Europe

From Crisis to opportunity Global Investor, 01/2014 Credit Suisse

From Crisis to opportunity

Global Investor, 01/2014

Credit Suisse

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

GLOBAL INVESTOR 1.14 — 53<br />

P<br />

7<br />

2014<br />

P<br />

SVK<br />

4.3%<br />

10.4%<br />

P<br />

P<br />

88<br />

P<br />

LTU<br />

6.5%<br />

21.7%<br />

FIN<br />

5.4%<br />

34.3%<br />

P<br />

ROU<br />

4.5%<br />

22.9%<br />

BGR<br />

6.0%<br />

16.3%<br />

GRC<br />

6.3%<br />

13.8%<br />

LVA<br />

5.9%<br />

35.8%<br />

EST<br />

4.7%<br />

25.8%<br />

14<br />

St.Petersburg<br />

P<br />

2,857<br />

P<br />

SOUTH STREAM<br />

CYP<br />

5.2%<br />

6.8%<br />

390<br />

Ankara<br />

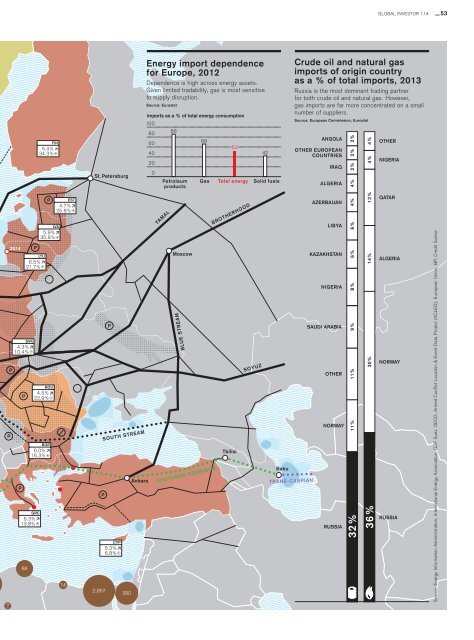

Energy import dependence<br />

for <strong>Europe</strong>, 2012<br />

Dependence is high across energy assets.<br />

Given limited tradability, gas is most sensitive<br />

to supply disruption.<br />

Source: Eurostat<br />

imports as a % of total energy consumption<br />

100<br />

80<br />

86<br />

60<br />

66<br />

53<br />

40<br />

42<br />

20<br />

0<br />

Petroleum<br />

products<br />

Gas Total energy Solid fuels<br />

YAMAL<br />

Moscow<br />

BLUE STREAM<br />

SOUTHERN CORRIDOR<br />

BROTHERHOOD<br />

Tbilisi<br />

SOYUZ<br />

Baku<br />

TRANS-CASPIAN<br />

Crude oil and natural gas<br />

imports of origin country<br />

as a % of total imports, 2013<br />

Russia is the most dominant trading partner<br />

for both crude oil and natural gas. However,<br />

gas imports are far more concentrated on a small<br />

number of suppliers.<br />

Source: <strong>Europe</strong>an Commission, Eurostat<br />

ANGOLA<br />

OTHER EUROPEAN<br />

COUNTRIES<br />

IRAQ<br />

ALGERIA<br />

AZERBAIJAN<br />

LIBYA<br />

KAZAKHSTAN<br />

NIGERIA<br />

SAUDI ARABIA<br />

OTHER<br />

NORWAY<br />

RUSSIA<br />

11% 9% 8% 6% 6% 4% 4% 3% 3% 3%<br />

11%<br />

30% 14% 12% 4% 4%<br />

32%<br />

36%<br />

OTHER<br />

NIGERIA<br />

QATAR<br />

ALGERIA<br />

NORWAY<br />

RUSSIA