Le principe de prudence : Les amortissements

Le principe de prudence : Les amortissements

Le principe de prudence : Les amortissements

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

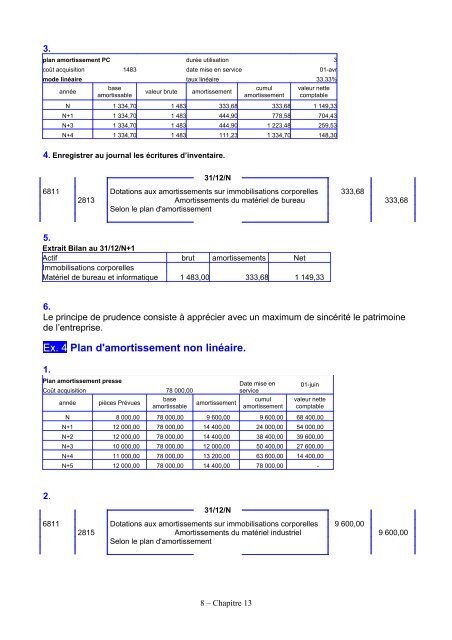

3.<br />

plan amortissement PC durée utilisation 3<br />

coût acquisition 1483 date mise en service 01-avr<br />

mo<strong>de</strong> linéaire taux linéaire 33,33%<br />

année<br />

base<br />

amortissable<br />

valeur brute<br />

amortissement<br />

cumul<br />

amortissement<br />

valeur nette<br />

comptable<br />

N 1 334,70 1 483 333,68 333,68 1 149,33<br />

N+1 1 334,70 1 483 444,90 778,58 704,43<br />

N+3 1 334,70 1 483 444,90 1 223,48 259,53<br />

N+4 1 334,70 1 483 111,23 1 334,70 148,30<br />

4. Enregistrer au journal les écritures d’inventaire.<br />

31/12/N<br />

6811 Dotations aux <strong>amortissements</strong> sur immobilisations corporelles 333,68<br />

2813 Amortissements du matériel <strong>de</strong> bureau 333,68<br />

Selon le plan d'amortissement<br />

5.<br />

Extrait Bilan au 31/12/N+1<br />

Actif brut <strong>amortissements</strong> Net<br />

Immobilisations corporelles<br />

Matériel <strong>de</strong> bureau et informatique 1 483,00 333,68 1 149,33<br />

6.<br />

<strong>Le</strong> <strong>principe</strong> <strong>de</strong> pru<strong>de</strong>nce consiste à apprécier avec un maximum <strong>de</strong> sincérité le patrimoine<br />

<strong>de</strong> l’entreprise.<br />

Ex. 4 Plan d'amortissement non linéaire.<br />

1.<br />

Plan amortissement presse<br />

Coût acquisition 78 000,00<br />

année pièces Prévues<br />

base<br />

amortissable<br />

amortissement<br />

Date mise en<br />

service<br />

cumul<br />

amortissement<br />

01-juin<br />

valeur nette<br />

comptable<br />

N 8 000,00 78 000,00 9 600,00 9 600,00 68 400,00<br />

N+1 12 000,00 78 000,00 14 400,00 24 000,00 54 000,00<br />

N+2 12 000,00 78 000,00 14 400,00 38 400,00 39 600,00<br />

N+3 10 000,00 78 000,00 12 000,00 50 400,00 27 600,00<br />

N+4 11 000,00 78 000,00 13 200,00 63 600,00 14 400,00<br />

N+5 12 000,00 78 000,00 14 400,00 78 000,00 -<br />

2.<br />

31/12/N<br />

6811 Dotations aux <strong>amortissements</strong> sur immobilisations corporelles 9 600,00<br />

2815 Amortissements du matériel industriel 9 600,00<br />

Selon le plan d'amortissement<br />

8 – Chapitre 13