acfe fraud prevention check-up - BKD

acfe fraud prevention check-up - BKD

acfe fraud prevention check-up - BKD

- No tags were found...

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

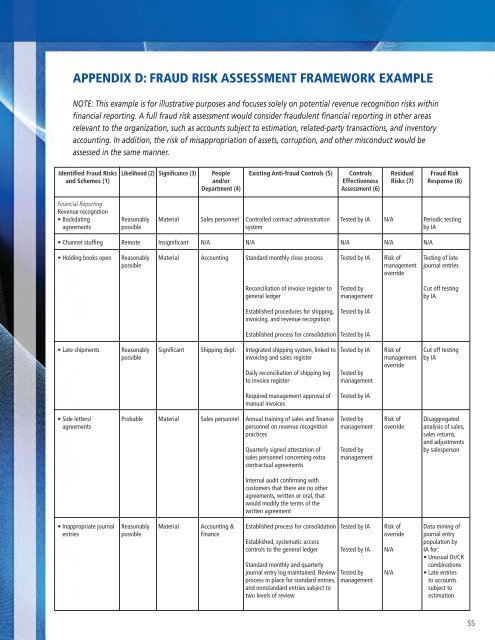

APPENDIX D: FRAUD RISK ASSESSMENT FRAMEWORK EXAMPLENOTE: This example is for illustrative purposes and focuses solely on potential revenue recognition risks withinfinancial reporting. A full <strong>fraud</strong> risk assessment would consider <strong>fraud</strong>ulent financial reporting in other areasrelevant to the organization, such as accounts subject to estimation, related-party transactions, and inventoryaccounting. In addition, the risk of misappropriation of assets, corr<strong>up</strong>tion, and other misconduct would beassessed in the same manner.Identified Fraud Risksand Schemes (1)Likelihood (2)Significance (3)Peopleand/orDepartment (4)Existing Anti-<strong>fraud</strong> Controls (5)ControlsEffectivenessAssessment (6)ResidualRisks (7)Fraud RiskResponse (8)Financial ReportingRevenue recognition• BackdatingagreementsReasonablypossibleMaterialSales personnelControlled contract administrationsystemTested by IAN/APeriodic testingby IA• Channel stuffingRemoteInsignificantN/AN/AN/AN/AN/A• Holding books openReasonablypossibleMaterialAccountingStandard monthly close processTested by IARisk ofmanagementoverrideTesting of latejournal entriesReconciliation of invoice register togeneral ledgerTested bymanagementCut off testingby IAEstablished procedures for shipping,invoicing, and revenue recognitionTested by IAEstablished process for consolidationTested by IA• Late shipmentsReasonablypossibleSignificantShipping dept.Integrated shipping system, linked toinvoicing and sales registerDaily reconciliation of shipping logto invoice registerTested by IATested bymanagementRisk ofmanagementoverrideCut off testingby IARequired management approval ofmanual invoicesTested by IA• Side letters/agreementsProbableMaterialSales personnelAnnual training of sales and financepersonnel on revenue recognitionpracticesQuarterly signed attestation ofsales personnel concerning extracontractual agreementsTested bymanagementTested bymanagementRisk ofoverrideDisaggregatedanalysis of sales,sales returns,and adjustmentsby salespersonInternal audit confirming withcustomers that there are no otheragreements, written or oral, thatwould modify the terms of thewritten agreement• Inappropriate journalentriesReasonablypossibleMaterialAccounting &FinanceEstablished process for consolidationEstablished, systematic accesscontrols to the general ledgerStandard monthly and quarterlyjournal entry log maintained. Reviewprocess in place for standard entries,and nonstandard entries subject totwo levels of reviewTested by IATested by IATested bymanagementRisk ofoverrideN/AN/AData mining ofjournal entrypopulation byIA for:• Unusual Dr/CRcombinations• Late entriesto accountssubject toestimation55