Download Annual Report 2006 - Foskor

Download Annual Report 2006 - Foskor

Download Annual Report 2006 - Foskor

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

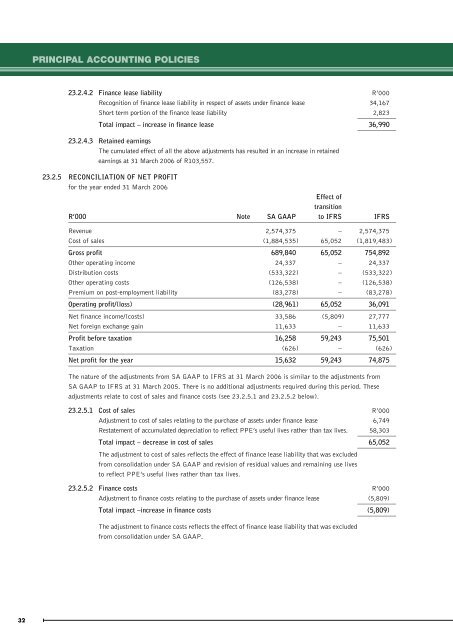

PRINCIPAL ACCOUNTING POLICIES23.2.4.2 Finance lease liability R’000Recognition of finance lease liability in respect of assets under finance lease 34,167Short term portion of the finance lease liability 2,823Total impact – increase in finance lease 36,99023.2.4.3 Retained earningsThe cumulated effect of all the above adjustments has resulted in an increase in retainedearnings at 31 March <strong>2006</strong> of R103,557.23.2.5 RECONCILIATION OF NET PROFITfor the year ended 31 March <strong>2006</strong>Effect oftransitionR’000 Note SA GAAP to IFRS IFRSRevenue 2,574,375 – 2,574,375Cost of sales (1,884,535) 65,052 (1,819,483)Gross profit 689,840 65,052 754,892Other operating income 24,337 – 24,337Distribution costs (533,322) – (533,322)Other operating costs (126,538) – (126,538)Premium on post-employment liability (83,278) – (83,278)Operating profit/(loss) (28,961) 65,052 36,091Net finance income/(costs) 33,586 (5,809) 27,777Net foreign exchange gain 11,633 – 11,633Profit before taxation 16,258 59,243 75,501Taxation (626) – (626)Net profit for the year 15,632 59,243 74,875The nature of the adjustments from SA GAAP to IFRS at 31 March <strong>2006</strong> is similar to the adjustments fromSA GAAP to IFRS at 31 March 2005. There is no additional adjustments required during this period. Theseadjustments relate to cost of sales and finance costs (see 23.2.5.1 and 23.2.5.2 below).23.2.5.1 Cost of sales R’000Adjustment to cost of sales relating to the purchase of assets under finance lease 6,749Restatement of accumulated depreciation to reflect PPE’s useful lives rather than tax lives. 58,303Total impact – decrease in cost of sales 65,052The adjustment to cost of sales reflects the effect of finance lease liability that was excludedfrom consolidation under SA GAAP and revision of residual values and remaining use livesto reflect PPE’s useful lives rather than tax lives.23.2.5.2 Finance costs R’000Adjustment to finance costs relating to the purchase of assets under finance lease (5,809)Total impact –increase in finance costs (5,809)The adjustment to finance costs reflects the effect of finance lease liability that was excludedfrom consolidation under SA GAAP.32