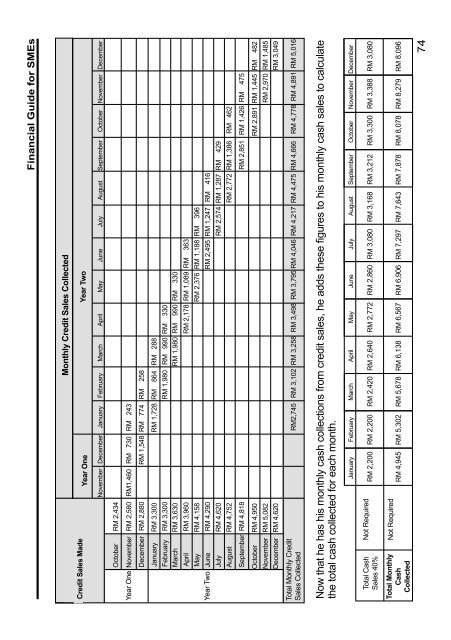

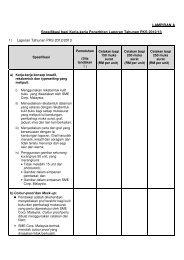

<strong>Financial</strong> <strong>Guide</strong> <strong>for</strong> <strong><strong>SME</strong>s</strong><strong>Financial</strong> <strong>Guide</strong> <strong>for</strong> <strong><strong>SME</strong>s</strong>Monthly Credit Sales CollectedCredit Sales MadeYear OneYear TwoNovember December January February March April May June July August September October November DecemberOctober RM 2,434Year OneNovember RM 2,580 RM1,460 RM 730 RM 243December RM 2,880 RM 1,548 RM 774 RM 258Year TwoJanuary RM 3,300 RM 1,728 RM 864 RM 288February RM 3,300 RM 1,980 RM 990 RM 330March RM 3,630 RM 1,980 RM 990 RM 330April RM 3,960 RM 2,178 RM 1,089 RM 363May RM 4,158 RM 2,376 RM 1,188 RM 396June RM 4,290 RM 2,495 RM 1,247 RM 416July RM 4,620 RM 2,574 RM 1,287 RM 429August RM 4,752 RM 2,772 RM 1,386 RM 462September RM 4,818 RM 2,851 RM 1,426 RM 475October RM 4,950 RM 2,891 RM 1,445 RM 482November RM 5,082 RM 2,970 RM 1,485December RM 4,620 RM 3,049Total Monthly CreditSales CollectedRM2,745 RM 3,102 RM 3,258 RM 3,498 RM 3,795 RM 4,046 RM 4,217 RM 4,475 RM 4,666 RM 4,778 RM 4,891 RM 5,016Now that he has his monthly cash collections from credit sales, he adds these figures to his monthly cash sales to calculatethe total cash collected <strong>for</strong> each month.January February March April May June July August September October November DecemberTotal CashSales 40%Not RequiredTotal MonthlyCashCollectedNot Required7474Chapter 6 p66-78 Eng.indd 748/15/11 5:02:25 PM

<strong>Financial</strong> <strong>Guide</strong> <strong>for</strong> <strong><strong>SME</strong>s</strong>Step 3: Other Cash InflowsTo complete the cash infl ow in<strong>for</strong>mation in the cash fl ow <strong>for</strong>ecast, you will needto identify any additional cash coming into the business. Of course, the types ofcash infl ows <strong>for</strong> each business will vary, but the following list may help you torecognise other cash infl ows in your business:• Additional equity contribution;• Income tax refunds;• Grants;• Loan proceeds;• Other income sources not included in sales (e.g. royalties, franchise andlicense fees); and• Proceeds from sale of assets.If you are preparing a cash fl ow <strong>for</strong>ecast <strong>for</strong> additional fi nancing, do not <strong>for</strong>getto include the loan funds in your infl ows.Step 4: Cash OutflowsAs we have indicated earlier, one of the major inputs into the <strong>for</strong>ecast is sales.Coupled with this infl ow is the cost of purchasing or manufacturing those goodsto sell. There<strong>for</strong>e, when determining your cash outfl ows, it is suggested <strong>for</strong> youto calculate the cost of goods sold in line with your sales <strong>for</strong>ecast. By doing this,if you need to change your sales numbers, an automatic change to the cost ofgoods sold fi gure should occur. Many computer programmes will allow you toset up a link between two items, such as your sales and cost of goods sold, tomake the process of <strong>for</strong>ecasting easier. The calculation of cost of goods soldwas discussed in Chapter 1, so you may want to refer back to the section or usethe gross margin percentage discussed in Chapter 4 when estimating the costof goods sold <strong>for</strong> your <strong>for</strong>ecast.ExpensesExpenses are those cash outfl ows relating to the operations of the businessand those that are not included in the cost of goods calculation. These are oftenreferred to as ”administration” or ”operational” expenditure. Again, the itemsof expense will depend on the type of business you are starting or currentlyoperating. One of the important areas to focus on when <strong>for</strong>ecasting expensesis the classifi cation. Remember in Chapter 4, the difference between fi xed andvariable expenses was discussed. When putting together your <strong>for</strong>ecast, thevariable expenses will be directly related to the <strong>for</strong>ecast sales numbers. So ifyou adjust your sales, these expenses will need to be amended in line with thesales adjustment. Of course, the fi xed expenses will remain the same, althoughyou may need to consider adjusting these <strong>for</strong> increases (e.g. infl ation).75Chapter 6 p66-78 Eng.indd 758/15/11 5:02:25 PM