IRFC COVER-final - Indian Railway Finance Corporation Ltd.

IRFC COVER-final - Indian Railway Finance Corporation Ltd.

IRFC COVER-final - Indian Railway Finance Corporation Ltd.

- No tags were found...

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

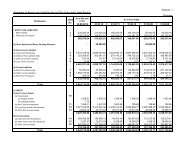

SCHEDULE-16SIGNIFICANT ACCOUNTING POLICIES AND NOTES ON ACCOUNTSA. Significant Accounting Policies1) Basis for preparation of Financial Statementsa) The financial statements are prepared under the historical cost convention, in accordance with the Generally Accepted AccountingPrinciples, Provisions of the Companies Act, 1956 and the applicable guidelines issued by the Reserve Bank of India as adoptedconsistently by the Company.b) Use of EstimatesThe preparation of financial statements in conformity with Generally Accepted Accounting Principles requires Management to makeestimates and assumptions that affect the reported amounts of asset and liabilities, disclosure of contingent assets and liabilities atthe date of the financial statements and the reported amounts of revenue and expenses during the reporting period. Examples of suchestimates include estimated useful life of fixed assets and estimated useful life of leased assets. The Management believes thatestimates used in the preparation of financial statements are prudent and reasonable. Actual results could differ from these estimates.Adjustments as a result of differences between actual and estimates are made prospectively.2) Revenue Recognitiona) Lease Income in respect of assets given on lease (including assets given prior to 01-04-2001) is recognised in accordance with theaccounting treatment provided in Accounting Standard -19.b) Lease Rentals on assets taken on lease and sub-leased to Ministry of <strong>Railway</strong>s (MOR) prior to 01.04.2001, are accounted for at therates of lease rentals provided in the agreements with the respective lessors and the sub-lessee (MOR), on accrual basis, as per theRevised Guidance Note on accounting for Leases issued by the Institute of Chartered Accountants of India (ICAI).c) Interest Income is recognised on time proportion basis. Dividend Income is recognised when the right to receive payment is established.d) Income relating to non performing assets is recognised on receipt basis in accordance with the guidelines issued by the Reserve Bankof India.3) Foreign Currency Transactionsa) Initial RecognitionInitial recognition is done at the rates prevailing on the date of transactioni) for acquisition of assets, andii)for interest payment on Loans, Commitment Charges and expenses.b) Recognition at the end of Accounting PeriodForeign Currency monetary assets and liabilities, other than the foreign currency liabilities swapped into <strong>Indian</strong> Rupees, are reportedusing the closing exchange rate in accordance with the provisions of AS 11 issued by the Institute of Chartered Accountants of India.Foreign Currency Liabilities swapped into <strong>Indian</strong> Rupees are stated at the reference rates fixed in the swap transactions, and nottranslated at the year end rate.c) Exchange Differencesi) Exchange differences arising on the actual settlement of monetary assets and liabilities at rates different from those at which theywere initially recorded during the year, or reported in previous financial statements, other than the exchange differences onsettlement of foreign currency loans and interest thereon recoverable separately from the lessee under the lease agreements,are recognised as income or expenses in the year in which they arise.ii)Notional Exchange Differences arising on reporting of outstanding long term foreign currency monetary assets and liabilities atrates different from those at which they were initially recorded during the year, or reported in previous financial statements, other48