INDIAN RAYON AND INDUSTRIES LIMITED - Aditya Birla Nuvo, Ltd

INDIAN RAYON AND INDUSTRIES LIMITED - Aditya Birla Nuvo, Ltd

INDIAN RAYON AND INDUSTRIES LIMITED - Aditya Birla Nuvo, Ltd

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

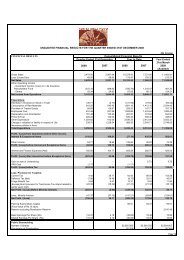

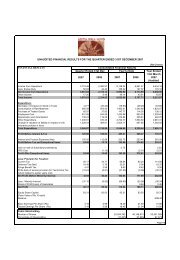

VISCOSE FILAMENT YARN<br />

1999-00 1998-99 % Change<br />

Installed Capacity (TPA) 15,000 15,000 —<br />

Production (Tonnes) 12,621 14,685 (-)14.1<br />

Sales Volume (Tonnes) 13,507 13,662 (-)1.1<br />

Gross Turnover (Rs. Crores) 244.6 279.8 (-)12.6<br />

Gross Realisation (Rs./Kg) 181.1 204.8 (-)11.6<br />

Operating Margin (%) 14.8 24.8<br />

Review of Operations<br />

Depressed domestic demand, sluggish exports and cheaper imports of substitute materials as well as end products impacted the Viscose Filament<br />

Yarn (VFY) business severely. Labour unrest and water scarcity at Veraval (Gujarat) compounded the problem further. As a result, despite<br />

outperforming domestic peers, the Division reported lower asset utilisation, drop in sales volumes and lower realisation. This affected overall margins<br />

and profitability of the Division adversely during the year.<br />

Depressed domestic demand<br />

The VFY sector in India witnessed one of worst years in its recent history. Industry demand dropped by 9% year-on-year (YoY) from 55,500<br />

tonnes in 1998-99 to 50,600 tonnes in 1999-2000. This was primarily due to a slump in demand from the user segments, notably the garments, dress<br />

materials and fashion fabrics. Such a poor trend was the result of a continued shift in consumption from VFY to Polyester Filament Yarn (PFY), prices<br />

of which remained substantially lower than the VFY prices despite firm global petrochemical prices. Further, relatively lower demand for fabrics also<br />

had adverse impact on the demand and prices of PFY in the local markets.<br />

Despite such an adverse market condition, the Company was able to maintain sales volumes at 13,507 tonnes during the year. Domestic sales<br />

improved from 11,440 tonnes in 1998-99 to 12,222 tonnes during the year, an increase of 7% YoY. Such a performance is a reflection of the<br />

Company’s continued focus on improved quality, strong brand image and aggressive marketing efforts. The Company’s market share has risen from<br />

24% in 1998-99 to 27% in 1999-2000.<br />

Sluggish exports<br />

The Company reported a sharp fall in export volumes, down 42%YoY to 1,285 tonnes in 1999-2000. We attribute this to sluggish global<br />

demand, change in fashion trends and increasing competition from cheaper substitutes.<br />

Lower asset utilisation<br />

Keeping in mind the poor demand situation and build-up of inventory towards end of last year, the Company decided to effect a 10-15% cut<br />

in production for most part of the year. This was lifted only during the last quarter of 1999-2000. The Company also faced an illegal strike at the<br />

VFY plant in Veraval, Gujarat for a brief period during March 2000. As a result of these, aggregate production fell 14% from 14,685 tonnes in 1998-<br />

99 to 12,621 tonnes in 1999-2000 and plant utilisation dropped from 98% to 84% during the year. Overall inventories are lower at 23 days and<br />

compare well with 39 days reported for 1998-99 and a peak inventory of 53 days in May 1999.<br />

Lower average realisation impacted margins adversely<br />

The Company reported a 12% YoY fall in gross realisation from Rs.204.8 per kg in 1998-99 to Rs.181.1 per kg in 1999-2000. Industry average<br />

price fell even sharper (by 15% YoY) and was due largely to the unfavourable demand situation and aggressive selling strategy followed by a few<br />

large players in the industry.<br />

This sharp fall in prices, together with lower volumes, negatively impacted margins during the year. Divisional margins fell from 25% in 1998-<br />

99 to 15%. A sharp rise in input costs also took its toll on margins. The average cost of wood pulp (the key raw material) moved up 18% YoY to<br />

US$630 per tonne, which together with rise in water costs added towards a major part of rise in input costs. The Company suffered on account of a<br />

8