AC Choksi Share Brokers Private Limited - Myiris.com

AC Choksi Share Brokers Private Limited - Myiris.com

AC Choksi Share Brokers Private Limited - Myiris.com

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

A C <strong>Choksi</strong><br />

<strong>Share</strong> <strong>Brokers</strong> <strong>Private</strong> <strong>Limited</strong><br />

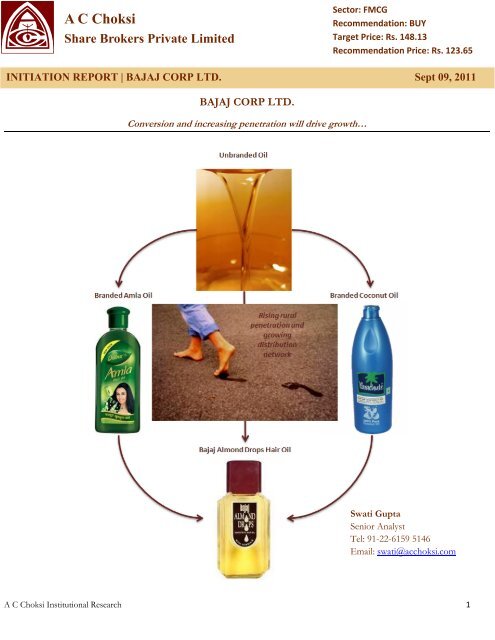

INITIATION REPORT | BAJAJ CORP LTD. Sept 09, 2011<br />

BAJAJ CORP LTD.<br />

Conversion and increasing penetration will drive growth…<br />

Sector: FMCG<br />

Re<strong>com</strong>mendation: BUY<br />

Target Price: Rs. 148.13<br />

Re<strong>com</strong>mendation Price: Rs. 123.65<br />

Swati Gupta<br />

Senior Analyst<br />

Tel: 91-22-6159 5146<br />

Email: swati@acchoksi.<strong>com</strong><br />

A C <strong>Choksi</strong> Institutional Research 1

A C <strong>Choksi</strong><br />

<strong>Share</strong> <strong>Brokers</strong> <strong>Private</strong> <strong>Limited</strong><br />

INITIATION REPORT | BAJAJ CORP LTD. Sept 09, 2011<br />

Re<strong>com</strong>mendation: BUY<br />

Target Price (Rs.) 148.1<br />

Re<strong>com</strong>mendation Price (Rs.) 123.7<br />

Potential Return (%) 19.8%<br />

BSE Sensex 16866.97<br />

Key Financials<br />

<strong>Share</strong>s Outstanding (mn) 147.5<br />

Face Value (Rs.) 1<br />

Market Capital (Rs. bn) 18.57<br />

Free Float (Rs. bn) 3.68<br />

Dividend Yield (%) 1.5%<br />

Stock Data<br />

BSE Code 533299<br />

NSE Code BAJAJCORP<br />

Bloomberg BJCOR IN<br />

Reuters Code B<strong>AC</strong>O.BO<br />

52-Week Range (Rs.) 151.50/73.30<br />

<strong>Share</strong> Holding Pattern 30 th June 2011<br />

FII, 5%<br />

DII, 4%<br />

Others, 6<br />

%<br />

Promoter,<br />

85%<br />

Investment Summary:<br />

• Almond Drops- Market leader in LHO Category:<br />

Bajaj Corp is the market leader in the LHO category in India through its<br />

flagship brand “Bajaj Almond Drops Hair Oil (ADHO)”. Almond hair<br />

oil category witnessed 29% CAGR by volume and 37.5% CAGR by<br />

value over FY07-FY11. ADHO <strong>com</strong>mands dominant market share in<br />

LHO category. Its market share by value improved from 40.3% during<br />

FY08 to 54.2% during Q1FY12. The <strong>com</strong>pany is targeting 60-65%<br />

market share over the next 3-4 years.<br />

• Strong volume growth of Almond hair oil:<br />

During Q1FY12, ADHO had achieved a dominant market share<br />

(volume) of 50.4% in LHO category as <strong>com</strong>pared to 38.4% in FY08.<br />

With rising disposable in<strong>com</strong>e, consumers tend to up-trade and ADHO<br />

emerged as a key beneficiary of changing consumer preferences.<br />

• Pricing Power and Premium Margins:<br />

Bajaj Corp has created a niche for itself which enables it to <strong>com</strong>mand<br />

premium prices as <strong>com</strong>pared to its peers. The <strong>com</strong>pany has successfully<br />

increased its prices at 7 year CAGR of 6.4%, without hampering volume<br />

growth. The <strong>com</strong>pany <strong>com</strong>mands one of the highest EBITDA margins<br />

in the industry. We believe that ADHO will continue to maintain<br />

premium pricing going forward due to strong brand equity and niche<br />

category positioning.<br />

• Conversion and strong distribution network to drive growth:<br />

ADHO is gaining market share at the expense of its peers. Going<br />

forward, it is expected to derive conversion from unbranded oils,<br />

coconut oil and amla oil. Further, Bajaj Corp is rapidly expanding its<br />

distribution reach as reaches urban and rural consumers through 2.02<br />

mn retail outlets serviced by 5690 direct distributors and 10,085<br />

wholesalers. Going forward, the <strong>com</strong>pany is likely to continue its thrust<br />

to strengthen its distribution reach to expand its market share in LHO<br />

category.<br />

• Valuation:<br />

We Initiate coverage on Bajaj Corp for 12-18 month horizon, with a<br />

target price of Rs. 148.13 per share based on DCF valuation method.<br />

Our DCF-based target price implies an earnings multiple of 14.55x<br />

FY13 earnings. This multiple is at significant discount as <strong>com</strong>pared to<br />

its peers, which factors in the risk of it being a single product <strong>com</strong>pany.<br />

A C <strong>Choksi</strong> Institutional Research 2

A C <strong>Choksi</strong><br />

<strong>Share</strong> <strong>Brokers</strong> <strong>Private</strong> <strong>Limited</strong><br />

INITIATION REPORT | BAJAJ CORP LTD. Sept 09, 2011<br />

Company Background:<br />

Bajaj Corp Ltd. (BCL), a leading producer of hair oils in India is a part of Shishir Bajaj<br />

Group of Companies. It was incorporated as ‘Bhaumik Agro Products <strong>Private</strong> <strong>Limited</strong>’<br />

on April 25, 2006. The name of the <strong>com</strong>pany was changed to Bajaj Corp Pvt. Ltd.<br />

Thereafter, the <strong>com</strong>pany was converted into public limited <strong>com</strong>pany in 2007 and the<br />

name changed to Bajaj Corp Ltd. The <strong>com</strong>pany <strong>com</strong>menced its business in April 2008.<br />

However, the products have been in existence since 1953 and were sold by different<br />

Bajaj group <strong>com</strong>panies.<br />

Bajaj Corp Ltd is one of the leading FMCG Company in India with brands in Hair care<br />

category. The brands have a track record of eight decades and the <strong>com</strong>pany is a part of<br />

one of the oldest business houses of the country. Bajaj Corp is promoted by Shishir<br />

Bajaj Group of <strong>com</strong>panies. Mr. Kushagra Nayan Bajaj is the chairman of the <strong>com</strong>pany.<br />

The <strong>com</strong>pany has a strong brand loyalty across the spectrum of Hair Oil category.<br />

Business Overview:<br />

The legacy of BCL’s products extends back to 1953 when Mr. Kamal Nayan Bajaj<br />

established Bajaj Sevahram (BSL) to market and sell hair oils and other beauty<br />

products. In 2001, in view of the impending Bajaj family settlement, the business was<br />

demerged to to form Bajaj Consumer Care Ltd (BCCL) in 2001 when BSL transferred<br />

its operating business and assigned all trademarks to BCCL. Subsequently, BCCL<br />

licensed these brands to BCL, pursuant to the Trademark License Agreement for a<br />

period of 99 years in 2008. As per the agreement, BCL will pay Royalty @ 1% of<br />

annual net sales turnover to BCCL.<br />

The <strong>com</strong>pany began operating as Bajaj Corp Ltd in April 2008. The <strong>com</strong>pany has since<br />

be<strong>com</strong>e India's third largest producer of hair oils and the largest producer of light hair<br />

oils, capturing an estimated 54.2% of the light hair oil market (based on value) in<br />

Q1FY12, according to Nielsen Retail Audit Report.<br />

The <strong>com</strong>pany’s key product is Bajaj Almond Drops Hair Oil (ADHO), a premium<br />

brand that is currently the market leader in the light hair oil segment. In addition, the<br />

<strong>com</strong>pany also markets other hair oil brands viz., Brahmi Amla Hair Oil (BAHO), Amla<br />

Shikakai (ASHO) and Jasmine Hair Oil (JHO). The <strong>com</strong>pany also produces oral care<br />

products under the brand name Bajaj Black Tooth Powder (BTP). During Q1FY12,<br />

Bajaj Corp forayed into cooling oil category with Kailash Parbat Cooling Oil (KPCO).<br />

A C <strong>Choksi</strong> Institutional Research 3

A C <strong>Choksi</strong><br />

<strong>Share</strong> <strong>Brokers</strong> <strong>Private</strong> <strong>Limited</strong><br />

INITIATION REPORT | BAJAJ CORP LTD. Sept 09, 2011<br />

Sales Break-up in Q1FY12 by Brand<br />

ADHO 91.56%<br />

Source: Company<br />

Other 8.53%<br />

KPCO 5.08%<br />

ASHO 0.44%<br />

BAHO 2.29%<br />

JHO 0.36%<br />

A C <strong>Choksi</strong> Institutional Research 4<br />

BTP<br />

0.36%<br />

Manufacturing Facilities Owned/Leased Products Excise Duty Exemption In<strong>com</strong>e Tax Exemption<br />

Company Operated<br />

Parwanoo, Himachal Pradesh Leased ADHO, ASHO<br />

Dehradun, Uttar Pradeh Owned ADHO<br />

Paonta Sahib, Himachal Pradesh Owned ADHO<br />

Installed Capacity 77.00 mn Ltrs<br />

Total Production in FY11 11.02 mn Ltrs<br />

Capacity Utilization 14.3%<br />

Starting from FY10, for 10<br />

years<br />

Starting from FY11, for 10<br />

years<br />

Starting from FY11, for 10<br />

years<br />

100% for 5 years, 30% for<br />

following 5 years<br />

100% for 5 years, 30% for<br />

following 5 years<br />

100% for 5 years, 30% for<br />

following 5 years<br />

Third Party<br />

Parwanoo, Himachal Pradesh<br />

ADHO, BAHO &<br />

JHO<br />

Starting from FY04, for 10<br />

years<br />

NA<br />

Udaipur, Rajasthan BTP NA NA<br />

Source: Company

A C <strong>Choksi</strong><br />

<strong>Share</strong> <strong>Brokers</strong> <strong>Private</strong> <strong>Limited</strong><br />

INITIATION REPORT | BAJAJ CORP LTD. Sept 09, 2011<br />

Key Management Details:<br />

Mr Kushagra Bajaj: Non Executive Chairman and one of the promoters of the<br />

<strong>com</strong>pany. He has 10 years of experience in the consumer & sugar industry and holds<br />

directorship other Bajaj group <strong>com</strong>panies including Bajaj Hindusthan Ltd.<br />

Equity Research Team<br />

022 6159 5146<br />

Mr. Roshan F. Hinger: Vice Chairman and Whole time director of the <strong>com</strong>pany with<br />

research@acchoksi.<strong>com</strong><br />

over 45 years of experience in FMCG business.<br />

Mr Sumit Malhotra: Whole time director of the <strong>com</strong>pany. He is Director of Sales and<br />

Marketing department of the <strong>com</strong>pany. He has 23 years of experience in FMCG<br />

sector.<br />

Mr Apoorv Bajaj: Executive President and also a promoter of the <strong>com</strong>pany.<br />

Mr. V.C. Nagori: Vice President – Finance. He has 25 years of experience in finance,<br />

taxation, audit and legal <strong>com</strong>pliance.<br />

Mr. D. K. Maloo: General Manager - Finance and <strong>com</strong>pany secretary. He has 22 years<br />

of experience in finance, taxation, audit and legal <strong>com</strong>pliance.<br />

A C <strong>Choksi</strong> Institutional Research 5

A C <strong>Choksi</strong><br />

<strong>Share</strong> <strong>Brokers</strong> <strong>Private</strong> <strong>Limited</strong><br />

INITIATION REPORT | BAJAJ CORP LTD. Sept 09, 2011<br />

Investment Rationale:<br />

Hair Oil Industry; growing at par with FMCG Industry Average:<br />

Hair care products contribute approximately 8% of the total FMCG market (Rs<br />

1338.76 bn) in India (Source: A C Nielsen). Hair care industry is growing at par with<br />

overall industry average of approximately 13-14%. Shampoo and hair oils, including<br />

coconut oils, continue to be the key <strong>com</strong>ponents of this segment. Hair oils category<br />

constitute more than 55% of the overall hair care industry in India. Hair oil category<br />

witnessed a volume growth of 16.7% CAGR from FY 2007 to FY 2011whereas it<br />

witnessed value growth of 20% CAGR over the same period. This growth is primarily<br />

attributed to the improvement in distribution network and supply chain efficiency.<br />

Source: A C Nielsen<br />

Hair Care Industry Size (Value) and Structure<br />

Coconut Oil<br />

(Rs.2,151 cr)<br />

Hair Oils( Rs.<br />

5,326 cr)<br />

Hair Care (Rs.<br />

10,243 cr)<br />

Perfumed Oil<br />

(Rs. 3,175 cr)<br />

Other Hair care<br />

products( Rs.<br />

4,917 cr)<br />

A C <strong>Choksi</strong> Institutional Research 6

A C <strong>Choksi</strong><br />

<strong>Share</strong> <strong>Brokers</strong> <strong>Private</strong> <strong>Limited</strong><br />

INITIATION REPORT | BAJAJ CORP LTD. Sept 09, 2011<br />

mn Ltr.<br />

300<br />

250<br />

200<br />

150<br />

100<br />

50<br />

0<br />

Overall Hair Oil Market by Volume Overall Hair Oil Market by Value<br />

Source: A C Nielsen<br />

mn Ltr.<br />

25<br />

20<br />

15<br />

10<br />

5<br />

0<br />

FY07 FY08 FY09 FY10 FY11 Q1FY12<br />

A C <strong>Choksi</strong> Institutional Research 7<br />

Rs. bn<br />

70<br />

60<br />

50<br />

40<br />

30<br />

20<br />

10<br />

0<br />

FY07 FY08 FY09 FY10 FY11 Q1FY12<br />

Light Hair Oil Segment is growing faster than overall hair oil market:<br />

Light Hair Oil (LHO) category is growing faster than overall Hair oil market in India.<br />

LHO category grew at 17.6% CAGR from FY07 to FY11 in volume terms while it<br />

grew at 25.5% CAGR from FY07 to FY11 in value terms.<br />

Light Hair Oil Market by Volume Light Hair Oil Market by Value<br />

Source: A C Nielsen<br />

FY07 FY08 FY09 FY10 FY11 Q1FY12<br />

Rs. bn<br />

10<br />

8<br />

6<br />

4<br />

2<br />

0<br />

FY07 FY08 FY09 FY10 FY11 Q1FY12<br />

Thus, share of LHO category increased consistently in overall hair oil category during<br />

past few years. This steady increase in LHO share was primarily driven by an increase<br />

in realizations which signifies a structural shift in consumer preference for non-sticky<br />

hair oils for which consumers are willing to pay premium price. This shift in consumer<br />

preference is attributable to rapid urbanization, favorable demographics, increase in<br />

disposable in<strong>com</strong>e, better distribution network and increasing penetration of branded<br />

oils in low SKUs.

A C <strong>Choksi</strong><br />

<strong>Share</strong> <strong>Brokers</strong> <strong>Private</strong> <strong>Limited</strong><br />

INITIATION REPORT | BAJAJ CORP LTD. Sept 09, 2011<br />

Source: A C Nielsen<br />

LHO share as a % of Overall Hair oil Market (by volume and value)<br />

From the following tables we can depict that penetration of branded hair oils is<br />

increasing steadily in India owing to conversion from unbranded hair oil to branded<br />

oils. The penetration of Hair oils grew 4% during 2010 and is currently at a penetration<br />

of 88.3%. On the other hand the unbranded Hair Oils which form 41% of the Hair Oil<br />

usage has seen a decline of 3% in the year 2010.<br />

100%<br />

90%<br />

80%<br />

70%<br />

60%<br />

50%<br />

40%<br />

30%<br />

20%<br />

10%<br />

0%<br />

58% 57%<br />

29%<br />

Source: A C Nielsen<br />

87%<br />

Penetration Level<br />

A C <strong>Choksi</strong> Institutional Research 8<br />

35%<br />

92%<br />

51%<br />

37%<br />

88%<br />

44%<br />

40%<br />

84%<br />

47%<br />

41%<br />

2000 2003 2005 2006 2010<br />

Unbranded Oil Branded Oil Total Hair Oil<br />

88%

A C <strong>Choksi</strong><br />

<strong>Share</strong> <strong>Brokers</strong> <strong>Private</strong> <strong>Limited</strong><br />

INITIATION REPORT | BAJAJ CORP LTD. Sept 09, 2011<br />

mn Ltrs<br />

Usage ratio of Branded Oil in Urban and Rural Market<br />

80%<br />

70%<br />

60%<br />

50%<br />

40%<br />

30%<br />

20%<br />

10%<br />

0%<br />

Source: A C Nielsen<br />

52%<br />

26%<br />

A C <strong>Choksi</strong> Institutional Research 9<br />

59%<br />

30%<br />

61%<br />

35%<br />

68%<br />

46%<br />

2000 2003 2005 2006<br />

Urban (%) Rural (%)<br />

Almond Drops- Market leader in fast growing LHO Category:<br />

Bajaj Corp is the market leader in the LHO category in India through its flagship brand<br />

“Bajaj Almond Drops Hair Oil (ADHO)”. As per Nielsen data, Almond hair oil<br />

category witnessed 29% CAGR by volume and 37.5% CAGR by value over FY07-<br />

FY11. ADHO <strong>com</strong>mands dominant market share in LHO category. Its market share<br />

by value improved from 40.3% during FY08 to 54.2% during Q1FY12.<br />

Almond Hair Oil (AHO) Market-Volume Almond Hair Oil (AHO) Market-Value<br />

12<br />

10<br />

8<br />

6<br />

4<br />

2<br />

0<br />

Source: A C Nielsen<br />

FY07 FY08 FY09 FY10 FY11 Q1FY12<br />

Rs. bn<br />

5<br />

4<br />

3<br />

2<br />

1<br />

0<br />

FY07 FY08 FY09 FY10 FY11 Q1FY12

A C <strong>Choksi</strong><br />

<strong>Share</strong> <strong>Brokers</strong> <strong>Private</strong> <strong>Limited</strong><br />

INITIATION REPORT | BAJAJ CORP LTD. Sept 09, 2011<br />

mn Ltr<br />

25<br />

20<br />

15<br />

10<br />

5<br />

0<br />

AHO share as a % of LHO - Volume AHO share as a % of LHO - Value<br />

FY07 FY08 FY09 FY10 FY11<br />

AHO LHO AHO volume as a % of LHO volume<br />

Source: A C Nielsen<br />

60%<br />

50%<br />

40%<br />

30%<br />

20%<br />

10%<br />

0%<br />

A C <strong>Choksi</strong> Institutional Research 10<br />

Rs. bn<br />

Strong volume growth of Almond hair oil:<br />

9<br />

8<br />

7<br />

6<br />

5<br />

4<br />

3<br />

2<br />

1<br />

0<br />

FY07 FY08 FY09 FY10 FY11<br />

AHO LHO AHO value as a % of LHO value<br />

During Q1FY12, ADHO had achieved a dominant market share (volume) of 50.4% in<br />

LHO category as <strong>com</strong>pared to 38.4% in FY08. During the period, Almond hair oil<br />

category registered ~29% CAGR by volume far higher than LHO category’s ~18%<br />

CAGR and overall Hair oil’s ~17% CAGR. Heavy hair oils like coconut oil and Amla<br />

oils are growing in high single digits while LHO are growing in high teens. It is visible<br />

that ADHO gained market share at the expense of its <strong>com</strong>petitors. With rising<br />

disposable in<strong>com</strong>e, consumers tend to up-trade and ADHO emerged as a key<br />

beneficiary of changing consumer preferences. ADHO is gaining market share from<br />

coconut hair oil, amla oils, other LHO and unbranded hair oil. Major conversion came<br />

from Marico’s Parachute Coconut Oil (CNO) and Dey’s Keo Karpin. While Marico<br />

maintained its dominant market share in CNO category due to continuous conversion<br />

from unbranded hair oil users to branded CNO users, Dey’s Medical’s Keo Karpin lost<br />

its dominant position in LHO segment. Keo Karpin had market share of 42% in LHO<br />

category during FY04 which declined to 19% in FY11.<br />

60%<br />

50%<br />

40%<br />

30%<br />

20%<br />

10%<br />

0%

A C <strong>Choksi</strong><br />

<strong>Share</strong> <strong>Brokers</strong> <strong>Private</strong> <strong>Limited</strong><br />

INITIATION REPORT | BAJAJ CORP LTD. Sept 09, 2011<br />

Premium positioning; High Realizations:<br />

ADHO is positioned as premium value-added hair oil due to its differentiation<br />

properties in terms of product (almond based) and packaging (glass bottle). The<br />

product is made from almond extracts with added Vitamin E and it is packaged in a<br />

glass-bottle instead of a PET-bottle, which helps to preserves the product properties<br />

for a longer period of time. Thus, Bajaj Corp has created a niche category of Almond<br />

Oil in LHO category which enables it to <strong>com</strong>mand premium prices as <strong>com</strong>pared to its<br />

peers. The <strong>com</strong>pany has successfully increased its prices from Rs 28 for 100ml in<br />

Mar’03 to Rs 46 in Apr’11 (CAGR of 6.4%), without hampering volume growth. The<br />

brand’s strong pricing power is evident from improvement in market share (by value)<br />

from 31.4% in FY06 to 54.2% in Q1FY12. In LHO category, ADHO’s closest<br />

<strong>com</strong>petitors are Dey’s Medical’s Keo Karpin with ~19% market share and Marico’s<br />

Hair & Care with ~16% market share. While 100 ml SKU of Keo Karpin and Hair &<br />

Care are available at Rs. 37 and Rs. 42 respectively, ADHO’s 100 ml SKU is available<br />

at Rs. 46. We believe that ADHO will continue to maintain premium pricing going<br />

forward due to strong brand equity and niche category positioning.<br />

100 ml<br />

ADHO<br />

Hair &<br />

Care<br />

Keo<br />

Karpin<br />

Source: Company<br />

Premium Pricing as <strong>com</strong>pared to <strong>com</strong>petitors<br />

0 10 20<br />

Prices( Rs.)<br />

30 40 50<br />

A C <strong>Choksi</strong> Institutional Research 11<br />

37<br />

42<br />

46

A C <strong>Choksi</strong><br />

<strong>Share</strong> <strong>Brokers</strong> <strong>Private</strong> <strong>Limited</strong><br />

INITIATION REPORT | BAJAJ CORP LTD. Sept 09, 2011<br />

Increasing focus on rural market without diluting margins:<br />

Light hair oils are primarily considered as an urban-centric product due to its premium<br />

pricing. However, it is unlikely to ignore 70% of total population living in rural India<br />

which is willing to up-trade with the rise in disposable in<strong>com</strong>e. In rural India<br />

disposable in<strong>com</strong>es are rising as farmers are shifting towards cash-crops and rural<br />

employment generation schemes are already in place. With growing exposure to<br />

information and media, rural consumers are well aware of branded products and are<br />

willing to up-trade. However, there is a significant difference between consumption<br />

pattern of rural and urban consumers. While consumption in urban India can be<br />

defined as “Small population-consuming a lot”, rural consumption can be defined as<br />

“Large population-consuming little”. Thus, it is important for a <strong>com</strong>pany looking<br />

forward to improve its traction in rural India to launch low-priced SKUs. Bajaj Corp is<br />

increasing its penetration in rural market with ADHO’s LPUs of 3 ml sachet and 20 ml<br />

which are priced at Rs. 1 and Rs. 10 respectively. Proportion of rural sales in overall<br />

revenues is increasing consistently. During FY05, 3 ml sachet contributed 0.8% of<br />

overall sales while during FY11 contribution of sachets increased to 10.4%. However,<br />

it is important to note that sachets are considered a low margin SKU due to high price<br />

sensitivity. However, Bajaj Corp happened to maintain its margins even in sachets due<br />

to cost rationalization in packaging material as sachet packaging is cheaper than glass<br />

bottle packaging. Thus, it gives Bajaj Corp an edge over its <strong>com</strong>petitors who would<br />

have to dilute their margins to increase traction in rural India. As a result, Bajaj Corp<br />

has a dominant market share of ~ 57.5% in LHO category in rural market. During<br />

FY11, sachet and 20 ml SKUs registered strong growth of 63% and 49.8% respectively<br />

which reinforces the fact of fast growing presence of Bajaj Corp in rural market.<br />

ADHO SKUs (ml)<br />

Source: Company<br />

300<br />

200<br />

100<br />

75<br />

50<br />

20<br />

Sachet<br />

Strong Growth in Low priced SKUs<br />

0% 10% 20% 30% 40% 50% 60% 70%<br />

A C <strong>Choksi</strong> Institutional Research 12

A C <strong>Choksi</strong><br />

<strong>Share</strong> <strong>Brokers</strong> <strong>Private</strong> <strong>Limited</strong><br />

INITIATION REPORT | BAJAJ CORP LTD. Sept 09, 2011<br />

100.0%<br />

90.0%<br />

80.0%<br />

70.0%<br />

60.0%<br />

50.0%<br />

40.0%<br />

30.0%<br />

20.0%<br />

10.0%<br />

0.0%<br />

Source: Company<br />

Sachets contribution increased consistently in overall sales<br />

0.8% 1.9% 2.9% 3.5% 5.8% 7.4% 10.4%<br />

FY05 FY06 FY07 FY08 FY09 FY10 FY11<br />

Sachet 20 50 75 100 200 300 500<br />

Strong Presence in North India:<br />

LHO sales are geographically concentrated specifically in the northern regions of the<br />

country due to willingness of consumers to try new products. Whereas, south India is<br />

still a major consumer of coconut oil due to its deep rooted traditional values. This<br />

can be depicted from the following chart as southern region contributes only 4% of<br />

total LHO sales while northern region contributes whopping 51%. On the other hand,<br />

contributions of eastern and western regions are almost similar at 22-23% level.<br />

Eastern region primarily uses mustard oil, amla oil, cooling oils and LHOs, while<br />

western region primarily uses coconut oil, mustard oil, groundnut oil and LHOs. Bajaj<br />

Corp has a strong presence in North, East and Western regions with its well<br />

entrenched distribution network.<br />

A C <strong>Choksi</strong> Institutional Research 13

A C <strong>Choksi</strong><br />

<strong>Share</strong> <strong>Brokers</strong> <strong>Private</strong> <strong>Limited</strong><br />

INITIATION REPORT | BAJAJ CORP LTD. Sept 09, 2011<br />

Source: Company<br />

80<br />

70<br />

60<br />

50<br />

40<br />

30<br />

20<br />

10<br />

0<br />

South, 4%<br />

Region wise break up of LHO Market<br />

North, 51%<br />

East , 22%<br />

West, 23%<br />

ADHO’s strong position in most of the states (except southern states)<br />

All India<br />

Punjab<br />

Source: Company<br />

Haryana<br />

Delhi<br />

Rajasthan<br />

U. P.<br />

ADHO Market <strong>Share</strong> % (Vol)<br />

A C <strong>Choksi</strong> Institutional Research 14<br />

Uttaranchal<br />

Assam<br />

Bihar<br />

Jharkhand<br />

Orissa<br />

W.Bengal<br />

Gujarat<br />

Total Urban Rural<br />

M.P.<br />

Chattisgarh<br />

Maharashtra<br />

Karnataka<br />

A.P.<br />

Tamil Nadu<br />

Kerala

A C <strong>Choksi</strong><br />

<strong>Share</strong> <strong>Brokers</strong> <strong>Private</strong> <strong>Limited</strong><br />

INITIATION REPORT | BAJAJ CORP LTD. Sept 09, 2011<br />

Strong Distribution network:<br />

Bajaj Corp has established strong distribution network in past few years. It reaches<br />

urban and rural consumers through 2.02 mn retail outlets serviced by 5690 direct<br />

distributors and 10,085 wholesalers. Northern Region is the major market for LHO<br />

category. Thus, approximately 49% of Bajaj corp’s stockists are based in North India,<br />

which ensures high penetration of ADHO in rural and urban area in the region. Bajaj<br />

Corp is rapidly expanding its distribution reach as its stockists strength has grown from<br />

less than 1500 in FY05 to 5690 in Q1FY12. Going forward, the <strong>com</strong>pany is likely to<br />

continue its thrust to strengthen its distribution reach to expand its market share in<br />

LHO category. Bajaj Corp has 32 regional distribution centers which further distributes<br />

to rural and urban stockists.<br />

Approximately 80% sales are derived through dominant distribution channels:<br />

Local Grocery stores and general stores are dominant distribution channels for LHO<br />

category as approximately 79% sales occur through these channels. Approximately<br />

80% of ADHO’s sales are derived through these channels. From distribution<br />

perspective, retailers play an important role to push a brand or influence purchase of<br />

consumers. Thus, ADHO which has already be<strong>com</strong>e a generic name for Almond oils<br />

provides the <strong>com</strong>pany an edge over its <strong>com</strong>petitors.<br />

Moderate Competitive intensity:<br />

Marico, Dabur, Bajaj Corp and Emami are the leading players in branded hair oil in<br />

India. Hair oil category is unlikely to face fierce <strong>com</strong>petition from MNCs as hair oils<br />

are not widely used in different geographies across the globe. Although hair oil<br />

category is highly penetrated, approximately 40% of total market is with unorganized<br />

players. Hence, with rising in<strong>com</strong>e levels and changing consumer preference there is a<br />

huge scope for all leading players to register healthy growth going forward. All four<br />

domestic players are market leader in their own niche. While Marico is a leading player<br />

with approximately 46% market share in branded CNO category, Dabur is leading in<br />

Amla oil category with ~70% market share. On the other hand, Emami is a dominant<br />

player in cooling oils with a market share of approximately 54.4% whereas Bajaj Corp<br />

is market leader in LHO category. Thus, all the players have stable growth <strong>com</strong>ing<br />

from their flagship product whereas they are trying to gain market share in other hair<br />

oil categories.<br />

A C <strong>Choksi</strong> Institutional Research 15

A C <strong>Choksi</strong><br />

<strong>Share</strong> <strong>Brokers</strong> <strong>Private</strong> <strong>Limited</strong><br />

INITIATION REPORT | BAJAJ CORP LTD. Sept 09, 2011<br />

ADHO’S Outlook:<br />

• Volume Outlook:<br />

We believe ADHO will register 15% volume growth during FY12 driven by<br />

conversion from peers, increasing penetration in rural market and expanding<br />

distribution reach. ADHO’s volume growth is primarily driven by conversion<br />

from coconut oil users, amla oil users, unbranded oil users and other LHO<br />

users. Amongst these, conversion from coconut oil users is approximately 40%<br />

whereas conversion from amla oil users is approximately 18%. During FY10,<br />

ADHO registered volume growth of 14.8% whereas during FY11 it registered<br />

a volume growth of 18.3%. It is important to note that, during FY10, ADHO’s<br />

100 ml SKU was available at 100% premium over Parachute’s 100 ml SKU.<br />

Whereas during FY11 copra prices increased significantly and Marico took a<br />

price increase of ~ 35%. On the other hand, ADHO took a price increase of<br />

~5% during the year. This resulted into a decline in premium (from 100% to<br />

56%) charged by ADHO over Parachute CNO. This reflected in more-thanaverage<br />

increase in ADHO’s volumes during FY11. However, increasing LLP<br />

(light Liquid Paraffin) prices necessitated Bajaj Corp to take further price<br />

increase and during Apr’11 Bajaj Corp had taken a weighted average price<br />

increase of 8.5%. On the other hand, copra prices started stabilizing due to<br />

flush season. Thus, during current year premium of ADHO over Parachute<br />

widened to ~70%. As per our estimates, during FY12 Marico is unlikely to take<br />

any steep price increase. Bajaj Corp is also not expected to take further price<br />

increase as LLP prices are expected to correct from H2FY12. Thus, this<br />

premium of 70% is expected to remain stable during the year. Local Grocery<br />

stores and general stores are dominant distribution channels for LHO category<br />

as approximately 79% sales occur through these channels.<br />

Dabur Amla’s 100 ml SKU is available at Rs. 36. During FY10 and FY11,<br />

ADHO’s 100 ml SKU <strong>com</strong>manded a premium of 18% and 17% respectively<br />

over Dabur Amla’s 100 ml SKU. However, during Q1FY12 this premium<br />

increased to 28% as ADHO had taken price increase of ~8.5% during Apr’11.<br />

During Q1FY12, Army which is one of the largest customers of Amla oil had<br />

downscaled business due to overall tightening up mandate by the government.<br />

Thus, volumes of Dabur Amla oil are likely to get hampered during FY12<br />

which will deter Dabur to take further price increase during the year.<br />

Thus, premium of ADHO over CNO and Amla oil widened during Q1FY12<br />

as <strong>com</strong>pared to FY11. Hence, we can conclude that ADHO’s volume growth<br />

will remain at normalized level of 15% during FY12.<br />

A C <strong>Choksi</strong> Institutional Research 16

A C <strong>Choksi</strong><br />

<strong>Share</strong> <strong>Brokers</strong> <strong>Private</strong> <strong>Limited</strong><br />

INITIATION REPORT | BAJAJ CORP LTD. Sept 09, 2011<br />

• Realizations Outlook:<br />

We have factored in 10% and 6% increase in realizations during FY12 and<br />

FY13 respectively. Bajaj Corp had already taken a weighted average price<br />

increase of 8.5% during Apr’11. As LLP prices are likely to correct from<br />

Q3FY12, we don’t anticipate any significant price increase during FY12.<br />

• Raw Materials Outlook:<br />

LLP, glass bottles and refined oil are major raw material for Bajaj Corp.<br />

LLP: LLP constitutes approximately 40-42% of total raw material cost of<br />

ADHO. During FY11, LLP cost registered a sharp increase of 49.5% due to<br />

high crude prices. We have factored in an increase of 28.2% in LLP prices<br />

during FY12. Further, as per our estimates LLP prices are expected to correct<br />

by 5.2 % during FY13.<br />

90<br />

80<br />

70<br />

60<br />

50<br />

40<br />

30<br />

LLP (Rs./Kg)<br />

Source: Company, A C <strong>Choksi</strong> Institutional Research<br />

A C <strong>Choksi</strong> Institutional Research 17

A C <strong>Choksi</strong><br />

<strong>Share</strong> <strong>Brokers</strong> <strong>Private</strong> <strong>Limited</strong><br />

INITIATION REPORT | BAJAJ CORP LTD. Sept 09, 2011<br />

Glass: Glass bottles constitute approximately 25-26% of total raw material cost<br />

of ADHO. We have factored in an increase of 17% during FY12 driven by an<br />

increase in soda ash prices. Major supplier for Bajaj Corp’s glass bottles, has<br />

already taken price increases during Q1FY12 and it is unlikely to take further<br />

price increase during the year unless there is an abnormal increase in soda ash<br />

prices.<br />

145<br />

140<br />

135<br />

130<br />

125<br />

120<br />

115<br />

110<br />

105<br />

100<br />

Glass Index<br />

Apr‐05 Apr‐06 Apr‐07 Apr‐08 Apr‐09 Apr‐10 Apr‐11<br />

Glass Index<br />

Source: Company, A C <strong>Choksi</strong> Institutional Research<br />

32<br />

30<br />

28<br />

26<br />

24<br />

22<br />

20<br />

18<br />

16<br />

14<br />

12<br />

10<br />

Soda Ash (Rs./Kg)<br />

Soda Ash (Rs./Kg)<br />

Source: Company, A C <strong>Choksi</strong> Institutional Research<br />

A C <strong>Choksi</strong> Institutional Research 18

A C <strong>Choksi</strong><br />

<strong>Share</strong> <strong>Brokers</strong> <strong>Private</strong> <strong>Limited</strong><br />

INITIATION REPORT | BAJAJ CORP LTD. Sept 09, 2011<br />

Refined oil: It constitutes approximately 8% of total raw material cost of<br />

ADHO. Production of groundnut and mustard are expected to increase by<br />

21% and 18% respectively, during the current crop season. However, due to<br />

high food inflation we have factored in an increase of 10% during FY12.<br />

Foray in emerging categories like cooling oils:<br />

Cooling oil is a fast growing category with a 5 year CAGR of ~20%. Bajaj Corp<br />

entered into this category with its Kailash Parbat Cooling oil (KPCO) brand during<br />

May’11 at pan-India level. During Q1FY12, KPCO registered sales of Rs. 54.2 mn.<br />

Emami is the market leader with approximately 54.4% market share in this category<br />

with its Navratna brand. Bajaj Corp is vying to create its niche in this category by<br />

positioning its product with differentiation factor. KPCO has extract of sandal which is<br />

known for its cooling properties and the product has different colour and fragrance as<br />

<strong>com</strong>pared to other products available in this category. Bajaj Corp has a strong<br />

distribution network to achieve pan-India scale for a new product at a faster pace. The<br />

product is gaining rapid traction in states like Punjab, Madhya Pradesh, Rajasthan and<br />

Gujarat where Bajaj Corp has a very strong distribution network. In cooling oil<br />

category, it primarily <strong>com</strong>petes with Emami which has a smaller distribution network<br />

as <strong>com</strong>pared to Bajaj Corp. There is a regional brand Himgange which has the second<br />

highest market share of ~25%. This brand is focused in U.P., Bihar, Chhattisgarh and<br />

Jharkhand. Marico is also prototyping its cooling oil “Parachute Advansed Coconut<br />

Cooling Oil” in Andhra Pradesh and is likely to expand its reach in near term in<br />

southern region where it has a strong foothold. Thus, we believe that strong<br />

distribution network and product differentiation will aid Bajaj Corp to gain traction<br />

and create its niche in this fast growing category.<br />

Shrinking investment behind under-performing categories:<br />

Bajaj Corp has presence in Amla oil category with its Bajaj Brahmi Amla Hair Oil<br />

(BAHO) and Bajaj Amla Shikakai Hair Oil (ASHO). Dabur is the market leader in<br />

Amla oil category with approximately 70% market share. However, despite of<br />

substantial advertisement and promotional spend these products were unable to get<br />

significant market share due to the lack of product differentiation. Thus, the <strong>com</strong>pany<br />

is unlikely to invest behind these products unless it finds a differentiation factor. Their<br />

contribution in sales and sales in absolute terms is declining consistently. Thus, we<br />

have factored in a decline of 16.0% in BAHO sales and 20.8% decline in ASHO sales<br />

during FY12.<br />

A C <strong>Choksi</strong> Institutional Research 19

A C <strong>Choksi</strong><br />

<strong>Share</strong> <strong>Brokers</strong> <strong>Private</strong> <strong>Limited</strong><br />

INITIATION REPORT | BAJAJ CORP LTD. Sept 09, 2011<br />

5.00%<br />

4.50%<br />

4.00%<br />

3.50%<br />

3.00%<br />

2.50%<br />

2.00%<br />

BAHO's Contribution to sales (%) BAHO Sales Value<br />

FY10 H1FY11 FY11 Q1FY12<br />

BAHO's Contribution to sales (%)<br />

Source: Company, A C <strong>Choksi</strong> Institutional Research<br />

2.00%<br />

1.50%<br />

1.00%<br />

0.50%<br />

0.00%<br />

A C <strong>Choksi</strong> Institutional Research 20<br />

Rs. mn.<br />

500<br />

400<br />

300<br />

200<br />

100<br />

0<br />

Q1 Q2 Q3 Q4<br />

FY11 FY10<br />

ASHO's Contribution to sales (%) ASHO Sales Value<br />

FY10 H1FY11 FY11 Q1FY12<br />

ASHO's Contribution to sales (%)<br />

Source: Company, A C <strong>Choksi</strong> Institutional Research<br />

Rs. mn<br />

200<br />

150<br />

100<br />

50<br />

0<br />

Q1 Q2 Q3 Q4<br />

FY11 FY10

A C <strong>Choksi</strong><br />

<strong>Share</strong> <strong>Brokers</strong> <strong>Private</strong> <strong>Limited</strong><br />

INITIATION REPORT | BAJAJ CORP LTD. Sept 09, 2011<br />

Financial Projections:<br />

Revenue to grow at 2-year CAGR of 21.3% by FY13:<br />

We expect market share of ADHO to increase going forward driven by its strong<br />

brand positioning, conversion from loose oils/coconut oil/amla oil users to ADHO<br />

and wider and deeper distribution network. Further, KPCO is expected to garner<br />

healthy traction in cooling oil category due to its product differentiation properties. In<br />

addition, Bajaj Corp is exploring options to extend its brand into high growth and high<br />

margin hair care and/or personal care categories to capitalize upon its brand equity and<br />

for optimum utilization of its wide spread distribution network. The <strong>com</strong>pany has<br />

sufficient cash, raised through IPO, to fund any inorganic or organic growth plans.<br />

Foray into cooling oil category and expansion in other categories will reduce its<br />

dependence on its core product ADHO. Hence, we believe Bajaj Corp is well on track<br />

for a steady revenue growth momentum. Going forward, overall revenues of the<br />

<strong>com</strong>pany are expected to grow at 2-year CAGR of 21.3% by FY13.<br />

6000<br />

5000<br />

4000<br />

3000<br />

2000<br />

1000<br />

0<br />

Revenue & Revenue Growth<br />

FY10 FY11 FY12E FY13E<br />

Total Sales Sales Growth<br />

Source: Company, A C <strong>Choksi</strong> Institutional Research<br />

A C <strong>Choksi</strong> Institutional Research 21<br />

40.0%<br />

35.0%<br />

30.0%<br />

25.0%<br />

20.0%<br />

15.0%<br />

10.0%<br />

5.0%<br />

0.0%

A C <strong>Choksi</strong><br />

<strong>Share</strong> <strong>Brokers</strong> <strong>Private</strong> <strong>Limited</strong><br />

INITIATION REPORT | BAJAJ CORP LTD. Sept 09, 2011<br />

Operating profit to witness healthy growth:<br />

Bajaj Corp’s operating margin is expected to grow at 2-year CAGR of 16.8% till FY13.<br />

However, during Q1FY12, raw material inflation remained intact. Further, during the<br />

quarter Bajaj Corp had launched KPCO which increased its A&P expenditure during<br />

the quarter. These factors will have dilutive impact on operating margin of the<br />

<strong>com</strong>pany during the year. Thus, we expect operating margins to contract by 351 bps yo-y<br />

during FY12. However, Management expects KPCO to achieve break even during<br />

second year of the launch with approximately 6% market share. Further, we expect a<br />

decline in LLP cost during FY13. This will result into margin expansion by 129 bps<br />

during FY13 as <strong>com</strong>pared to FY12.<br />

1600.0<br />

1400.0<br />

1200.0<br />

1000.0<br />

800.0<br />

600.0<br />

400.0<br />

200.0<br />

0.0<br />

EBITDA (Rs. Mn) & EBITDA Margin<br />

FY10 FY11 FY12E FY13E<br />

EBITDA EBITDA Margin<br />

Source: Company, A C <strong>Choksi</strong> Institutional Research<br />

Strong growth in net profit:<br />

A C <strong>Choksi</strong> Institutional Research 22<br />

35.0%<br />

30.0%<br />

25.0%<br />

20.0%<br />

15.0%<br />

10.0%<br />

We expect net profit to grow at 20.7% 2-year CAGR by FY13. We have factored in tax<br />

rate of 20% during FY12 and FY13. Despite of high tax rate as <strong>com</strong>pared to FY11 and<br />

margin contraction at operating level, net margin is expected to contract by just 117<br />

bps during FY12, primarily due to an increase in other in<strong>com</strong>e. During FY13, PAT<br />

margin is expected to expand by 86 bps.<br />

5.0%<br />

0.0%

A C <strong>Choksi</strong><br />

<strong>Share</strong> <strong>Brokers</strong> <strong>Private</strong> <strong>Limited</strong><br />

INITIATION REPORT | BAJAJ CORP LTD. Sept 09, 2011<br />

1600<br />

1400<br />

1200<br />

1000<br />

800<br />

600<br />

400<br />

200<br />

0<br />

PAT (Rs. Mn) & PAT Margin<br />

FY10 FY11 FY12E FY13E<br />

Adjusted PAT Net Margin<br />

Source: Company, A C <strong>Choksi</strong> Institutional Research<br />

Negative Working Capital Cycle:<br />

A C <strong>Choksi</strong> Institutional Research 23<br />

29.0%<br />

28.8%<br />

28.6%<br />

28.4%<br />

28.2%<br />

28.0%<br />

27.8%<br />

27.6%<br />

27.4%<br />

27.2%<br />

27.0%<br />

26.8%<br />

Bajaj Corp has a policy to sell in cash. Thus, its trade account receivable days were as<br />

low as 6.14 during FY11. This resulted into negative working capital cycle during the<br />

year. Going forward, we believe that the <strong>com</strong>pany will maintain its strong receivable<br />

policy. Further, inventory days are expected to decline from FY13, as exceptionally<br />

high raw material cost scenario seems to be over which will lead to a decline in raw<br />

material position building. Thus, we expect that the <strong>com</strong>pany will continue to maintain<br />

negative working capital cycle going forward.<br />

Cash rich business model; capable to fund capex through internal accruals:<br />

During FY10, Bajaj Corp had raised Rs. 2,970 mn through IPO. Out of this, the<br />

<strong>com</strong>pany had allocated Rs. 2200 mn for promotion of new products and Rs. 500 mn<br />

for acquisitions and strategic activities. In the recent past, acquisitions deals<br />

<strong>com</strong>manded high valuations in FMCG space. Thus, we believe that Bajaj Corp is<br />

scouting for a regional brand which it will scale up at pan-India level leveraging on its<br />

wide-spread distribution network. The <strong>com</strong>pany generates healthy cash flow at<br />

operational level; it generated Rs 1,014.6 mn for FY11 and will continue to generate<br />

healthy cash flows in future on account of negative working capital cycle. We have<br />

factored in a maintenance capex of Rs. 150 mn and Rs. 180 mn during FY12 and FY13<br />

in our estimates.

A C <strong>Choksi</strong><br />

<strong>Share</strong> <strong>Brokers</strong> <strong>Private</strong> <strong>Limited</strong><br />

INITIATION REPORT | BAJAJ CORP LTD. Sept 09, 2011<br />

DCF-Valuation<br />

Valuation:<br />

In our DCF model we have derived explicit free cash flow projections till FY 2020<br />

after which we have assumed a terminal value. Based on a W<strong>AC</strong>C of 10.90% and a<br />

perpetual growth rate of 5% we arrive at a DCF fair value of Rs. 148.13 for Bajaj Corp.<br />

We initiate the coverage on the stock with “BUY” re<strong>com</strong>mendation with potential<br />

upside of 19.8%.<br />

Particulars (Rs. Mn) FY 2011A FY 2012E FY 2013E FY 2014E FY 2015E FY 2016E FY 2017E FY 2018E FY 2019E FY 2020E<br />

Net revenues 3,587 4,475 5,282 6,074 6,985 7,963 8,998 10,078 11,186 12,305<br />

EBIT 1,063 1,164 1,435 1,680 1,929 2,117 2,388 2,570 2,848 3,066<br />

EBIT margin 29.6% 26.0% 27.2% 27.7% 27.6% 26.6% 26.5% 25.5% 25.5% 24.9%<br />

Net in<strong>com</strong>e (Adjusted) 1,031 1,234 1,502 1,719 1,844 1,982 2,210 2,371 2,606 2,500<br />

Free Cash Flow (FCF) analysis<br />

NOPLAT 853 855 1,059 1,250 1,347 1,456 1,652 1,779 1,979 1,835<br />

Depreciation 18 28 39 51 61 73 86 101 116 133<br />

Change in working capital (455) (212) (149) (156) (170) (184) (196) (207) (214) (218)<br />

Capex (62) (150) (180) (207) (237) (271) (306) (343) (380) (409)<br />

Free cash flow 1,264 945 1,067 1,250 1,341 1,442 1,628 1,744 1,929 1,777<br />

Discounted Free Cash Flow 8,001<br />

Perpetual growth rate 5.00%<br />

W<strong>AC</strong>C 10.90%<br />

Terminal Value 31,622<br />

Discounted Terminal Value 13,035<br />

Net Debt<br />

(813)<br />

Outstanding shares (mn)<br />

147.5<br />

Fair Value per share (Rs.) 148.13<br />

Source: Company, A C <strong>Choksi</strong> Institutional Research<br />

DCF sensitivity analysis<br />

Terminal growth rate<br />

148.13 3.00% 4.00% 5.00% 6.00% 7.00%<br />

9.90% 142.1 156.6 177.0 207.9 260.0<br />

10.40% 132.7 144.7 161.2 185.2 223.3<br />

W<strong>AC</strong>C 10.90% 124.5 134.6 148.1 167.2 196.0<br />

11.40% 117.3 125.8 137.1 152.5 174.9<br />

11.90% 110.9 118.2 127.6 140.3 158.1<br />

Source: A C <strong>Choksi</strong> Institutional Research<br />

A C <strong>Choksi</strong> Institutional Research 24

A C <strong>Choksi</strong><br />

<strong>Share</strong> <strong>Brokers</strong> <strong>Private</strong> <strong>Limited</strong><br />

INITIATION REPORT | BAJAJ CORP LTD. Sept 09, 2011<br />

Investment Concerns:<br />

• Single Product Concentration: ADHO contributes approximately 92% of overall<br />

sales. Although, ADHO enjoys pricing power due to its dominant market share in<br />

LHO category any unhealthy <strong>com</strong>petitive activity can hamper its market share<br />

and/or premium margins. However, the <strong>com</strong>pany is in the process of reducing this<br />

risk by diversifying its product portfolio through new product launches.<br />

• Volatility in raw material prices: LLP, glass bottles and vegetable oils are major<br />

raw material for Bajaj Corp. For LLP requirement, the <strong>com</strong>pany enters into future<br />

contracts while glass bottles and vegetable oils are purchased at spot prices. During<br />

FY11, raw material prices increased significantly and continue to move up till<br />

Q1FY12. The <strong>com</strong>pany had already taken price increase to mitigate the impact of<br />

input cost inflation. However, if raw material prices increases more than our<br />

estimates, it may adversely affect Bajaj Corp by either affecting margins or volumes.<br />

This will lead to deviation from our estimates.<br />

• Unsuccessful new product launches: The <strong>com</strong>pany is in the process of launching<br />

new products. However, any unsuccessful launch will impact profitability of the<br />

<strong>com</strong>pany and will burn its cash reserves. Along with that, it can also hamper brand<br />

equity of the <strong>com</strong>pany.<br />

• Risk related to acquisitions: The <strong>com</strong>pany is on a look out for acquisition.<br />

However, Bajaj Corp is keeping a conservative stance to fund these acquisitions<br />

(largely through internal accruals). Recent acquisition deals in FMCG space<br />

happened at exorbitant valuations. Thus, it will be tough to identify a strong regional<br />

player at reasonable valuations. Further, after a successful acquisition, the <strong>com</strong>pany<br />

runs a risk of being unable to create market for a regional brand at national level.<br />

• Slowdown in consumer spending: During macro-economic slowdown and rising<br />

inflation consumers tend to reduce spending by down trading. Considering Bajaj<br />

Corp’s premium priced flagship product, a slowdown in consumer spending would<br />

be a risk to our earnings estimates and target price as consumers tend to down-trade<br />

in such a scenario.<br />

• Low Float: Bajaj Consumer Care Ltd. Holds 84.75% stake in Bajaj Corp. Thus,<br />

Bajaj Corp has low liquidity which makes stock vulnerable to steep downward<br />

movement in case of unfavorable news. However, as per new SEBI guidelines,<br />

promoters need to gradually reduce their holding to 75% or below, over a period of<br />

time. This mandate will address the low liquidity concern in the stock.<br />

A C <strong>Choksi</strong> Institutional Research 25

A C <strong>Choksi</strong><br />

<strong>Share</strong> <strong>Brokers</strong> <strong>Private</strong> <strong>Limited</strong><br />

INITIATION REPORT | BAJAJ CORP LTD. Sept 09, 2011<br />

FINANCIALS:<br />

INCOME STATEMENT<br />

Particulars (Rs. Mn) FY10A FY11A FY12E FY13E<br />

Total Revenues (Net of Excise) 2,946 3,587 4,475 5,282<br />

Cost of goods sold 1,177 1,585 2,121 2,407<br />

Gross profit 1,769 2,002 2,354 2,874<br />

Gross profit Margin 60.0% 55.8% 52.6% 54.4%<br />

Selling, Gen & Adm Expenses 284 354 446 527<br />

Ad. & Sales Promotion 373 405 512 629<br />

Staff Cost 138 163 205 245<br />

EBITDA 973 1,081 1,191 1,474<br />

EBITDA Margin 33.0% 30.1% 26.6% 27.9%<br />

Depreciation & Amortization 8 18 28 39<br />

EBIT 964 1,063 1,164 1,435<br />

EBIT Margin 32.7% 29.6% 26.0% 27.2%<br />

Other In<strong>com</strong>e 51 178 379 442<br />

Exceptional Items 0 190 0 0<br />

Adjusted PBT 1,016 1,240 1,542 1,877<br />

Provision for In<strong>com</strong>e Taxes 176 210 308 375<br />

Reported PAT 839 841 1,234 1,502<br />

Adjusted PAT 839 1,031 1,234 1,502<br />

PAT Margin 28.5% 28.7% 27.6% 28.4%<br />

Diluted Weighted Average shares (mn) 125 148 148 148<br />

Diluted EPS (Rs.) 6.71 6.99 8.36 10.18<br />

Dividends 920 280 411 500<br />

Dividend Tax 156 47 68 83<br />

Source: Company, A C <strong>Choksi</strong> Institutional Research<br />

A C <strong>Choksi</strong> Institutional Research 26

A C <strong>Choksi</strong><br />

<strong>Share</strong> <strong>Brokers</strong> <strong>Private</strong> <strong>Limited</strong><br />

INITIATION REPORT | BAJAJ CORP LTD. Sept 09, 2011<br />

BALANCE SHEET<br />

Particulars (Rs. Mn) FY10A FY11A FY12E FY13E<br />

Current Assets<br />

Cash and cash equivalents 168 813 1,660 2,586<br />

Trade accounts receivable 29 60 76 91<br />

Inventories 99 144 198 216<br />

Loans and Advances 25 43 54 69<br />

Total current assets 320 1,061 1,988 2,963<br />

Fixed Assets<br />

Gross Block 196 247 397 577<br />

Less: Accumulated Depreciation 13 30 58 97<br />

Net Block 184 217 339 480<br />

Capital WIP 0 3 0 0<br />

Intangible Assets 0 0 0 0<br />

Investments 21 3,301 3,301 3,301<br />

Deffered Tax assets -1 0 0 0<br />

Misc. Expenses 23 1 0 0<br />

Total non-current assets 227 3521 3640 3781<br />

Total assets 547 4,581 5,628 6,744<br />

Current liabilities<br />

Sundry Creditors 145 356 479 554<br />

Advance from Customers 19 21 23 25<br />

Deposits from C&Fs and others 4 4 4 4<br />

Statutory Liabilities 43 53 64 76<br />

Other Liabilities 7 9 10 11<br />

Provisions 49 375 530 637<br />

Total current liabilities 268 818 1,110 1,308<br />

Long term debt 0 0 0 0<br />

Other long term liabilities 0 0 0 0<br />

Total long term liabilities 0 0 0 0<br />

Minority Interest 0 0 0 0<br />

<strong>Share</strong> Capital 125 148 148 148<br />

<strong>Share</strong> Premium 0 2,948 2,948 2,948<br />

Reserves & Surplus 154 668 1,423 2,341<br />

Total liabilities and equity 547 4,581 5,628 6,744<br />

Source: Company, A C <strong>Choksi</strong> Institutional Research<br />

A C <strong>Choksi</strong> Institutional Research 27

A C <strong>Choksi</strong><br />

<strong>Share</strong> <strong>Brokers</strong> <strong>Private</strong> <strong>Limited</strong><br />

INITIATION REPORT | BAJAJ CORP LTD. Sept 09, 2011<br />

CASH FLOW STATEMENT<br />

Particulars (Rs. Mn) FY10A FY11A FY12E FY13E<br />

Net in<strong>com</strong>e (loss) before taxes 1,016 1,240 1,542 1,877<br />

Operating profit before working capital changes 976 1,089 1,199 1,481<br />

(Increase)/decrease in Debtors (26) (29) (16) (15)<br />

(Increase)/decrease in Inventories (22) (45) (53) (19)<br />

(Increase)/decrease in Other Loans & Advances 64 (14) (11) (15)<br />

Increase/(decrease) in Creditors 8 219 125 77<br />

Increase/(decrease) in Other liabilities 6 11 12 14<br />

Increase/(decrease) in Provisions 24 (1) 2 3<br />

Cash generated from operations 1031 1228 1258 1526<br />

Tax Paid (170) (214) (308) (375)<br />

Net cash from operating activities 861 1015 950 1151<br />

Cash flow from investing activities<br />

Capital Expenditures (128) (62) (150) (180)<br />

Capital WIP 0 0 3 0<br />

Interest Received 46 113 324 396<br />

Dividend Received 0 5 5 5<br />

(Purchase)/Sale of Investment (Net) (19) (3227) 42 34<br />

Defferred tax liability 0 0 (0) 0<br />

Misc. expenses 0 0 1 0<br />

Net cash used in investing activities (102) (3171) 224 254<br />

Cash flows from financing activities<br />

Proceeds from the issue of share capital 0 2970 0 0<br />

Payment of Dividend (923) 0 (280) (411)<br />

Payment of Dividend Tax (157) 0 (47) (68)<br />

<strong>Share</strong> Issue Expenses (23) (168) 0 0<br />

Net Cash from financing activities (1102) 2802 (327) (479)<br />

Increase/Decrease in cash and cash equivalents (343) 646 847 926<br />

Cash and cash equivalents at the beginning 510 168 813 1,660<br />

Cash and cash equivalents at the end 168 813 1,660 2,586<br />

Source: Company, A C <strong>Choksi</strong> Institutional Research<br />

A C <strong>Choksi</strong> Institutional Research 28

A C <strong>Choksi</strong><br />

<strong>Share</strong> <strong>Brokers</strong> <strong>Private</strong> <strong>Limited</strong><br />

INITIATION REPORT | BAJAJ CORP LTD. Sept 09, 2011<br />

RATIOS<br />

Particulars (Rs. Mn) FY11A FY12E FY13E<br />

Growth (%)<br />

Total sales 21.8% 24.8% 18.0%<br />

EBITDA 11.1% 10.2% 23.7%<br />

Net profit 22.8% 19.7% 21.7%<br />

EPS 4.1% 19.7% 21.7%<br />

Per <strong>Share</strong><br />

Earnings 6.99 8.36 10.18<br />

Dividends 1.90 2.79 3.39<br />

Book value 25.51 30.63 36.85<br />

Cash 5.58 8.18 9.92<br />

Div Yield 1.5% 2.3% 2.8%<br />

Margins (%)<br />

Gross Margin 44.2% 47.4% 45.6%<br />

EBITDA 30.1% 26.6% 27.9%<br />

PAT 28.7% 27.6% 28.4%<br />

Financial<br />

Creditor Days 82 83 84<br />

Debtor Days 6.1 6.2 6.3<br />

Inventory Days 33.2 34.0 32.8<br />

Dividend Payout Ratio 27.2% 33.3% 33.3%<br />

Valuations<br />

PE (x) 17.6 14.7 12.1<br />

P/BV (x) 4.8 4.0 3.3<br />

EV/EBITDA (x) 16.0 13.8 10.6<br />

EV/Sales (x) 4.8 3.7 2.9<br />

ROE 51% 30% 30%<br />

ROCE 51% 30% 30%<br />

Source: Company, A C <strong>Choksi</strong> Institutional Research<br />

A C <strong>Choksi</strong> Institutional Research 29

A C <strong>Choksi</strong><br />

<strong>Share</strong> <strong>Brokers</strong> <strong>Private</strong> <strong>Limited</strong><br />

INITIATION REPORT | BAJAJ CORP LTD. Sept 09, 2011<br />

Disclaimer<br />

The information and views presented in this report are prepared by A C <strong>Choksi</strong> <strong>Share</strong> <strong>Brokers</strong> <strong>Private</strong> <strong>Limited</strong>. The information contained herein is based on<br />

our analysis and up on sources that we consider reliable. We, however, do not vouch for the accuracy or the <strong>com</strong>pleteness thereof. This material is for<br />

personal information and we are not responsible for any loss incurred based upon it. The investments discussed or re<strong>com</strong>mended in this report may not be<br />

suitable for all investors. Investors must make their own investment decisions based on their specific investment objectives and financial position and using<br />

such independent advice, as they believe necessary. While acting upon any information or analysis mentioned in this report, investors may please note that<br />

neither A C <strong>Choksi</strong> <strong>Share</strong> <strong>Brokers</strong> <strong>Private</strong> <strong>Limited</strong> nor any person connected with any associated <strong>com</strong>panies of A C <strong>Choksi</strong> <strong>Share</strong> <strong>Brokers</strong> <strong>Private</strong> <strong>Limited</strong><br />

accepts any liability arising from the use of this information and views mentioned in this document. The analysts for this report certifies that all of the views<br />

expressed in this report accurately reflect his or her personal views about the subject <strong>com</strong>pany or <strong>com</strong>panies and its or their securities, and no part of his or<br />

her <strong>com</strong>pensation was, is or will be, directly or indirectly related to specific re<strong>com</strong>mendations or views expressed in this report.<br />

Disclosure of Interest<br />

Analyst ownership of the stock NO<br />

Broking Relationship with the <strong>com</strong>pany covered NO<br />

Investment Banking relationship with the <strong>com</strong>pany covered NO<br />

Discretionary Portfolio Management Services NO<br />

Swati Gupta- 022 6159 5146<br />

swati@acchoksi.<strong>com</strong><br />

A C <strong>Choksi</strong> Institutional Research 30