AUDIT ANALYTICS AUDIT

1JWn3ix

1JWn3ix

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

<strong>AUDIT</strong> <strong>ANALYTICS</strong> AND CONTINUOUS <strong>AUDIT</strong>:LOOKING TOWARD THE FUTURE<br />

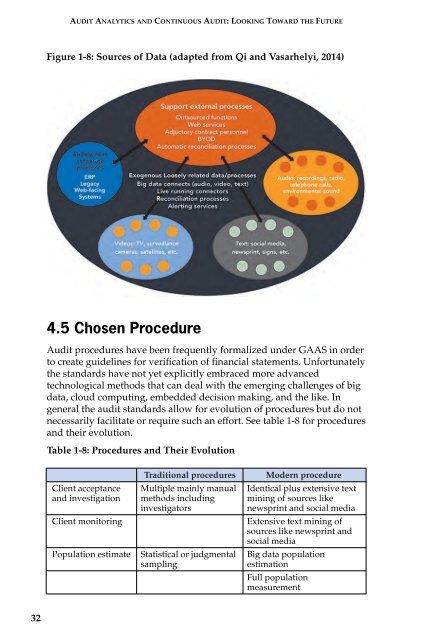

Figure 1-8: Sources of Data (adapted from Qi and Vasarhelyi, 2014)<br />

4.5 Chosen Procedure<br />

Audit procedures have been frequently formalized under GAAS in order<br />

to create guidelines for verification of financial statements. Unfortunately<br />

the standards have not yet explicitly embraced more advanced<br />

technological methods that can deal with the emerging challenges of big<br />

data, cloud computing, embedded decision making, and the like. In<br />

general the audit standards allow for evolution of procedures but do not<br />

necessarily facilitate or require such an effort. See table 1-8 for procedures<br />

and their evolution.<br />

Table 1-8: Procedures and Their Evolution<br />

Client acceptance<br />

and investigation<br />

Client monitoring<br />

Population estimate<br />

Traditional procedures<br />

Multiple mainly manual<br />

methods including<br />

investigators<br />

Statistical or judgmental<br />

sampling<br />

Modern procedure<br />

Identical plus extensive text<br />

mining of sources like<br />

newsprint and social media<br />

Extensive text mining of<br />

sources like newsprint and<br />

social media<br />

Big data population<br />

estimation<br />

Full population<br />

measurement<br />

32