Granger-causality tests

Granger-causality tests

Granger-causality tests

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

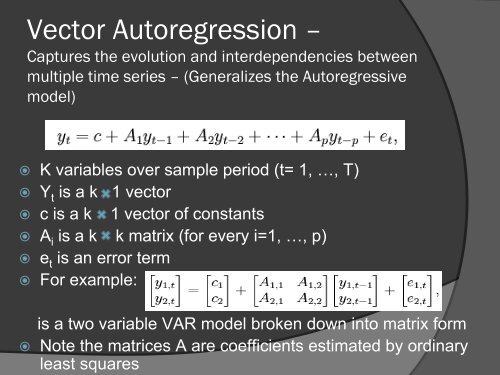

is a two variable VAR model broken down into matrix form<br />

Note the matrices A are coefficients estimated by ordinary<br />

least squares<br />

Vector Autoregression –<br />

Captures the evolution and interdependencies between<br />

multiple time series – (Generalizes the Autoregressive<br />

model)<br />

K variables over sample period (t= 1, …, T)<br />

Y t is a k 1 vector<br />

c is a k 1 vector of constants<br />

A i is a k k matrix (for every i=1, …, p)<br />

e t is an error term<br />

For example: