Le principe de prudence : Les amortissements

Le principe de prudence : Les amortissements

Le principe de prudence : Les amortissements

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

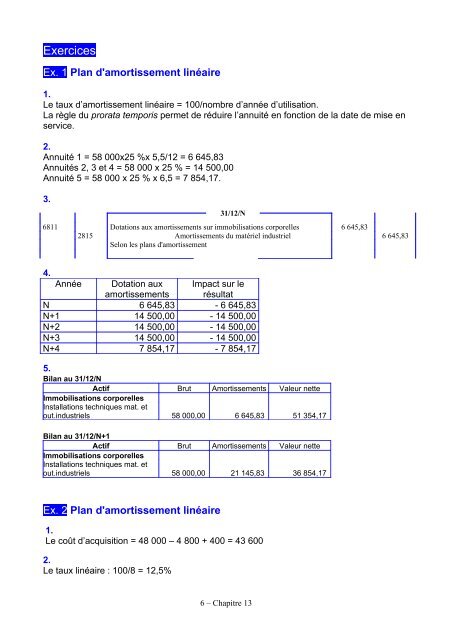

Exercices<br />

Ex. 1 Plan d'amortissement linéaire<br />

1.<br />

<strong>Le</strong> taux d’amortissement linéaire = 100/nombre d’année d’utilisation.<br />

La règle du prorata temporis permet <strong>de</strong> réduire l’annuité en fonction <strong>de</strong> la date <strong>de</strong> mise en<br />

service.<br />

2.<br />

Annuité 1 = 58 000x25 %x 5,5/12 = 6 645,83<br />

Annuités 2, 3 et 4 = 58 000 x 25 % = 14 500,00<br />

Annuité 5 = 58 000 x 25 % x 6,5 = 7 854,17.<br />

3.<br />

31/12/N<br />

6811 Dotations aux <strong>amortissements</strong> sur immobilisations corporelles 6 645,83<br />

2815 Amortissements du matériel industriel 6 645,83<br />

Selon les plans d'amortissement<br />

4.<br />

Année Dotation aux<br />

<strong>amortissements</strong><br />

Impact sur le<br />

résultat<br />

N 6 645,83 - 6 645,83<br />

N+1 14 500,00 - 14 500,00<br />

N+2 14 500,00 - 14 500,00<br />

N+3 14 500,00 - 14 500,00<br />

N+4 7 854,17 - 7 854,17<br />

5.<br />

Bilan au 31/12/N<br />

Actif Brut Amortissements Valeur nette<br />

Immobilisations corporelles<br />

Installations techniques mat. et<br />

out.industriels 58 000,00 6 645,83 51 354,17<br />

Bilan au 31/12/N+1<br />

Actif Brut Amortissements Valeur nette<br />

Immobilisations corporelles<br />

Installations techniques mat. et<br />

out.industriels 58 000,00 21 145,83 36 854,17<br />

Ex. 2 Plan d'amortissement linéaire<br />

1.<br />

<strong>Le</strong> coût d’acquisition = 48 000 – 4 800 + 400 = 43 600<br />

2.<br />

<strong>Le</strong> taux linéaire : 100/8 = 12,5%<br />

6 – Chapitre 13