AUDIT ANALYTICS AUDIT

1JWn3ix

1JWn3ix

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

<strong>AUDIT</strong> <strong>ANALYTICS</strong> AND CONTINUOUS <strong>AUDIT</strong>:LOOKING TOWARD THE FUTURE<br />

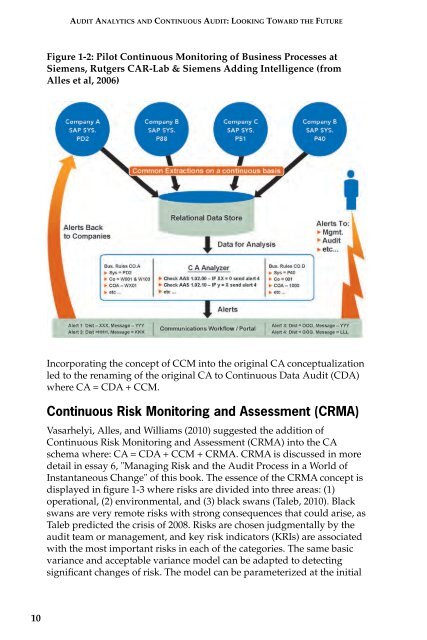

Figure 1-2: Pilot Continuous Monitoring of Business Processes at<br />

Siemens, Rutgers CAR-Lab & Siemens Adding Intelligence (from<br />

Alles et al, 2006)<br />

Incorporating the concept of CCM into the original CA conceptualization<br />

led to the renaming of the original CA to Continuous Data Audit (CDA)<br />

where CA = CDA + CCM.<br />

Continuous Risk Monitoring and Assessment (CRMA)<br />

Vasarhelyi, Alles, and Williams (2010) suggested the addition of<br />

Continuous Risk Monitoring and Assessment (CRMA) into the CA<br />

schema where: CA = CDA + CCM + CRMA. CRMA is discussed in more<br />

detail in essay 6, "Managing Risk and the Audit Process in a World of<br />

Instantaneous Change" of this book. The essence of the CRMA concept is<br />

displayed in figure 1-3 where risks are divided into three areas: (1)<br />

operational, (2) environmental, and (3) black swans (Taleb, 2010). Black<br />

swans are very remote risks with strong consequences that could arise, as<br />

Taleb predicted the crisis of 2008. Risks are chosen judgmentally by the<br />

audit team or management, and key risk indicators (KRIs) are associated<br />

with the most important risks in each of the categories. The same basic<br />

variance and acceptable variance model can be adapted to detecting<br />

significant changes of risk. The model can be parameterized at the initial<br />

10