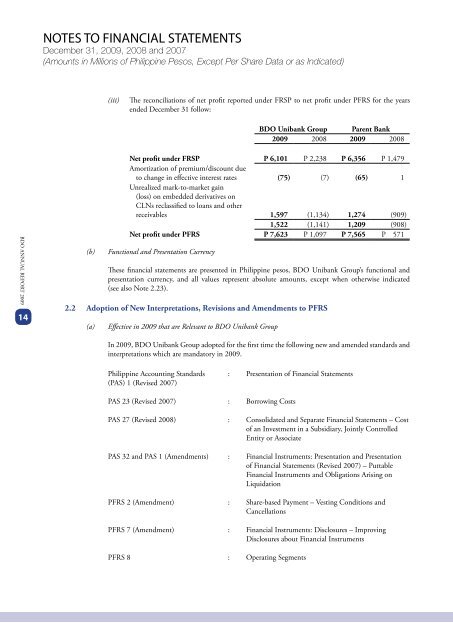

NOTES TO <strong>FINANCIAL</strong> STATEMENTSDecember 31, <strong>2009</strong>, 2008 and 2007(Amounts in Millions of Philippine Pesos, Except Per Share Data or as Indicated)(iii)The reconciliations of net profit reported under FRSP to net profit under PFRS for the yearsended December 31 follow:<strong>BDO</strong> Unibank Group Parent Bank<strong>2009</strong> 2008 <strong>2009</strong> 2008<strong>BDO</strong> <strong>ANNUAL</strong> <strong>REPORT</strong> <strong>2009</strong>14(b)Net profit under FRSP P 6,101 P 2,238 P 6,356 P 1,479Amortization of premium/discount dueto change in effective interest rates (75) (7) (65) 1Unrealized mark-to-market gain(loss) on embedded derivatives onCLNs reclassified to loans and otherreceivables 1,597 (1,134) 1,274 (909)1,522 (1,141) 1,209 (908)Net profit under PFRS P 7,623 P 1,097 P 7,565 P 571Functional and Presentation CurrencyThese financial statements are presented in Philippine pesos, <strong>BDO</strong> Unibank Group’s functional andpresentation currency, and all values represent absolute amounts, except when otherwise indicated(see also Note 2.23).2.2 Adoption of New Interpretations, Revisions and Amendments to PFRS(a)Effective in <strong>2009</strong> that are Relevant to <strong>BDO</strong> Unibank GroupIn <strong>2009</strong>, <strong>BDO</strong> Unibank Group adopted for the first time the following new and amended standards andinterpretations which are mandatory in <strong>2009</strong>.Philippine Accounting Standards(PAS) 1 (Revised 2007): Presentation of Financial StatementsPAS 23 (Revised 2007) : Borrowing CostsPAS 27 (Revised 2008) : Consolidated and Separate Financial Statements – Costof an Investment in a Subsidiary, Jointly ControlledEntity or AssociatePAS 32 and PAS 1 (Amendments) : Financial Instruments: Presentation and Presentationof Financial Statements (Revised 2007) – PuttableFinancial Instruments and Obligations Arising onLiquidationPFRS 2 (Amendment) : Share-based Payment – Vesting Conditions andCancellationsPFRS 7 (Amendment) : Financial Instruments: Disclosures – ImprovingDisclosures about Financial InstrumentsPFRS 8 : Operating Segments

NOTES TO <strong>FINANCIAL</strong> STATEMENTSDecember 31, <strong>2009</strong>, 2008 and 2007(Amounts in Millions of Philippine Pesos, Except Per Share Data or as Indicated)Philippine InterpretationInternational Financial ReportingInterpretationsCommittee (IFRIC) 13: Customer Loyalty ProgrammesVarious Standards : 2008 Annual Improvements to PFRSDiscussed below are the effects in the financial statements of the new and amended accounting standardsand interpretations.(i) PAS 1 (Revised 2007), Presentation of Financial Statements (effective from January 1, <strong>2009</strong>).The amendment requires an entity to present all items of income and expense recognized inthe period in a single statement of comprehensive income or in two statements: a separatestatement of income and a statement of comprehensive income. The statement of income shalldisclose income and expense recognized in profit or loss in the same way as the current version ofPAS 1. The statement of comprehensive income shall disclose profit or loss for the period, pluseach component of income and expense recognized outside of profit or loss or the “non-ownerchanges in equity”, which are no longer allowed to be presented in the statements of changes inequity, classified by nature (e.g., gains or losses on available-for-sale assets or translation differencesrelated to foreign operations). Changes in equity arising from transactions with owners areexcluded from the statement of comprehensive income (e.g., dividends and capital increase). Anentity is also required to include in its set of financial statements a statement showing its financialposition at the beginning of the previous period when the entity retrospectively applies anaccounting policy or makes a retrospective restatement. The adoption of PAS 1 (Revised 2007)by <strong>BDO</strong> Unibank Group did not result in any material adjustments in its financial statements.With respect to the presentation of comprehensive income, <strong>BDO</strong> Unibank Group electedto present two statements: a separate statement of income and a statement of comprehensiveincome.<strong>BDO</strong> <strong>ANNUAL</strong> <strong>REPORT</strong> <strong>2009</strong>15(ii)(iii)PAS 23 (Revised 2007), Borrowing Costs. The revised standard requires that all borrowingcosts that are directly attributable to the acquisition, construction or production of a qualifyingasset shall be capitalized as part of the cost of that asset. The option of immediately expensingborrowing costs that qualify for asset recognition had been removed. <strong>BDO</strong> Unibank Groupdetermined that the adoption of this new standard has no significant effects on the financialstatements for <strong>2009</strong>, as well as for prior and future periods, as the <strong>BDO</strong> Unibank Group’s currentaccounting policy is to capitalize all interests directly related to qualifying assets.PAS 27 (Revised 2008), Consolidated and Separate Financial Statements – Cost of an Investment in aSubsidiary, Jointly Controlled Entity or Associate. Under the revised standard, the definition of costmethod from PAS 27 was removed and dividend was required to be presented as income in theseparate financial statements of the investor. The amendments address the initial measurementrequirements for the cost of an investment in the separate financial statements of a new parentformed as the result of a specific type of reorganization, i.e., the new parent is required to measurethe cost of its investment in the previous parent at the carrying amount of its share of the equityitems of the previous parent at the date of the reorganization. Management considered theamendments to have no impact on the financial statements of <strong>BDO</strong> Unibank Group.