- Page 1 and 2:

A N N U A L R E P O R T 2 0 1 0

- Page 4 and 5:

PAGE PAGE PAGE financial summary 14

- Page 6 and 7:

Grupo Security Summarized Unconsoli

- Page 9:

02 principal financial indicators n

- Page 12 and 13:

DEAR SHAREHOLDERS I have the pleasu

- Page 15 and 16:

oard and management 04

- Page 17 and 18:

04board and management SENIOR MANAG

- Page 19 and 20:

05 recognitions 17 COMPANIES WITH B

- Page 21 and 22:

06 activities 19 ENCUENTRO JUVENTUD

- Page 23 and 24:

06 activities 21 A SCHOOL FOR VILLA

- Page 25:

2003 Inversiones Seguros Security i

- Page 28 and 29:

ECONOMIC CONTEXT EXTERNAL ENVIRONME

- Page 30 and 31:

CHILE: GDP GROWTH (%) 7 6 5 4 3 2 1

- Page 33 and 34:

09strategic pillars

- Page 35 and 36:

09strategic pillars security, where

- Page 37 and 38:

09 strategic pillars RISK MANAGEMEN

- Page 39 and 40:

10business areas

- Page 41:

10 business areas 39 PAGE

- Page 44 and 45:

FINANCING BANKING INDUSTRY Banking

- Page 46 and 47:

The following graph shows the evolu

- Page 48 and 49:

EARNINGS AND ROE OF BANCO SECURITY

- Page 50 and 51:

RISK Banco Security has been charac

- Page 53 and 54:

10business areas I N V E S T M E N

- Page 55 and 56:

10 business areas 53 Administradora

- Page 57:

10 business areas 55 SECURITIZADORA

- Page 60 and 61:

INSURANCE INSURANCE INDUSTRY The Ch

- Page 62 and 63:

Compañía de Seguros Generales Pen

- Page 65 and 66:

10business areas S E R V I C E S

- Page 67:

It is important to recall that the

- Page 70 and 71:

INVESTMENT POLICY The bylaws of Gru

- Page 72 and 73:

The individual financial liabilitie

- Page 74 and 75:

BANK CREDITORS As of December 31, 2

- Page 76 and 77:

ASSOCIATED RISKS Local Financial Ri

- Page 79 and 80:

company information 12

- Page 81 and 82:

12company information In accordance

- Page 83 and 84:

12 company information 81 • Revis

- Page 85 and 86: 12 company information 83 In Seguro

- Page 87 and 88: 12 company information 85 STOCK MAR

- Page 89 and 90: 12 company information 87 SOCIEDAD

- Page 91 and 92: 12 company information 89 INMOBILIA

- Page 93 and 94: Regulatory Framework Grupo Security

- Page 95 and 96: financial statements 13

- Page 97: financial statements 13 C o n s o l

- Page 100 and 101: Consolidated Statement of Financial

- Page 102 and 103: Consolidated statement of comprehen

- Page 104 and 105: CONSOLIDATED STATEMENTS OF CASH FLO

- Page 106 and 107: CONSOLIDATED STATEMENT OF CHANGES I

- Page 108 and 109: The following companies are include

- Page 110 and 111: ) Description of Grupo Security’s

- Page 112 and 113: - Fair value option As indicated in

- Page 114 and 115: Disclosure of the Adoption of new a

- Page 116 and 117: For financial assets, the amortized

- Page 118 and 119: The recoverable amount is the highe

- Page 120 and 121: Vida Security maintains current der

- Page 122 and 123: f) Structured fixed income notes Vi

- Page 124 and 125: CategorY Estimated range of loss Lo

- Page 126 and 127: The main components of the cost of

- Page 128 and 129: 2.30 Foreign currency and indexatio

- Page 130 and 131: The most significant areas of estim

- Page 132 and 133: i. Pension insurances reserves This

- Page 134 and 135: 3.1 Main changes in the accounting

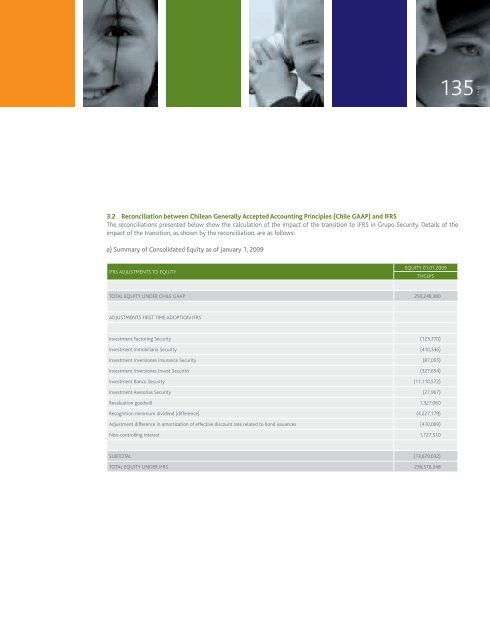

- Page 138 and 139: ) Summary of Consolidated Equity as

- Page 140 and 141: 3.3 Main adjustments made a) Invest

- Page 142 and 143: NotE 5 - Income taxes Deferred tax

- Page 144 and 145: Inmobiliaria Security S.A. measures

- Page 146 and 147: NotE 8 - Investments in Associates

- Page 148 and 149: NotE 9 - Property, Plant and Equipm

- Page 150 and 151: ) The amortization of intangible as

- Page 152 and 153: NotE 13 - Other Financial Assets, C

- Page 154 and 155: NotE 16 - Other Non-Financial Asset

- Page 156 and 157: Detail of bank obligations as of De

- Page 158 and 159: Detail of bank obligations as of Ja

- Page 160 and 161: Detail of the bonds at December 31,

- Page 162 and 163: NotE 19 - Other Non-Financial Liabi

- Page 164 and 165: NotE 23 - Other Financial Liabiliti

- Page 166 and 167: Note 24 - Non-Current Liabilities A

- Page 168 and 169: ) Cost of Sales The items includes

- Page 170 and 171: NotE 26 - Administrative expenses T

- Page 172 and 173: BALANCE 31.12.2010 31.12.2009 01.01

- Page 174 and 175: Up to 1 year From 1 to 3 years From

- Page 176 and 177: The management of Grupo Security S.

- Page 178 and 179: c) Statement of Financial Position

- Page 180 and 181: e) Statement of Financial Position

- Page 182 and 183: 2) Risk Management Structure Banco

- Page 184 and 185: 4º Credit Management Basically, th

- Page 186 and 187:

In the case of the Bank’s impaire

- Page 188 and 189:

These are the details of guarantees

- Page 190 and 191:

Loans that are classified individua

- Page 192 and 193:

Such limitations allow the Bank to

- Page 194 and 195:

Banco Security and its Subsidiaries

- Page 196 and 197:

Market risk trading ledger 31.12.20

- Page 198 and 199:

Regulatory Liquidity Mismatching as

- Page 200 and 201:

Regulatory Liquidity Mismatching as

- Page 202 and 203:

currency swaps). These derivatives

- Page 204 and 205:

Participants in the Credit Risk Com

- Page 206 and 207:

7) Regulatory Capital Requirement I

- Page 208 and 209:

6) Summary of the Policy for Invest

- Page 210 and 211:

d) Dividends The policy agreed by t

- Page 212 and 213:

The following table shows financial

- Page 214 and 215:

Valores Security S.A. Corredores de

- Page 216 and 217:

• The Board of Directors agreed t

- Page 218 and 219:

Note 37 - Subsequent Events On Janu

- Page 220 and 221:

MANAGEMENT’S ANALYSIS OF CONSOLID

- Page 222 and 223:

2.2 Factoring Industry Factoring ha

- Page 224 and 225:

5. Risk Factors 5.1 Dependence on d

- Page 226 and 227:

6 PERFORMANCE INDECATORS OF THE CON

- Page 228 and 229:

$ Pesos Chilenos MM$ Millones de Pe

- Page 230 and 231:

BANCO SECURITY AND SUBSIDIARIES Typ

- Page 232 and 233:

Banco Security and Subsidiaries Con

- Page 234 and 235:

Banco Security and Subsidiaries Con

- Page 236 and 237:

Valores Security S.A. Corredores de

- Page 238 and 239:

Administradora General de Fondos Se

- Page 240 and 241:

Factoring Security S.A. Type of ent

- Page 242 and 243:

Asesorias Security S.A. AND SUBSIDI

- Page 244 and 245:

Securitizadora Security S.A. Type o

- Page 246 and 247:

Global Asset Advisors Type of entit

- Page 248 and 249:

Inversiones Seguros Security Ltda A

- Page 250 and 251:

Seguros Vida Security Previsión S.

- Page 252 and 253:

Compañía de Seguros Generales Pen

- Page 254 and 255:

Servicios Security S.A. AND SUBSIDI

- Page 256 and 257:

Corredores de Seguros Security Ltda

- Page 258 and 259:

Europ Assistance Chile s.A. Type of

- Page 260 and 261:

Cooper Gay Chile S.A. Corredores de

- Page 262 and 263:

Inmobiliaria Security S.A. AND SUBS

- Page 264 and 265:

INVERSIONES INVEST SECURITY LTDA. A

- Page 266 and 267:

Travel Security S.A. AND SUBSIDIARI

- Page 268 and 269:

Global Security Gestión y Servicio

- Page 270 and 271:

Mandatos Security Ltda. Type of ent

- Page 272 and 273:

GROUP OWNERSHIP STRUCTURE The follo

- Page 274 and 275:

D E C L A R A T I O N O F R E S P O

- Page 276 and 277:

ADDRESSES OF COMPANIES OF GRUPO SEC

- Page 278 and 279:

Santa Elena Branch Santa Elena 2400

- Page 280 and 281:

Santiago Nueva York 33, Office 1402

- Page 282:

“THIS PAPER COMES FROM FORESTS MA