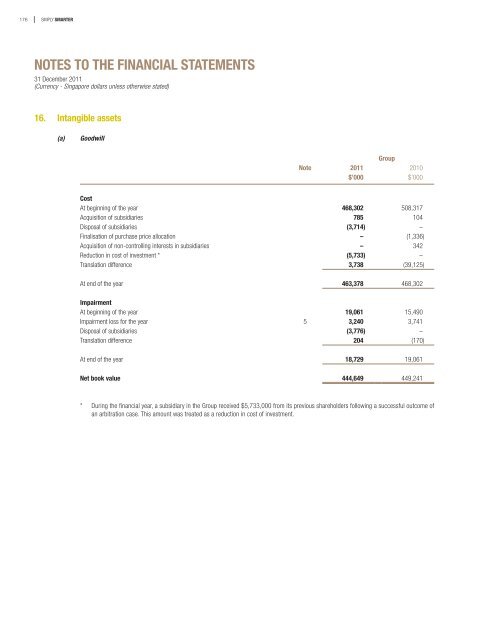

176 SIMPLY SMARTERNOTES TO THE FINANCIAL STATEMENTS31 December 2011(Currency - <strong>Singapore</strong> dollars unless o<strong>the</strong>rwise stated)16. Intangible assets(a)GoodwillGroupNote 2011 2010$’000 $’000CostAt beginning of <strong>the</strong> year 468,302 508,317Acquisition of subsidiaries 785 104Disposal of subsidiaries (3,714) –Finalisation of purchase price allocation – (1,336)Acquisition of non-controlling interests in subsidiaries – 342Reduction in cost of investment * (5,733) –Translation difference 3,738 (39,125)At end of <strong>the</strong> year 463,378 468,302ImpairmentAt beginning of <strong>the</strong> year 19,061 15,490Impairment loss for <strong>the</strong> year 5 3,240 3,741Disposal of subsidiaries (3,776) –Translation difference 204 (170)At end of <strong>the</strong> year 18,729 19,061Net book value 444,649 449,241* During <strong>the</strong> <strong>financial</strong> year, a subsidiary in <strong>the</strong> Group received $5,733,000 from its previous shareholders following a successful outcome ofan arbitration case. This amount was treated as a reduction in cost of investment.

SINGAPORE TECHNOLOGIES ENGINEERING LTD Annual Report 2011177NOTES TO THE FINANCIAL STATEMENTS31 December 2011(Currency - <strong>Singapore</strong> dollars unless o<strong>the</strong>rwise stated)16. Intangible assets (continued)(b)O<strong>the</strong>r intangible assetsNoteDealernetworkDevelopmentexpenditureCommercialandintellectualpropertyrightsFilm costinven<strong>to</strong>ry Brands O<strong>the</strong>rs Total$’000 $’000 $’000 $’000 $’000 $’000 $’000The GroupCostAt 1.1.2010 9,132 12,971 68,080 11,583 83,239 5,021 190,026Additions – 3,231 1,256 220 – – 4,707Finalisation of purchase priceallocation – – – – – 1,336 1,336Write-off – (2,153) – – – – (2,153)Translation difference (754) (434) (5,024) – (6,981) 7 (13,186)At 31.12.2010 and at 1.1.2011 8,378 13,615 64,312 11,803 76,258 6,364 180,730Additions – 2,803 – – – – 2,803Acquisition of a subsidiary – – – – 248 648 896Disposal of a subsidiary – (2,082) – – – – (2,082)Translation difference 67 335 530 – 592 1 1,525At 31.12.2011 8,445 14,671 64,842 11,803 77,098 7,013 183,872Accumulated amortisationAt 1.1.2010 4,683 2,326 24,544 744 3,687 2,468 38,452Amortisation for <strong>the</strong> year 5 1,266 1,155 6,926 13 1,258 472 11,090Impairment loss 5 – 815 – 4,123 – – 4,938Write-off – (2,063) – – – – (2,063)Translation difference (454) (118) (2,017) – (380) – (2,969)At 31.12.2010 and 1.1.2011 5,495 2,115 29,453 4,880 4,565 2,940 49,448Amortisation for <strong>the</strong> year 5 778 1,175 5,680 – 1,169 473 9,275Impairment loss 5 – – 874 6,090 – – 6,964Disposal of a subsidary – (2,082) – – – – (2,082)Translation difference 71 81 459 – 67 – 678At 31.12.2011 6,344 1,289 36,466 10,970 5,801 3,413 64,283Net book valueAt 31.12.2011 2,101 13,382 28,376 833 71,297 3,600 119,589At 31.12.2010 2,883 11,500 34,859 6,923 71,693 3,424 131,282Impairment of film cost inven<strong>to</strong>ryAn impairment test relating <strong>to</strong> <strong>the</strong> carrying amount of film cost inven<strong>to</strong>ry was triggered during <strong>the</strong> <strong>financial</strong> year as a result of revised salesforecasts and actual sales data received from <strong>the</strong> film producers. The recoverable amount was estimated based on its value in use basedon sales forecasts provided by <strong>the</strong> producers and using a discount rate of 8.49% (2010: 5.7%). The carrying amount of <strong>the</strong> film inven<strong>to</strong>rywas determined <strong>to</strong> be higher than its recoverable amount and an impairment loss of $6,090,000 (2010: $4,123,000) was recognised. Theimpairment loss is recognised in cost of sales in <strong>the</strong> income statement.