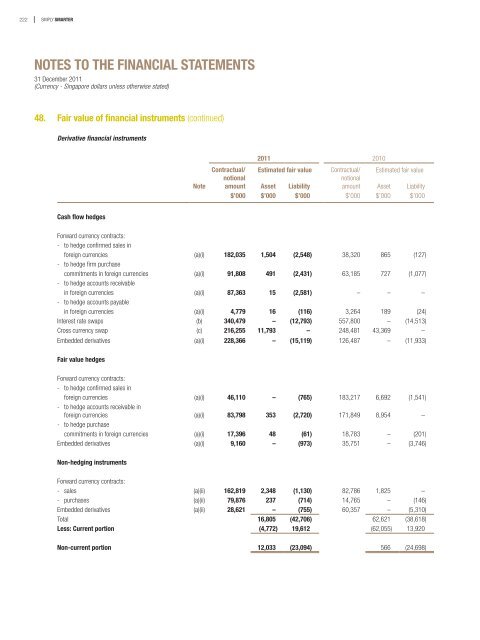

222 SIMPLY SMARTERNOTES TO THE FINANCIAL STATEMENTS31 December 2011(Currency - <strong>Singapore</strong> dollars unless o<strong>the</strong>rwise stated)48. Fair value of <strong>financial</strong> instruments (continued)Derivative <strong>financial</strong> instrumentsNote2011 2010Contractual/ Estimated fair value Contractual/ Estimated fair valuenotionalnotionalamount Asset Liability amount Asset Liability$’000 $’000 $’000 $’000 $’000 $’000Cash flow hedgesForward currency contracts:- <strong>to</strong> hedge confirmed sales inforeign currencies (a)(i) 182,035 1,504 (2,548) 38,320 865 (127)- <strong>to</strong> hedge firm purchasecommitments in foreign currencies (a)(i) 91,808 491 (2,431) 63,185 727 (1,077)- <strong>to</strong> hedge accounts receivablein foreign currencies (a)(i) 87,363 15 (2,581) – – –- <strong>to</strong> hedge accounts payablein foreign currencies (a)(i) 4,779 16 (116) 3,264 189 (24)Interest rate swaps (b) 340,479 – (12,793) 557,800 – (14,513)Cross currency swap (c) 216,255 11,793 – 248,481 43,369 –Embedded derivatives (a)(i) 228,366 – (15,119) 126,487 – (11,933)Fair value hedgesForward currency contracts:- <strong>to</strong> hedge confirmed sales inforeign currencies (a)(i) 46,110 – (765) 183,217 6,692 (1,541)- <strong>to</strong> hedge accounts receivable inforeign currencies (a)(i) 83,798 353 (2,720) 171,849 8,954 –- <strong>to</strong> hedge purchasecommitments in foreign currencies (a)(i) 17,396 48 (61) 18,783 – (201)Embedded derivatives (a)(i) 9,160 – (973) 35,751 – (3,746)Non-hedging instrumentsForward currency contracts:- sales (a)(ii) 162,819 2,348 (1,130) 82,786 1,825 –- purchases (a)(ii) 79,876 237 (714) 14,765 – (146)Embedded derivatives (a)(ii) 28,621 – (755) 60,357 – (5,310)Total 16,805 (42,706) 62,621 (38,618)Less: Current portion (4,772) 19,612 (62,055) 13,920Non-current portion 12,033 (23,094) 566 (24,698)

SINGAPORE TECHNOLOGIES ENGINEERING LTD Annual Report 2011223NOTES TO THE FINANCIAL STATEMENTS31 December 2011(Currency - <strong>Singapore</strong> dollars unless o<strong>the</strong>rwise stated)48. Fair value of <strong>financial</strong> instruments (continued)(a)Forward currency contracts(i)As at 31 December 2011, <strong>the</strong> Group has forward currency contracts and embedded derivatives separated from <strong>the</strong> foreign currencyportion of sales contracts amounting <strong>to</strong> $750,815,000 (2010: $640,856,000) designated as hedges of confirmed sales in foreigncurrencies, firm purchase commitments in foreign currencies, accounts receivable in foreign currencies and accounts payable inforeign currencies.The maturity dates of <strong>the</strong> forward currency contracts and embedded derivatives separated from <strong>the</strong> foreign currency portion of <strong>the</strong>sales contracts approximate <strong>the</strong> timing of <strong>the</strong> expected cash flows of <strong>the</strong>ir respective hedged items, which are on varying periods up<strong>to</strong> 6 years from <strong>the</strong> <strong>financial</strong> year-end.(ii)As at 31 December 2011, <strong>the</strong> Group has outstanding forward currency contracts and embedded derivatives separated from <strong>the</strong>foreign currency portion of sales contracts amounting <strong>to</strong> $271,316,000 (2010: $157,908,000), which are not designated as hedgesof confirmed sales in foreign currencies and firm purchase commitments in foreign currencies.(b)Interest rate swapsAs at 31 December 2011, <strong>the</strong> Group has outstanding interest rate swaps amounting <strong>to</strong> $340,479,000 (2010: $557,800,000), which aredesignated as cash flow hedges.The USD interest rate swaps are being used <strong>to</strong> hedge <strong>the</strong> exposure <strong>to</strong> variability in cash flows associated with <strong>the</strong> floating rate of <strong>the</strong> unsecuredUSD long-term loans. Under <strong>the</strong> USD interest rate swaps, <strong>the</strong> Group pays fixed rates of interest of 3.68% <strong>to</strong> 3.80% (2010: 3.68% <strong>to</strong> 3.86%)per annum and receives variable rates of interest equal <strong>to</strong> <strong>the</strong> LIBOR per annum on <strong>the</strong> notional amount. The USD interest rate swaps have <strong>the</strong>same maturity terms as <strong>the</strong> unsecured USD long-term loans due in 2013.During <strong>the</strong> year, <strong>the</strong> Group entered in<strong>to</strong> a new Euro interest rate swap which is used <strong>to</strong> hedge 72% of <strong>the</strong> exposure <strong>to</strong> variability in cash flowsassociated with <strong>the</strong> floating rate of a cross currency swap. Under <strong>the</strong> Euro interest rate swap, <strong>the</strong> Group pays a fixed rate of interest of 2.50%per annum and receives a variable rate of interest equal <strong>to</strong> <strong>the</strong> EURIBOR per annum on <strong>the</strong> notional amount. The Euro interest rate swap has <strong>the</strong>same maturity terms as <strong>the</strong> cross currency swap.In <strong>the</strong> prior year, <strong>the</strong> Group had a Euro interest rate swap which <strong>the</strong> Group paid a fixed rate of interest of 2.95% per annum and received avariable rate of interest equal <strong>to</strong> <strong>the</strong> EURIBOR + 1.2% per annum on <strong>the</strong> notional amount. The cross interest rate swap matured during <strong>the</strong> year.(c)Cross currency swapAs at 31 December 2011, <strong>the</strong> Group has an outstanding cross currency swap amounting <strong>to</strong> $216,255,000 (2010: $248,481,000), which isdesignated as hedging instrument in a cash flow hedge relationship.During <strong>the</strong> year, <strong>the</strong> Group entered in<strong>to</strong> a new USD cross currency swap which is used <strong>to</strong> hedge foreign currency exposure of a USD bank loanmaturing in 2014. It converts <strong>the</strong> USD bank loan with floating USD interest rate at LIBOR + 0.60% per annum <strong>to</strong> an equivalent Euro bank loan(Euro 120,000,000) with floating Euro interest rate at EURIBOR + 0.41% per annum.In <strong>the</strong> prior year, <strong>the</strong> Group had a SGD cross currency swap which converted a SGD bank loan with floating SGD interest rate at SIBOR + 1.325%per annum <strong>to</strong> an equivalent Euro bank loan (Euro 112,300,000) with floating Euro interest rate at EURIBOR + 1.2% per annum. The crosscurrency swap matured during <strong>the</strong> year.