AUDIT ANALYTICS AUDIT

1JWn3ix

1JWn3ix

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

ESSAY 1: CONTINUOUS <strong>AUDIT</strong>ING—A NEW VIEW<br />

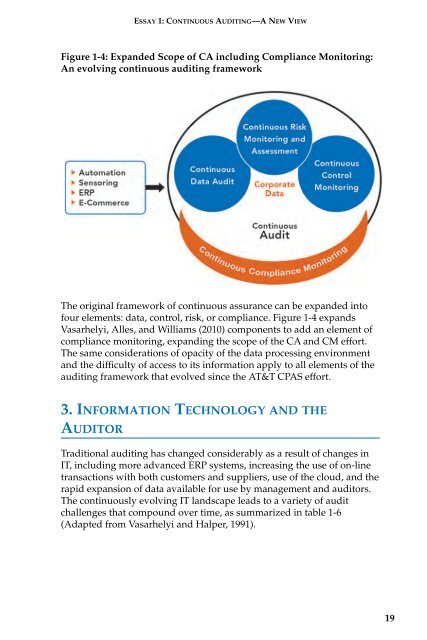

Figure 1-4: Expanded Scope of CA including Compliance Monitoring:<br />

An evolving continuous auditing framework<br />

The original framework of continuous assurance can be expanded into<br />

four elements: data, control, risk, or compliance. Figure 1-4 expands<br />

Vasarhelyi, Alles, and Williams (2010) components to add an element of<br />

compliance monitoring, expanding the scope of the CA and CM effort.<br />

The same considerations of opacity of the data processing environment<br />

and the difficulty of access to its information apply to all elements of the<br />

auditing framework that evolved since the AT&T CPAS effort.<br />

3. INFORMATION TECHNOLOGY AND THE<br />

<strong>AUDIT</strong>OR<br />

Traditional auditing has changed considerably as a result of changes in<br />

IT, including more advanced ERP systems, increasing the use of on-line<br />

transactions with both customers and suppliers, use of the cloud, and the<br />

rapid expansion of data available for use by management and auditors.<br />

The continuously evolving IT landscape leads to a variety of audit<br />

challenges that compound over time, as summarized in table 1-6<br />

(Adapted from Vasarhelyi and Halper, 1991).<br />

19