Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

January 2012<br />

KMEFIC Research<br />

Equity Analysis Report<br />

<strong>Saudi</strong> <strong>Cement</strong> Industry<br />

<strong>Saudi</strong> Arabia is the largest cement producer in the GCC with a production capacity exceeding 42<br />

mtpa at the end of 2010. The <strong>Saudi</strong> cement industry enjoys an abundance of limestone reserves at<br />

low prices in addition to natural gas subsidies provided by Aramco. This allows <strong>Saudi</strong> cement<br />

companies to enjoy higher gross margins than their GCC competitors. <strong>Saudi</strong> cement companies<br />

have raised a request to increase the natural gas subsidies in order to meet growing domestic<br />

cement demand caused by new expansions.<br />

On June 6 th , 2008, the Ministry of Commerce & Industry took a decision to ban cement exports in<br />

order to fix and lower the domestic price of cement. The ban also called for cement companies to<br />

maintain 10% of their total cement production in reserves. However, a lot of the companies did not<br />

respond to this request despite strong governmental support in the form of low interest rate loans<br />

(from the <strong>Saudi</strong> Industrial Development Fund - SIDF) as well as obtaining quarries at low prices. As<br />

a result of the export ban, <strong>Saudi</strong> cement companies suffered from escalating clinker inventories<br />

during 2008 and 2009. Clinker inventory reached 10.9 million tons at the end of 2009, and 7.4<br />

million tons in 2008 against 1.7 million at the end of 2007.<br />

In an attempt to curb piling clinker inventories, a lot of the cement companies have shut down<br />

some of their production lines. As a result of this step, and in an atmosphere of growing domestic<br />

demand due to huge infrastructural projects, clinker inventories of <strong>Saudi</strong> cement companies fell<br />

0.8 million tons to reach 10.0 million tons at the end of 2010.<br />

<strong>Saudi</strong> <strong>Cement</strong> Industry Performance<br />

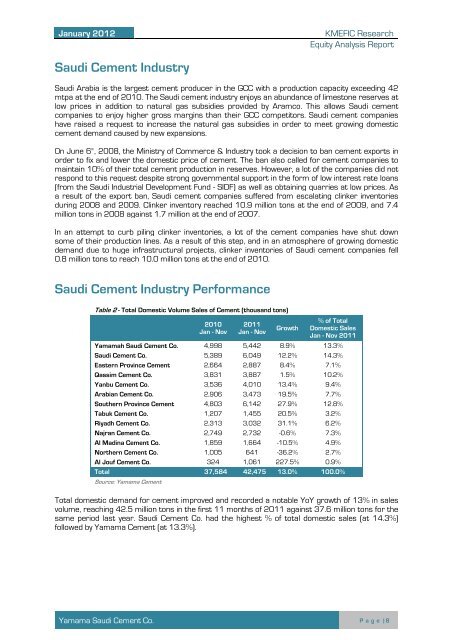

Table 2 - Total Domestic Volume Sales of <strong>Cement</strong> (thousand tons)<br />

2010<br />

Jan - Nov<br />

2011<br />

Jan - Nov<br />

Growth<br />

% of Total<br />

Domestic Sales<br />

Jan - Nov 2011<br />

Yamamah <strong>Saudi</strong> <strong>Cement</strong> Co. 4,998 5,442 8.9% 13.3%<br />

<strong>Saudi</strong> <strong>Cement</strong> Co. 5,389 6,049 12.2% 14.3%<br />

Eastern Province <strong>Cement</strong> 2,664 2,887 8.4% 7.1%<br />

Qassim <strong>Cement</strong> Co. 3,831 3,887 1.5% 10.2%<br />

Yanbu <strong>Cement</strong> Co. 3,536 4,010 13.4% 9.4%<br />

Arabian <strong>Cement</strong> Co. 2,906 3,473 19.5% 7.7%<br />

Southern Province <strong>Cement</strong> 4,803 6,142 27.9% 12.8%<br />

Tabuk <strong>Cement</strong> Co. 1,207 1,455 20.5% 3.2%<br />

Riyadh <strong>Cement</strong> Co. 2,313 3,032 31.1% 6.2%<br />

Najran <strong>Cement</strong> Co. 2,749 2,732 -0.6% 7.3%<br />

Al Madina <strong>Cement</strong> Co. 1,859 1,664 -10.5% 4.9%<br />

Northern <strong>Cement</strong> Co. 1,005 641 -36.2% 2.7%<br />

Al Jouf <strong>Cement</strong> Co. 324 1,061 227.5% 0.9%<br />

Total 37,584 42,475 13.0% 100.0%<br />

Source: Yamama <strong>Cement</strong><br />

Total domestic demand for cement improved and recorded a notable YoY growth of 13% in sales<br />

volume, reaching 42.5 million tons in the first 11 months of 2011 against 37.6 million tons for the<br />

same period last year. <strong>Saudi</strong> <strong>Cement</strong> Co. had the highest % of total domestic sales (at 14.3%)<br />

followed by Yamama <strong>Cement</strong> (at 13.3%).<br />

Yamama <strong>Saudi</strong> <strong>Cement</strong> Co. P a g e | 8