choices<br />

between alternative measures can result in<br />

excessive dependence on key technologies. For<br />

example, <strong>the</strong> omission of a nuclear programme<br />

would result in heavy dependence on CCS<br />

technology, which is currently unproven at <strong>the</strong><br />

scale required for a major power plant.<br />

10. Avoiding fuel dependence. Fuel diversity issues<br />

can be managed if a holistic view of UK energy use<br />

is taken. The reference scenario (<strong>the</strong> base case<br />

for evaluation of alternative options) achieves a<br />

good diversity of fuels by substituting electricity for<br />

oil in <strong>the</strong> transport sector and by having a flexible<br />

electricity generation mix.<br />

11. Quick wins. Because of <strong>the</strong> scale of <strong>the</strong><br />

measures, improved building insulation, improved<br />

industry energy efficiency and greater use of<br />

electric vehicles all offer valuable reductions in<br />

carbon emissions by 2020. Early action is needed<br />

to deliver <strong>the</strong>se reductions.<br />

Figure 1 UK forward capacity gap<br />

Figure 2 Value of measures to 2050 CO 2 emission reductions<br />

05:06