AUDIT ANALYTICS AUDIT

1JWn3ix

1JWn3ix

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

ESSAY 6: MANAGING RISK AND THE <strong>AUDIT</strong> PROCESS<br />

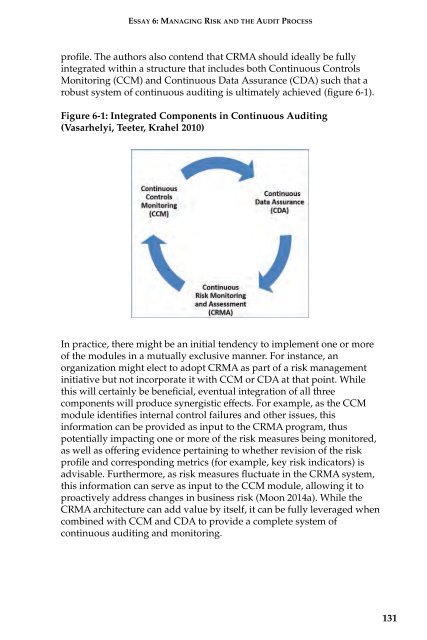

profile. The authors also contend that CRMA should ideally be fully<br />

integrated within a structure that includes both Continuous Controls<br />

Monitoring (CCM) and Continuous Data Assurance (CDA) such that a<br />

robust system of continuous auditing is ultimately achieved (figure 6-1).<br />

Figure 6-1: Integrated Components in Continuous Auditing<br />

(Vasarhelyi, Teeter, Krahel 2010)<br />

In practice, there might be an initial tendency to implement one or more<br />

of the modules in a mutually exclusive manner. For instance, an<br />

organization might elect to adopt CRMA as part of a risk management<br />

initiative but not incorporate it with CCM or CDA at that point. While<br />

this will certainly be beneficial, eventual integration of all three<br />

components will produce synergistic effects. For example, as the CCM<br />

module identifies internal control failures and other issues, this<br />

information can be provided as input to the CRMA program, thus<br />

potentially impacting one or more of the risk measures being monitored,<br />

as well as offering evidence pertaining to whether revision of the risk<br />

profile and corresponding metrics (for example, key risk indicators) is<br />

advisable. Furthermore, as risk measures fluctuate in the CRMA system,<br />

this information can serve as input to the CCM module, allowing it to<br />

proactively address changes in business risk (Moon 2014a). While the<br />

CRMA architecture can add value by itself, it can be fully leveraged when<br />

combined with CCM and CDA to provide a complete system of<br />

continuous auditing and monitoring.<br />

131