Part 1 - Shire of Ashburton

Part 1 - Shire of Ashburton

Part 1 - Shire of Ashburton

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

<strong>Shire</strong> <strong>of</strong> <strong>Ashburton</strong> Tourism Strategy<br />

January 2011<br />

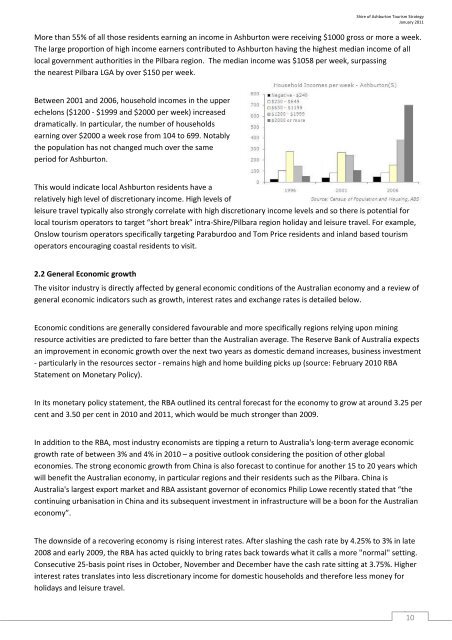

More than 55% <strong>of</strong> all those residents earning an income in <strong>Ashburton</strong> were receiving $1000 gross or more a week.<br />

The large proportion <strong>of</strong> high income earners contributed to <strong>Ashburton</strong> having the highest median income <strong>of</strong> all<br />

local government authorities in the Pilbara region. The median income was $1058 per week, surpassing<br />

the nearest Pilbara LGA by over $150 per week.<br />

Between 2001 and 2006, household incomes in the upper<br />

echelons ($1200 ‐ $1999 and $2000 per week) increased<br />

dramatically. In particular, the number <strong>of</strong> households<br />

earning over $2000 a week rose from 104 to 699. Notably<br />

the population has not changed much over the same<br />

period for <strong>Ashburton</strong>.<br />

This would indicate local <strong>Ashburton</strong> residents have a<br />

relatively high level <strong>of</strong> discretionary income. High levels <strong>of</strong><br />

leisure travel typically also strongly correlate with high discretionary income levels and so there is potential for<br />

local tourism operators to target “short break” intra‐<strong>Shire</strong>/Pilbara region holiday and leisure travel. For example,<br />

Onslow tourism operators specifically targeting Paraburdoo and Tom Price residents and inland based tourism<br />

operators encouraging coastal residents to visit.<br />

2.2 General Economic growth<br />

The visitor industry is directly affected by general economic conditions <strong>of</strong> the Australian economy and a review <strong>of</strong><br />

general economic indicators such as growth, interest rates and exchange rates is detailed below.<br />

Economic conditions are generally considered favourable and more specifically regions relying upon mining<br />

resource activities are predicted to fare better than the Australian average. The Reserve Bank <strong>of</strong> Australia expects<br />

an improvement in economic growth over the next two years as domestic demand increases, business investment<br />

‐ particularly in the resources sector ‐ remains high and home building picks up (source: February 2010 RBA<br />

Statement on Monetary Policy).<br />

In its monetary policy statement, the RBA outlined its central forecast for the economy to grow at around 3.25 per<br />

cent and 3.50 per cent in 2010 and 2011, which would be much stronger than 2009.<br />

In addition to the RBA, most industry economists are tipping a return to Australia's long‐term average economic<br />

growth rate <strong>of</strong> between 3% and 4% in 2010 – a positive outlook considering the position <strong>of</strong> other global<br />

economies. The strong economic growth from China is also forecast to continue for another 15 to 20 years which<br />

will benefit the Australian economy, in particular regions and their residents such as the Pilbara. China is<br />

Australia's largest export market and RBA assistant governor <strong>of</strong> economics Philip Lowe recently stated that “the<br />

continuing urbanisation in China and its subsequent investment in infrastructure will be a boon for the Australian<br />

economy”.<br />

The downside <strong>of</strong> a recovering economy is rising interest rates. After slashing the cash rate by 4.25% to 3% in late<br />

2008 and early 2009, the RBA has acted quickly to bring rates back towards what it calls a more "normal" setting.<br />

Consecutive 25‐basis point rises in October, November and December have the cash rate sitting at 3.75%. Higher<br />

interest rates translates into less discretionary income for domestic households and therefore less money for<br />

holidays and leisure travel.<br />

10