AUDIT ANALYTICS AUDIT

1JWn3ix

1JWn3ix

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

CASE STUDY A: DEVELOPING CONTINUOUS ASSURANCE AT SIEMENS<br />

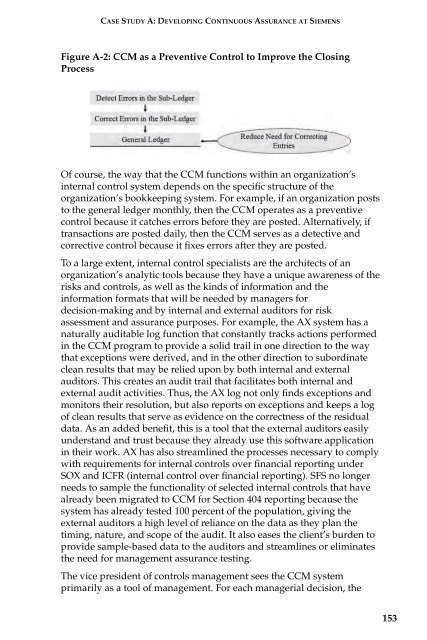

Figure A-2: CCM as a Preventive Control to Improve the Closing<br />

Process<br />

Of course, the way that the CCM functions within an organization’s<br />

internal control system depends on the specific structure of the<br />

organization’s bookkeeping system. For example, if an organization posts<br />

to the general ledger monthly, then the CCM operates as a preventive<br />

control because it catches errors before they are posted. Alternatively, if<br />

transactions are posted daily, then the CCM serves as a detective and<br />

corrective control because it fixes errors after they are posted.<br />

To a large extent, internal control specialists are the architects of an<br />

organization’s analytic tools because they have a unique awareness of the<br />

risks and controls, as well as the kinds of information and the<br />

information formats that will be needed by managers for<br />

decision-making and by internal and external auditors for risk<br />

assessment and assurance purposes. For example, the AX system has a<br />

naturally auditable log function that constantly tracks actions performed<br />

in the CCM program to provide a solid trail in one direction to the way<br />

that exceptions were derived, and in the other direction to subordinate<br />

clean results that may be relied upon by both internal and external<br />

auditors. This creates an audit trail that facilitates both internal and<br />

external audit activities. Thus, the AX log not only finds exceptions and<br />

monitors their resolution, but also reports on exceptions and keeps a log<br />

of clean results that serve as evidence on the correctness of the residual<br />

data. As an added benefit, this is a tool that the external auditors easily<br />

understand and trust because they already use this software application<br />

in their work. AX has also streamlined the processes necessary to comply<br />

with requirements for internal controls over financial reporting under<br />

SOX and ICFR (internal control over financial reporting). SFS no longer<br />

needs to sample the functionality of selected internal controls that have<br />

already been migrated to CCM for Section 404 reporting because the<br />

system has already tested 100 percent of the population, giving the<br />

external auditors a high level of reliance on the data as they plan the<br />

timing, nature, and scope of the audit. It also eases the client’s burden to<br />

provide sample-based data to the auditors and streamlines or eliminates<br />

the need for management assurance testing.<br />

The vice president of controls management sees the CCM system<br />

primarily as a tool of management. For each managerial decision, the<br />

153