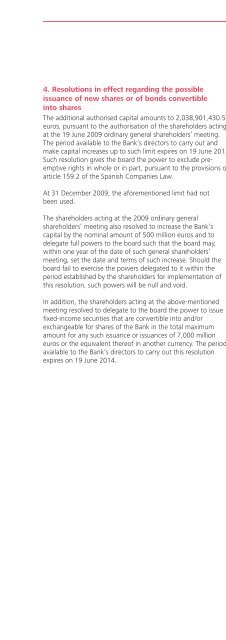

114Latin America• In the current context, focus on customer linkage,transaction banking, control of costs and riskmanagement.• Sound revenues from the moderate increase in businessactivity, improved spreads on assets and GBM’scontribution.• Slower pace in nominal costs, reflecting the moreselective growth policy.• Strong net operating income which, after absorbing thelarger provisions, increased 19.4% (excluding theexchange-rate impact).• Intense management of early NPLs and their recovery.<strong>Santander</strong> generated attributable profit of EUR 3,833 million in<strong>2009</strong>, 6.2% more than in 2008 (+11.4% excluding theexchange-rate impact), after incorporating the results of BancoReal in Brazil.As mentioned in other parts of this <strong>report</strong>, the 2008 figures havebeen restated to include Banco Real by global integration inorder to provide like-for-like comparisons. In July, Banco deVenezuela was sold to the Republic of Venezuela via Banco deDesarrollo de Venezuela for $1,050 million. The results of thisbank in 2008 and <strong>2009</strong> have been eliminated from the variouslines and incorporated on a net basis to discontinuedoperations.Gross income and expenses*% variation in euros <strong>2009</strong> / 2008+9.3GrossincomeExpenses-7.1* Excluding exchange rate impact: Gross income:+14.8%; expenses: -2.6%Net operating incomeMillion euros9,072200811,071<strong>2009</strong>+22.0%*Efficiency ratio(with amortisations)%43.92008 <strong>2009</strong>Attributable profitMillion euros3,8333,6092008<strong>2009</strong>37.3+6.2%** Excluding exchange rate impact: +28.4% * Excluding exchange rate impact: +11.4%Economic environmentThe region’s main economies began to show signs as of thethird quarter of emerging from the recession started at the endof 2008, and today the general perception is that this time LatinAmerica has satisfactorily withstood the global crisis.NPL ratio%2.954.25NPL coverage%108105Three factors played a role in this:• First, the Brazilian economy, which accounts for 40% of theregion’s GDP, began to grow in the second quarter and withsuch intensity that its GDP did not fall for the year as a whole.Peru was also able to grow in <strong>2009</strong> (by more than 1%). Brazilthus consolidated its model and together with Chile’s becamethe “second success story” in the region.• Second, for the first time in 50 years, Latin America was ableto implement anti-cyclical monetary and fiscal policies tomitigate the impact of external shocks. The most notable casewas Chile, a country whose strong institutions and orthodoxyenabled fiscal and monetary impulses of around 10% and 6%of GDP, respectively. As a result, Chile was one of the fewreally open economies in the world whose GDP declined byless than 2%.• Third, the region was able to avoid any banking crisisepisodes. Furthermore, this time Latin American banks werenot part of the problem but of the solution and the nominalstock of lending was maintained. Brazil was largelyresponsible for this development and increased its share of theregion’s total lending to 60% of the total stock.2008<strong>2009</strong>2008 <strong>2009</strong>As well as other good developments, most of the region’s largeeconomies were able to get through <strong>2009</strong> without eroding thequality of their institutions, their rules and their basicmacroeconomic fundamentals. As a result, inflation, except inVenezuela and Argentina, is expected to be no more than 5% in2010 and within the target ranges of central banks.Budget deficits in all countries are also expected to be below3% of GDP and net public debt below 40% of GDP. Theimprovement in the international prices of raw materials and thereduction in risk premiums since March <strong>2009</strong> point to GDPgrowth of more than 3.5% and to job creation.<strong>Annual</strong> Report <strong>2009</strong>Economic and Financial Review

115In the countries where <strong>Santander</strong> operates – Brazil, Mexico,Chile, Argentina, Colombia, Puerto Rico, Uruguay and Peru – thepace of lending slowed sharply (6% in <strong>2009</strong>, excluding theexchange-rate impact). Overall, loans to individuals grew 8%and continued to decelerate for other concepts (cards: -2%;consumer: +11%; mortgages: +8% and to companies andinstitutions +5%).Savings (deposits and mutual funds) increased 13%, with aslight jump in the fourth quarter after a sharp deceleration in thefirst half of the year. In general terms, and based on the mainfinancial systems, Brazil’s growth was the strongest and Chile’sslowed the most.The following factors regarding the impact of interest rates andexchange rates on business and converting figures into eurosshould be taken into account when analysing the financialinformation:– The weighted average of the region’s medium- and shortterminterest rates fell between 2008 and <strong>2009</strong>. In generalterms, interest rates registered a sharp fall during <strong>2009</strong>.– Earnings in euros are impacted by average exchange rates. Inglobal terms, Latin American currencies depreciated againstthe dollar while the dollar, the currency used to managebusiness in Latin America, strengthened against the euro by5%. The Brazilian real slid against the euro from 2.66 to 2.76,the Mexican peso from 16.3 to 18.8 and the Chilean pesofrom 757 to 775.Strategy in <strong>2009</strong>Given the economic downturn and the greater degree ofuncertainty in markets, the strategy focused on customermanagement (based on linkage and transactions), higherspreads on loans, rigorous management of risks, with a greateremphasis on recoveries, and lower growth in costs reflecting amore selective policy.In Brazil, Banco Real’s consolidation gave the strategy somefeatures that differentiated it. Of note was Banco <strong>Santander</strong>Brazil’s capital increase through a new share offer in the secondhalf of <strong>2009</strong>, the proceeds of which will finance the strategicplan in the coming years.In Puerto Rico, and in order to find a solution to the lack ofliquidity of the <strong>Santander</strong> share and cut costs and administrativeexpenses, on December 14 Grupo <strong>Santander</strong> announced itsintention to acquire 9.4% of <strong>Santander</strong> Bancorp and delist it onthe New York Stock Exchange.Grupo <strong>Santander</strong> had 5,754 branches at the end of <strong>2009</strong>(including traditional ones and points of banking attention),while the number of ATMs was 27,000.Lending to individuals and SMEs accounts for 59% of theGroup’s total loans in Latin America. After several years ofincreasing its market share of non-mortgage loans to individuals(cards, consumer), the Group applied tighter criteria because ofthe increase in its risk premium and the perception of an erosionof its credit quality in some of the countries where it operates.The risk premium reached 4.75% in <strong>2009</strong>.Activity and income statementThe main developments in <strong>2009</strong> (all year-on-year percentagechanges exclude the exchange-rate impact and the exit fromthe perimeter of consolidation of Banco de Venezuela) were:• The pace of lending continued to decline, with consumercredit and cards down 3%, mortgages up 11% andcommercial credit (companies in all their range andinstitutions) falling 3%. Loans to individuals increased 3%,that to SMEs dropped 2% and to companies 11%. Theshare of total lending in the countries where the Groupoperates is 11.5%.• Savings (deposits without repos and mutual funds) hardlychanged. Demand deposits grew 13% and mutual funds16%, while time deposits declined 17%. The market share indeposits and mutual funds was 9.5% and 9.6% in demanddeposits. The overall market share (loans, deposits and mutualfunds) was 10.2%.• Due to the weak economic situation, the Group is placing lessemphasis on market shares in retail lending, while inwholesale business the focus is on providing transactionservices and hedging risks (exchange rates, interest rates) andactive participation in restructurings.• Net interest income increased 9.9%. The rise in spreads onloans was due to the measures taken to increase entry pricesand try to offset the higher cost of financing in the marketsand the higher risk premium. Spreads on loans (withdifferences between countries) were higher than in 2008. Asfor spreads on deposits, after falling they stabilised to someextent (falls in year-end rates compared to 2008 of 375 b.p. inMexico, 500 b.p. in Brazil, 600 b.p. in Colombia and 775 b.p.in Chile).• Net fee income rose 4.1%. That from mutual funds declined9.9%, while that from foreign trade and, to a lesser extent,cards and insurance grew. Income from the administration ofaccounts dropped, impacted by regulatory changes in most ofthe region. The slower pace of business also affected feeincome.• Gains on financial transactions increased 144.2%, due togood results in customer activity and capital gains.• As a result, gross income increased 14.8%.The total number of customers was 37.7 million, 1.6 millionmore than in 2008 on a like-for-like basis (including Banco Realin Brazil and ABN-AMRO in Uruguay and excluding Venezuela).The Group’s strategic focus in the last few quarters has been oncustomer linkage. Thus, the number of linked customersaccount for 30% of total customers in the region.Economic and Financial Review<strong>Annual</strong> Report <strong>2009</strong>