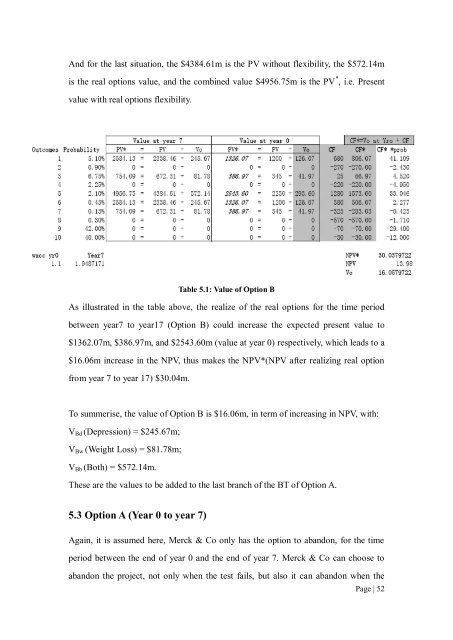

And for the last situation, the $4384.61m is the PV without flexibility, the $572.14mis the <strong>real</strong> <strong>options</strong> value, and the comb<strong>in</strong>ed value $4956.75m is the PV * , i.e. Presentvalue with <strong>real</strong> <strong>options</strong> flexibility.Table 5.1: Value <strong>of</strong> Option BAs illustrated <strong>in</strong> the table above, the <strong>real</strong>ize <strong>of</strong> the <strong>real</strong> <strong>options</strong> for the time periodbetween year7 <strong>to</strong> year17 (Option B) could <strong>in</strong>crease the expected present value <strong>to</strong>$1362.07m, $386.97m, and $2543.60m (value at year 0) respectively, which leads <strong>to</strong> a$16.06m <strong>in</strong>crease <strong>in</strong> the NPV, thus makes the NPV*(NPV after <strong>real</strong>iz<strong>in</strong>g <strong>real</strong> optionfrom year 7 <strong>to</strong> year 17) $30.04m.To summerise, the value <strong>of</strong> Option B is $16.06m, <strong>in</strong> term <strong>of</strong> <strong>in</strong>creas<strong>in</strong>g <strong>in</strong> NPV, with:V Bd (Depression) = $245.67m;V Bw (Weight Loss) = $81.78m;V Bb (Both) = $572.14m.These are the values <strong>to</strong> be added <strong>to</strong> the last branch <strong>of</strong> the BT <strong>of</strong> Option A.5.3 Option A (Year 0 <strong>to</strong> year 7)Aga<strong>in</strong>, it is assumed here, Merck & Co only has the option <strong>to</strong> abandon, for the timeperiod between the end <strong>of</strong> year 0 and the end <strong>of</strong> year 7. Merck & Co can choose <strong>to</strong>abandon the project, not only when the test fails, but also it can abandon when thePage | 52

project turns out <strong>to</strong> be unpr<strong>of</strong>itable.The first option is at the end <strong>of</strong> year 2, when Merck & Co. can choose whether or not<strong>to</strong> abandon. The second is at the end <strong>of</strong> year 4, and the third is at the end <strong>of</strong> year 7. Asall the <strong>options</strong> can only be exercised at a specific time (i.e. when the Phase ends), itcan be seen as a European option. Moreover, s<strong>in</strong>ce the third option only exist if thesecond option is open, and the second only exist when the first option is open, theycan be seen as a sequential compound option.Furthermore, as there are two k<strong>in</strong>d <strong>of</strong> uncerta<strong>in</strong>ty regard<strong>in</strong>g <strong>to</strong> this option, it can beseen as a compound ra<strong>in</strong>bow option. The <strong>valuation</strong> <strong>of</strong> a compound ra<strong>in</strong>bow option canbe calculated from a b<strong>in</strong>omial tree approach. However, as result <strong>of</strong> the complexity <strong>of</strong>this compound option, the <strong>valuation</strong> <strong>of</strong> this compound ra<strong>in</strong>bow option can be ratherdifficult. As will see later, there are three underly<strong>in</strong>g assets, which have five differentprobabilities <strong>of</strong> success for Phase III, and recomb<strong>in</strong>ed as three probabilities at Phase II,it would be very complicated <strong>to</strong> construct a s<strong>in</strong>gle b<strong>in</strong>omial tree <strong>in</strong> order <strong>to</strong> value thiscompound ra<strong>in</strong>bow option. Therefore, firstly, a simpler <strong>valuation</strong> approach is used, byvalu<strong>in</strong>g three separate compound <strong>options</strong> <strong>in</strong>dividually, and then comb<strong>in</strong><strong>in</strong>g the valueus<strong>in</strong>g their correspond<strong>in</strong>g probabilities. After this <strong>valuation</strong>, the compound ra<strong>in</strong>bowoption is valued by us<strong>in</strong>g a s<strong>in</strong>gle b<strong>in</strong>omial tree <strong>to</strong> compare the different results.5.3.1 Five variables that determ<strong>in</strong>e the value <strong>of</strong> the <strong>options</strong>The value <strong>of</strong> the underly<strong>in</strong>g asset – there are three underly<strong>in</strong>g asset <strong>in</strong> this case,which are $1200m, $345m, and $2250m respectively.The time <strong>to</strong> expiration – <strong>in</strong> this case, as it is a compound option, T 1 is 2, T 2 is 2, andT 3 is 3.Volatility – as mentioned earlier, for the time period between year 0 and year 7, thevolatility would be more project-related. In this case, past performance <strong>of</strong> LABPharmaceuticals can also be used as a reference. Here, volatility could be calculatedus<strong>in</strong>g the basic formula for standard deviation, and then transferred <strong>to</strong> yearly volatilityPage | 53

- Page 1 and 2:

APPLICATION OF REAL OPTIONS VALUATI

- Page 3 and 4:

Table of ContentsAbstract .........

- Page 5 and 6:

List of TablesTable 5.1: Value of O

- Page 7 and 8: Chapter One— IntroductionAs one o

- Page 9 and 10: Then, in Chapter 4, the case study

- Page 11 and 12: and we will have the right to take

- Page 13 and 14: project, to get its salvage value,

- Page 15 and 16: The option to switch:If assets have

- Page 17 and 18: 2.2 Advantages of Real Option Valua

- Page 19 and 20: In the case of pharmaceutical R&D,

- Page 21 and 22: delayed in time. Undertaking one pr

- Page 23 and 24: Figure 2.2: Advantages and disadvan

- Page 25 and 26: smallest possible payoff of zero, w

- Page 27 and 28: options applications is the binomia

- Page 29 and 30: t: years to expirationr: annual ris

- Page 31 and 32: Chapter Three— Apply Real options

- Page 33 and 34: on Howell et al (2001).3.1.1 Precli

- Page 35 and 36: approved.3.2 real options valuation

- Page 37 and 38: Figure 3.3: Comparison of a call op

- Page 39 and 40: applying the principals of activity

- Page 41 and 42: that has occurred in the past. Depe

- Page 43 and 44: Chapter Four— Case StudyFor this

- Page 45 and 46: 4.3 DavanrikLAB Pharmaceuticals ori

- Page 47 and 48: efficacious for depression only, a

- Page 49 and 50: Chapter Five— Case Study Analysis

- Page 51 and 52: figure below:Figure 5.3: NPV of Dav

- Page 53 and 54: Merck & Co (10%), which gives $2338

- Page 55 and 56: approval and other issues. Therefor

- Page 57: of $345m at year 0 (which is $672.3

- Page 61 and 62: these three options, the risk-free

- Page 63 and 64: ewrite as, noting all the costs (in

- Page 65 and 66: Figure 5.10: Valuation of Option A

- Page 67 and 68: Figure 5.12: Valuation of Option A

- Page 69 and 70: Figure 5.13 Valuation of Compound r

- Page 71 and 72: $ in millionmillion to $113.97 mill

- Page 73 and 74: Chapter Six— Limitations and conc

- Page 75 and 76: discovery projects, arrives in a di

- Page 77 and 78: References1. Amram M & Kulatilaka N

- Page 79 and 80: 31/08/2006, available at: http://ho

- Page 81 and 82: 46. T rigeorgis L . (1995), ―M et