Granger-causality tests

Granger-causality tests

Granger-causality tests

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

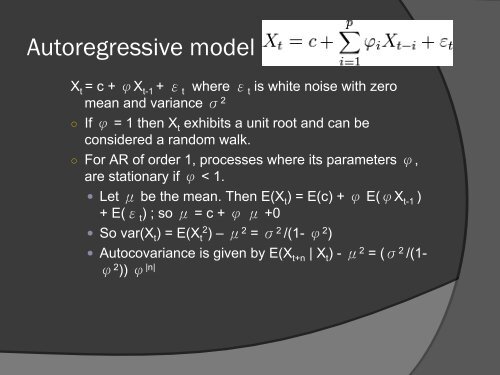

Autoregressive model<br />

X t = c + φX t-1 + ε t where ε t is white noise with zero<br />

mean and variance σ 2<br />

○ If φ = 1 then X t exhibits a unit root and can be<br />

considered a random walk.<br />

○ For AR of order 1, processes where its parameters φ,<br />

are stationary if φ < 1.<br />

• Let μ be the mean. Then E(X t ) = E(c) + φ E(φX t-1 )<br />

+ E(ε t ) ; so μ = c + φ μ+0<br />

• So var(X t ) = E(X t 2 ) – μ 2 = σ 2 /(1- φ 2 )<br />

• Autocovariance is given by E(X t+n | X t ) - μ 2 =(σ 2 /(1-<br />

φ 2 )) φ |n|