Funds GreatLink - Great Eastern Life

Funds GreatLink - Great Eastern Life

Funds GreatLink - Great Eastern Life

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

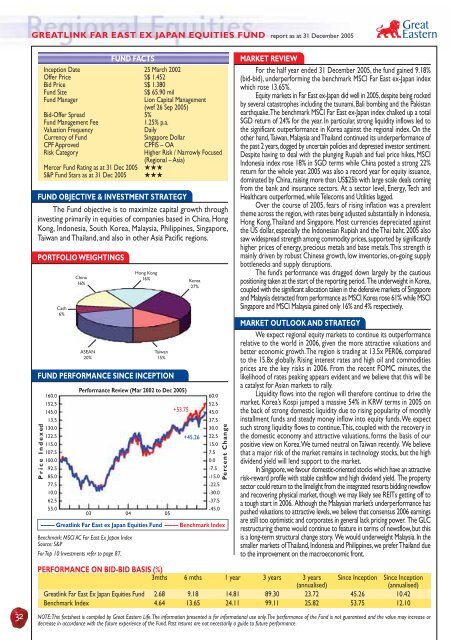

GREATLINK FAR EAST EX JAPAN EQUITIES FUND report as at 31 December 2005<br />

FUND FACTS<br />

Inception Date 25 March 2002<br />

Offer Price S$ 1.452<br />

Bid Price S$ 1.380<br />

Fund Size<br />

Fund Manager<br />

S$ 65.90 mil<br />

Lion Capital Management<br />

(wef 26 Sep 2005)<br />

Bid-Offer Spread 5%<br />

Fund Management Fee<br />

1.25% p.a.<br />

Valuation Frequency<br />

Daily<br />

Currency of Fund<br />

Singapore Dollar<br />

CPF Approved<br />

CPFIS – OA<br />

Risk Category<br />

Higher Risk / Narrowly Focused<br />

(Regional – Asia)<br />

Mercer Fund Rating as at 31 Dec 2005 ★★★<br />

S&P Fund Stars as at 31 Dec 2005 ★★★<br />

FUND OBJECTIVE & INVESTMENT STRATEGY<br />

The Fund objective is to maximize capital growth through<br />

investing primarily in equities of companies based in China, Hong<br />

Kong, Indonesia, South Korea, Malaysia, Philippines, Singapore,<br />

Taiwan and Thailand, and also in other Asia Pacific regions.<br />

PORTFOLIO WEIGHTINGS<br />

FUND PERFORMANCE SINCE INCEPTION<br />

Price Indexed<br />

160.0<br />

152.5<br />

145.0<br />

13.5<br />

130.0<br />

122.5<br />

115.0<br />

107.5<br />

100.0<br />

92.5<br />

85.0<br />

77.5<br />

10.0<br />

62.5<br />

55.0<br />

Cash<br />

6%<br />

China<br />

16%<br />

ASEAN<br />

20%<br />

Hong Kong<br />

16%<br />

Taiwan<br />

15%<br />

Performance Review (Mar 2002 to Dec 2005)<br />

03 04 05<br />

+53.75<br />

Korea<br />

27%<br />

+45.26<br />

60.0<br />

52.5<br />

45.0<br />

37.5<br />

30.0<br />

22.5<br />

15.0<br />

7.5<br />

0.0<br />

-7.5<br />

-15.0<br />

-22.5<br />

-30.0<br />

-37.5<br />

-45.0<br />

––––– <strong>Great</strong>link Far East ex Japan Equities Fund ––––– Benchmark Index<br />

Benchmark: MSCI AC Far East Ex Japan Index<br />

Source: S&P<br />

For Top 10 Investments refer to page 87.<br />

Percent Change<br />

MARKET REVIEW<br />

For the half year ended 31 December 2005, the fund gained 9.18%<br />

(bid-bid), underperforming the benchmark MSCI Far East ex-Japan index<br />

which rose 13.65%.<br />

Equity markets in Far East ex-Japan did well in 2005, despite being rocked<br />

by several catastrophes including the tsunami, Bali bombing and the Pakistan<br />

earthquake. The benchmark MSCI Far East ex-Japan index chalked up a total<br />

SGD return of 24% for the year. In particular, strong liquidity inflows led to<br />

the significant outperformance in Korea against the regional index. On the<br />

other hand, Taiwan, Malaysia and Thailand continued its underperformance of<br />

the past 2 years, dogged by uncertain policies and depressed investor sentiment.<br />

Despite having to deal with the plunging Rupiah and fuel price hikes, MSCI<br />

Indonesia index rose 18% in SGD terms while China posted a strong 22%<br />

return for the whole year. 2005 was also a record year for equity issuance,<br />

dominated by China, raising more than US$25b with large scale deals coming<br />

from the bank and insurance sectors. At a sector level, Energy, Tech and<br />

Healthcare outperformed, while Telecoms and Utilities lagged.<br />

Over the course of 2005, fears of rising inflation was a prevalent<br />

theme across the region, with rates being adjusted substantially in Indonesia,<br />

Hong Kong, Thailand and Singapore. Most currencies depreciated against<br />

the US dollar, especially the Indonesian Rupiah and the Thai baht. 2005 also<br />

saw widespread strength among commodity prices, supported by significantly<br />

higher prices of energy, precious metals and base metals. This strength is<br />

mainly driven by robust Chinese growth, low inventories, on-going supply<br />

bottlenecks and supply disruptions.<br />

The fund’s performance was dragged down largely by the cautious<br />

positioning taken at the start of the reporting period. The underweight in Korea,<br />

coupled with the significant allocation taken in the defensive markets of Singapore<br />

and Malaysia detracted from performance as MSCI Korea rose 61% while MSCI<br />

Singapore and MSCI Malaysia gained only 16% and 4% respectively.<br />

MARKET OUTLOOK AND STRATEGY<br />

We expect regional equity markets to continue its outperformance<br />

relative to the world in 2006, given the more attractive valuations and<br />

better economic growth. The region is trading at 13.5x PER06, compared<br />

to the 15.8x globally. Rising interest rates and high oil and commodities<br />

prices are the key risks in 2006. From the recent FOMC minutes, the<br />

likelihood of rates peaking appears evident and we believe that this will be<br />

a catalyst for Asian markets to rally.<br />

Liquidity flows into the region will therefore continue to drive the<br />

market. Korea’s Kospi jumped a massive 54% in KRW terms in 2005 on<br />

the back of strong domestic liquidity due to rising popularity of monthly<br />

installment funds and steady money inflow into equity funds. We expect<br />

such strong liquidity flows to continue. This, coupled with the recovery in<br />

the domestic economy and attractive valuations, forms the basis of our<br />

positive view on Korea. We turned neutral on Taiwan recently. We believe<br />

that a major risk of the market remains in technology stocks, but the high<br />

dividend yield will lend support to the market.<br />

In Singapore, we favour domestic-oriented stocks which have an attractive<br />

risk-reward profile with stable cashflow and high dividend yield. The property<br />

sector could return to the limelight from the integrated resorts bidding newsflow<br />

and recovering physical market, though we may likely see REITs getting off to<br />

a tough start in 2006. Although the Malaysian market’s underperformance has<br />

pushed valuations to attractive levels, we believe that consensus 2006 earnings<br />

are still too optimistic and corporates in general lack pricing power. The GLC<br />

restructuring theme would continue to feature in terms of newsflow, but this<br />

is a long-term structural change story. We would underweight Malaysia. In the<br />

smaller markets of Thailand, Indonesia and Philippines, we prefer Thailand due<br />

to the improvement on the macroeconomic front.<br />

PERFORMANCE ON BID-BID BASIS (%)<br />

3mths 6 mths 1 year 3 years 3 years Since Inception Since Inception<br />

(annualised)<br />

(annualised)<br />

<strong>Great</strong>link Far East Ex Japan Equities Fund 2.68 9.18 14.81 89.30 23.72 45.26 10.42<br />

Benchmark Index 4.64 13.65 24.11 99.11 25.82 53.75 12.10<br />

32 NOTE: This factsheet is compiled by <strong>Great</strong> <strong>Eastern</strong> <strong>Life</strong>. The information presented is for informational use only. The performance of the Fund is not guaranteed and the value may increase or<br />

decrease in accordance with the future experience of the Fund. Past returns are not necessarily a guide to future performance.