Europe

From Crisis to opportunity Global Investor, 01/2014 Credit Suisse

From Crisis to opportunity

Global Investor, 01/2014

Credit Suisse

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

GLOBAL INVESTOR 1.14 — 42 1999<br />

Has Spanish<br />

competitiveness<br />

become more<br />

German?<br />

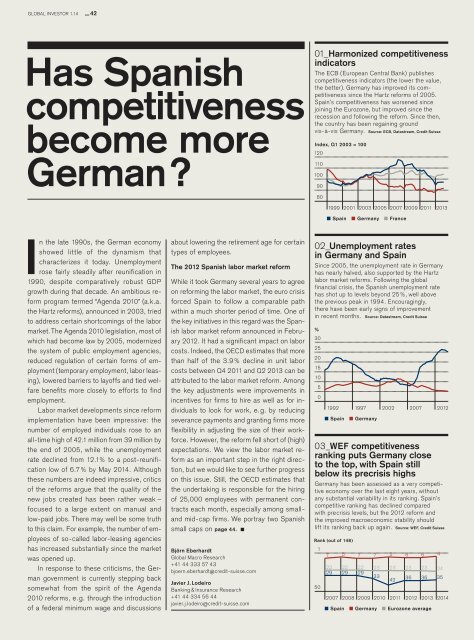

01_Harmonized competitiveness<br />

indicators<br />

The ECB (<strong>Europe</strong>an Central Bank) publishes<br />

competitiveness indicators (the lower the value,<br />

the better). Germany has improved its competitiveness<br />

since the Hartz reforms of 2005.<br />

Spain’s competitiveness has worsened since<br />

joining the Eurozone, but improved since the<br />

recession and following the reform. Since then,<br />

the country has been regaining ground<br />

vis-à-vis Germany. Source: ECB, Datastream, Credit Suisse<br />

<br />

120<br />

110<br />

100<br />

90<br />

80<br />

2001 2003 2005 2007 2009 2011 2013<br />

Spain Germany France<br />

n the late 1990s, the German economy<br />

showed little of the dynamism that<br />

characterizes it today. Unemployment<br />

rose fairly steadily after reunification in<br />

1990, despite comparatively robust GDP<br />

growth during that decade. An ambitious reform<br />

program termed “Agenda 2010” (a.k.a.<br />

the Hartz reforms), announced in 2003, tried<br />

to address certain shortcomings of the labor<br />

market. The Agenda 2010 legislation, most of<br />

which had become law by 2005, modernized<br />

the system of public employment agencies,<br />

reduced regulation of certain forms of employment<br />

(temporary employment, labor leasing),<br />

lowered barriers to layoffs and tied welfare<br />

benefits more closely to efforts to find<br />

employment.<br />

Labor market developments since re form<br />

implementation have been impressive: the<br />

number of employed individuals rose to an<br />

all-time high of 42.1 million from 39 million by<br />

the end of 2005, while the unemployment<br />

rate declined from 12.1 % to a post-reunification<br />

low of 6.7 % by May 2014. Although<br />

these numbers are indeed impressive, critics<br />

of the reforms argue that the quality of the<br />

new jobs created has been rather weak –<br />

focused to a large extent on manual and<br />

low-paid jobs. There may well be some truth<br />

to this claim. For example, the number of employees<br />

of so-called labor-leasing agencies<br />

has increased substantially since the market<br />

was opened up.<br />

In response to these criticisms, the German<br />

government is currently stepping back<br />

somewhat from the spirit of the Agenda<br />

2010 reforms, e. g. through the introduction<br />

of a federal minimum wage and discussions<br />

about lowering the retirement age for certain<br />

types of employees.<br />

The 2012 Spanish labor market reform<br />

While it took Germany several years to agree<br />

on reforming the labor market, the euro crisis<br />

forced Spain to follow a comparable path<br />

within a much shorter period of time. One of<br />

the key initiatives in this regard was the Spanish<br />

labor market reform announced in February<br />

2012. It had a significant impact on labor<br />

costs. Indeed, the OECD estimates that more<br />

than half of the 3.9 % decline in unit labor<br />

costs between Q4 2011 and Q2 2013 can be<br />

attributed to the labor market reform. Among<br />

the key adjustments were improvements in<br />

incentives for firms to hire as well as for individuals<br />

to look for work, e. g. by reducing<br />

severance payments and granting firms more<br />

flexibility in adjusting the size of their workforce.<br />

However, the reform fell short of (high)<br />

expectations. We view the labor market reform<br />

as an important step in the right direction,<br />

but we would like to see further progress<br />

on this issue. Still, the OECD estimates that<br />

the undertaking is responsible for the hiring<br />

of 25,000 employees with permanent contracts<br />

each month, especially among smalland<br />

mid-cap firms. We portray two Spanish<br />

small caps on page 44.<br />

Björn Eberhardt<br />

Global Macro Research<br />

+41 44 333 57 43<br />

bjoern.eberhardt@credit-suisse.com<br />

Javier J. Lodeiro<br />

Banking & Insurance Research<br />

+41 44 334 56 44<br />

javier.j.lodeiro@credit-suisse.com<br />

02_Unemployment rates<br />

in Germany and Spain<br />

Since 2005, the unemployment rate in Germany<br />

has nearly halved, also supported by the Hartz<br />

labor market reforms. Following the global<br />

financial crisis, the Spanish unemployment rate<br />

has shot up to levels beyond 25 %, well above<br />

the previous peak in 1994. Encouragingly,<br />

there have been early signs of improvement<br />

in recent months. Source: Datastream, Credit Suisse<br />

%<br />

30<br />

25<br />

20<br />

15<br />

10<br />

5<br />

0<br />

50<br />

1992 1997 2002 2007 2012<br />

Spain<br />

Rank (out of 148)<br />

1<br />

7 5 7<br />

22<br />

29<br />

22<br />

29<br />

Germany<br />

03_WEF competitiveness<br />

ranking puts Germany close<br />

to the top, with Spain still<br />

below its precrisis highs<br />

Germany has been assessed as a very competitive<br />

economy over the last eight years, without<br />

any substantial variability in its ranking. Spain’s<br />

competitive ranking has declined compared<br />

with precrisis levels, but the 2012 reform and<br />

the improved macroeconomic stability should<br />

lift its ranking back up again. Source: WEF, Credit Suisse<br />

22<br />

29<br />

7<br />

23<br />

33<br />

2007 2008 2009 2010 2011 2012 2013 2014<br />

Spain Germany Eurozone average<br />

5<br />

23<br />

42<br />

6<br />

23<br />

36<br />

6<br />

23<br />

36<br />

4<br />

24<br />

35