On the real effects of private equity investment: evidence from new ...

On the real effects of private equity investment: evidence from new ...

On the real effects of private equity investment: evidence from new ...

- No tags were found...

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

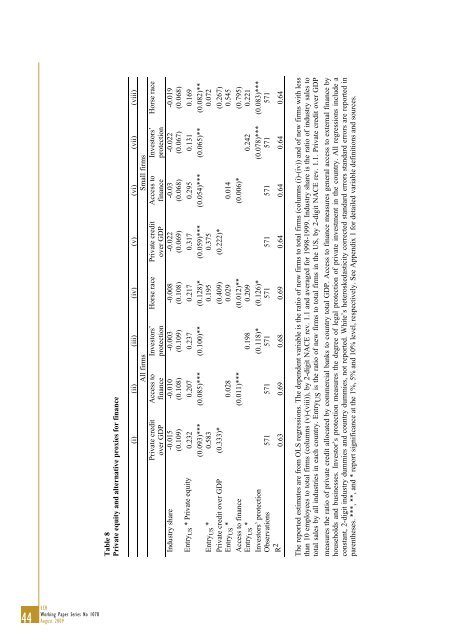

Table 8Private <strong>equity</strong> and alternative proxies for financeIndustry share(i) (ii) (iii) (iv) (v) (vi) (vii) (viii)All firms Small firmsPrivate creditover GDPAccess t<strong>of</strong>inanceInvestors’protectionHorse race Private creditover GDPAccess t<strong>of</strong>inanceInvestors’protectionHorse race-0.015 -0.010 -0.003 -0.008 -0.022 -0.03 -0.022 -0.019(0.109) (0.108) (0.109) (0.108) (0.069) (0.068) (0.067) (0.068)Entry US * Private <strong>equity</strong> 0.232 0.207 0.237 0.217 0.317 0.295 0.131 0.169(0.093)*** (0.085)*** (0.100)** (0.128)* (0.059)*** (0.054)*** (0.065)** (0.082)**Entry US *0.583 0.195 0.375 0.072Private credit over GDP (0.333)* (0.409) (0.222)* (0.267)Entry US *0.028 0.029 0.014 0.545Access to finance (0.011)*** (0.012)** (0.006)* (0.795)Entry US *0.198 0.209 0.242 0.221Investors’ protection (0.118)* (0.126)* (0.078)*** (0.083)***Observations 571 571 571 571 571 571 571 571R 2 0.63 0.69 0.68 0.69 0.64 0.64 0.64 0.64The reported estimates are <strong>from</strong> OLS regressions. The dependent variable is <strong>the</strong> ratio <strong>of</strong> <strong>new</strong> firms to total firms (columns (i)-(iv)) and <strong>of</strong> <strong>new</strong> firms with lessthan 10 employees to total firms (columns (v)-(viii)), by 2-digit NACE rev. 1.1 and averaged for 1998-1999. Industry share is <strong>the</strong> ratio <strong>of</strong> industry sales tototal sales by all industries in each country. Entry US is <strong>the</strong> ratio <strong>of</strong> <strong>new</strong> firms to total firms in <strong>the</strong> US, by 2-digit NACE rev. 1.1. Private credit over GDPmeasures <strong>the</strong> ratio <strong>of</strong> <strong>private</strong> credit allocated by commercial banks to country total GDP. Access to finance measures general access to external finance byhouseholds and businesses. Investor’s protection measures <strong>the</strong> degree <strong>of</strong> legal protection <strong>of</strong> <strong>private</strong> <strong>investment</strong> in <strong>the</strong> country. All regressions include aconstant, 2-digit industry dummies and country dummies, not reported. White’s heteroskedasticity corrected standard errors standard errors are reported inparen<strong>the</strong>ses. ***, **, and * report significance at <strong>the</strong> 1%, 5% and 10% level, respectively. See Appendix 1 for detailed variable definitions and sources.44 ECBWorking Paper Series No 1078August 2009